Invest the Most with a Mega Backdoor Roth Solo 401(k)

The Mega Backdoor Roth Solo 401(k) is the only retirement plan that lets a self-employed person or small business owner with no employees contribute up to $70,000 in 2025 (or $77,500 if age 50+)—and convert most or all of it to Roth using after-tax contributions and in-plan Roth conversions.

Why Choose Us as Your Mega Backdoor Roth Solo 401(k) Provider?

IRA Financial specializes in Mega Backdoor Roth Solo 401(k) plans. When you partner with us, you’ll get expert guidance, transparent flat-fee pricing, and a streamlined setup designed specifically for high-earning self-employed individuals. We simplify the process of maximizing your tax-free retirement savings, allowing you to invest confidently and efficiently.

No commissions or surprise charges.

Serving investors in all 50 states.

Live chat available 8AM–6PM Central Time.

Manage assets or have us handle them.

Led by Roth IRA specialists.

100% Self-Directed IRA solutions.

Simple Transparent Pricing

At IRA Financial, we believe investing for retirement shouldn’t come with complicated fee structures or fine print. You keep more of what you earn, and you stay in control every step of the way.

Whether you’re investing in real estate, private companies, precious metals, or crypto, your IRA works harder—because your money stays invested, not chipped away by layers of fees.

Mega Backdoor Roth Solo 401(k)

$399

/ annually

- Best plan for self-employed individuals

- Invest in almost everything you want

- Checkbook Control - serve as your own trustee

- Maximize tax deductions (up to $77,500)

- Borrow up to $50,000 tax free!

- No transaction or asset value fees

- Guaranteed IRS audit protection

Mega Backdoor Roth Solo 401(k)

Premium Compliance

IRS tax rules and guidelines change annually. IRA Financial ensures your plan documents are updated and that your self-directed structure remains compliant and respected by the IRS.

Included with your plan

- Mega Backdoor Roth Solo 401(k) plan document updates as required by law

- Unlimited Roth Solo 401(k) plan tax & consulting services*

- Preparation and filing of IRS Form 5500-EZ

- Expedited IRS support

- Access to exclusive webinars

- Free copies of self-directed retirement books by Adam Bergman

Have questions?

How to Start a Mega Backdoor Roth Solo 401(k) Plan

Opening a Mega Backdoor Roth Solo 401(k) with IRA Financial is straightforward. Follow these steps to set up your plan and start investing.

01

Open Your Account

Opening a self-directed retirement account is simple. Submit your online account application in just a few minutes. Get Started

02

Get your Roth Solo 401(k) account number

Once your account is reviewed and approved. You’ll receive your account number and gain full access to our online retirement platform.

03

Fund your account

Transfer or rollover funds from an existing retirement account or fund your account through a direct contribution. Once funded, you’ll be able to make your investments and start growing your wealth.

The Advantages of a Mega Backdoor Roth Solo 401(k)

Higher contribution limits

The Mega Backdoor Roth strategy allows you to make after-tax contributions to your Solo 401(k) and convert them to Roth, enabling total Roth contributions that can exceed standard Roth IRA and Roth Solo 401(k) limits by over $40,000 annually.

Massive tax-free growth potential

Make after-tax contributions to your Solo 401(k), then convert them to Roth for tax-free growth and qualified tax-free withdrawals in retirement.

Ability to borrow funds

Borrow up to $50,000 or 50% of your balance (whichever is lower) without taxes or penalties—ideal for emergency liquidity.

