What Is IRA Financial’s New Unified Platform? A Smarter Way to Invest in Both Traditional and Alternative Assets

For decades, self-directed investors faced an unavoidable tradeoff. If you wanted to invest in stocks and ETFs, you went to a brokerage. If you wanted to invest in real estate, private equity, or crypto, you went to a self-directed IRA custodian. Two accounts, two fee structures, two sets of tax forms, and two separate logins just to manage one retirement strategy.

IRA Financial has eliminated that tradeoff.

The IRA Financial Unified Platform is the first retirement account solution that combines institutional-grade stock and ETF trading with full access to alternative assets including real estate, private equity, private lending, precious metals, and cryptocurrency, all inside a single account for one flat annual fee.

Key Takeaways:

- What the Unified Platform is and why it is different from anything that existed before

- How the Interactive Brokers integration works for the traditional 40% of your portfolio

- What alternative assets are accessible on the same platform

- How the flat fee structure compares to asset-based models

- Why the August 2025 Executive Order matters for retirement investors

The Problem the Platform Was Built to Solve

The fragmentation of the retirement account industry was never a legal requirement. It was a business model.

Traditional brokerage firms like Fidelity and Schwab built platforms optimized for the assets they could easily manage, trade, and charge fees on: stocks, bonds, and mutual funds. Self-directed custodians built platforms for alternative assets but typically offered no integrated stock trading capability. The result was a bifurcated world where investors who wanted both had to manage multiple accounts, pay multiple fees, and reconcile multiple sets of statements at tax time.

IRA Financial spent sixteen years building toward a solution. The Unified Platform is the result: one account that does both, with none of the operational complexity that previously made the combined strategy inaccessible for most investors.

The Traditional Side: Institutional-Grade Trading Through Interactive Brokers

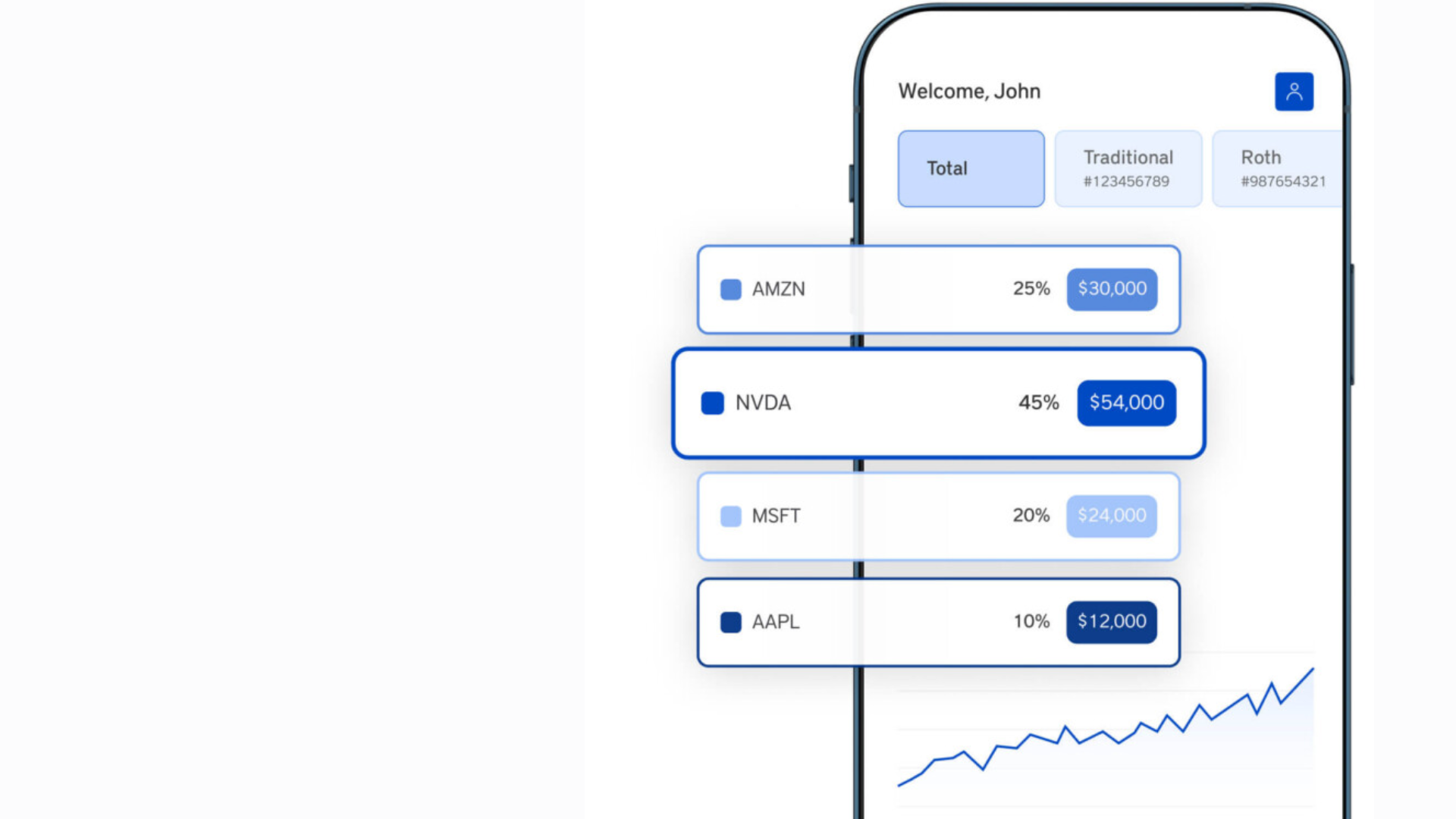

The 40% traditional anchor of any well-constructed retirement portfolio, the stocks, ETFs, and fixed income that provide liquidity and public market exposure, is now accessible directly inside an IRA Financial account through the firm’s integration with Interactive Brokers.

Interactive Brokers is one of the most technologically advanced trading platforms in the world, managing accounts across more than 150 market centers globally. Through the IRA Financial platform, account holders get zero-commission trading on US-listed stocks and ETFs, real-time execution with institutional-grade infrastructure, access to the full range of publicly traded securities, and all of it inside the same account that also holds their real estate, private equity, and crypto positions.

This matters for a specific reason. Rebalancing between the traditional and alternative portions of a portfolio previously required wire transfers between institutions, processing delays of five to ten business days, and coordination between two separate customer service systems. On the Unified Platform, moving capital from a stock position into a private lending note, or from a cash distribution on a real estate investment back into an index fund, happens within a single account interface.

The Alternative Side: The Full Universe of Self-Directed Investing

The alternative asset capabilities of the Unified Platform are the same as those IRA Financial has offered for sixteen years, now integrated with the