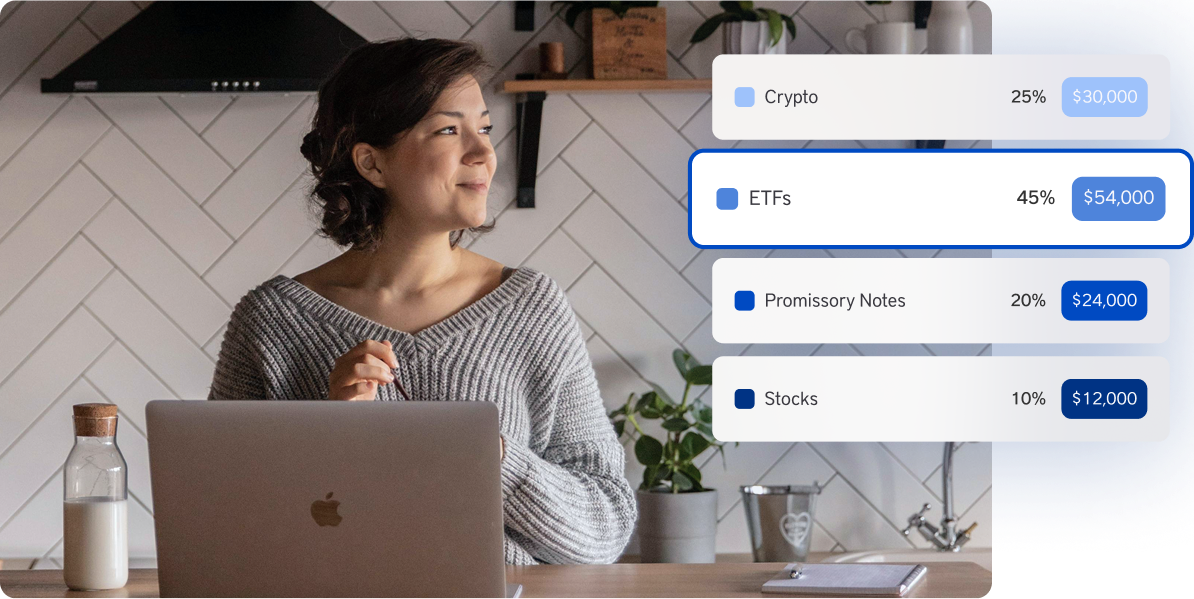

Broader investment Choices

Diversify beyond conventional investments like stocks and bonds into alternative assets, including real estate, private equity, cryptocurrency, precious metals, and more, enhancing your potential for wealth accumulation.

Direct investment control

Make direct investment decisions without needing brokerage or custodian approval. With full checkbook control, you have ultimate authority to manage your Roth Solo 401(k) investments efficiently and independently.

Creditor protection

Funds within your Solo 401(k) receive strong federal creditor protection under ERISA, providing greater security for your retirement savings compared to many other investment accounts.

Our Mega Backdoor Roth Solo 401(k) vs Other Providers

Many Roth Solo 401(k) providers charge asset-based fees, limit your investment choices to traditional assets, or require custodian approval for each transaction. Our flat-fee, self-directed plan offers full investment flexibility and direct access through checkbook control—so you can act quickly and invest on your terms.

IRA Financial | Other Providers | |

What Alternative Assets Can You Invest in with a Mega Backdoor Roth 401(k)?

A self-directed Solo 401(k) with Mega Backdoor Roth capability allows you to invest beyond traditional assets like stocks and mutual funds. Gain access to alternative investments such as real estate, private equity, cryptocurrency, precious metals, tax liens, and more—offering greater potential for diversification and long-term growth.

Book a Consultation

Schedule a free consultation with a member of our team to explore how opening a self-directed retirement account can unlock your ability to invest tax-free in a variety of alternative assets.

Mega Backdoor Roth Solo 401(k) FAQs

Below are answers to common Mega Backdoor Roth Solo 401(k) questions covering eligibility, contributions, investment flexibility, and tax advantages.

A Roth Solo 401(k) is a retirement plan specifically designed for self-employed and business owners without full-time employees. It offers:

- A Mega Backdoor Roth Solo 401(k) is an advanced retirement plan for self-employed individuals and small business owners with no full-time employees (other than a spouse). It allows you to dramatically increase your Roth retirement savings beyond standard IRS limits by combining after-tax contributions with in-plan Roth conversions. Features include:

- Ultra-High Roth Contribution Potential: Contribute up to $70,000 in 2025 (or $77,500 if age 50+) using a combination of employee deferrals, employer contributions, and after-tax contributions that can be converted to Roth—far exceeding the Roth IRA and standard Roth Solo 401(k) limits.

- Tax-Free Growth & Withdrawals: After-tax contributions converted to Roth grow tax-free, and qualified withdrawals in retirement are entirely tax-free under IRS rules.

- Investment Flexibility: When set up as a self-directed plan with checkbook control, a Mega Backdoor Roth Solo 401(k) allows direct investing in both traditional and alternative assets—such as real estate, private equity, and crypto—without custodian approval.

- Loan Access: Borrow up to $50,000 or 50% of your account balance, whichever is less, tax- and penalty-free, if repaid on schedule per IRS loan rules.

These three plans can get confusing, here’s a breakdown of the differences:

A Solo 401(k) is a retirement plan for self-employed individuals and small business owners with no full-time employees (other than a spouse). It allows for high annual contributions through a combination of pre-tax employee deferrals and employer profit-sharing contributions, offering tax-deferred growth and tax deductions today.

- 2025 limit: Up to $70,000 (or $77,500 if 50+)

- Contributions reduce taxable income now

- Withdrawals are taxable

A Roth Solo 401(k) is a type of Solo 401(k) that lets you make Roth contributions. These contributions grow tax-free, and qualified withdrawals in retirement are also tax-free.

- No upfront tax break

- Tax-free qualified withdrawals

- Ideal for those expecting higher taxes in retirement

A Mega Backdoor Roth Solo 401(k) is a more advanced setup that allows after-tax, non-Roth contributions beyond the standard Roth limit—then converts them to Roth. This strategy enables you to potentially contribute the entire 401(k) limit to Roth each year, if your plan allows it.

- Uses after-tax contributions + in-plan Roth conversions

- Requires a custom plan design (not supported by most brokerages)

- Enables dramatically higher Roth contributions than any other method

- Often paired with checkbook control and broader investment flexibility

To be eligible for a Mega Backdoor Roth Solo 401(k), you must be:

- Self-employed or the owner of a small business with no full-time employees other than yourself and possibly your spouse

- Earning self-employment income from freelance work, consulting, sole proprietorship, LLC, S-corp, or similar

This setup is ideal for high-income earners who want to maximize Roth contributions well beyond traditional IRS limits.

For 2025, a Solo 401(k)—including the Roth option—has a total annual contribution limit of $73,500 (or $77,500 if you’re age 50 or older). This total includes:

- Employee deferrals: Up to $23,000 (or **$30,500 if 50+), which can be designated as either Roth (after-tax) or traditional (pre-tax)

- Employer profit-sharing contributions: Up to 25% of net self-employment income (always pre-tax)

- After-tax contributions (only in custom plans): These are non-Roth, after-tax contributions that can be converted to Roth through the Mega Backdoor Roth strategy

Important: Standard Roth Solo 401(k) plans only allow Roth contributions on the employee deferral portion. To contribute more than $23,000/$30,500 to Roth, your plan must support after-tax contributions and in-plan Roth conversions.

With a Mega Backdoor Solo Roth 401(k) you can invest it:

- Real Estate – Buy rental properties, raw land, or commercial real estate.

- Cryptocurrency – Invest in Bitcoin, Ethereum, and other digital assets

- Private Equity – Fund startups, private businesses, or venture capital

- Tax Liens & Deeds – Purchase tax lien certificates for potential returns.

- Precious Metals – Buy IRS-approved gold, silver, and platinum.

Prohibited investments include collectibles and transactions involving disqualified persons (e.g., yourself or immediate family).

Yes—Mega Backdoor Roth Solo 401(k) plans allow participant loans as long as your plan document includes a loan provision.

- You can borrow up to $50,000 or 50% of your account balance, whichever is less

- The loan is tax- and penalty-free, provided it is repaid within 5 years with interest (usually prime rate + 1%)

No credit check is required, and the process is entirely self-directed if you have checkbook control

Beginning in 2024, thanks to the SECURE Act 2.0, the RMD rules have changed. Roth Solo 401(k) accounts are no longer required to take RMDs during the account owner’s lifetime. This rule mirrors how Roth IRAs work.

See What Our Clients Have to Say

My wife and I have decided to take control of our own IRAs. Using IRA Financial Group has been very simple. Our account manager is very accessible and responsive. The service received compared to the price paid is very good.

The team at IRA Financial was patient and awesome to help me fill out my 5500-EZ form for my Solo 401K. They are great!

The customer service rep was very helpful. She provided me the appropriate forms to get my Roth IRA checkbook writing set up and additional forms I'm going to need moving forward. IRA Financial team is the best!!

Start Self-Directing Your Retirement

Build your retirement with a self directed IRA designed for alternative and non traditional investments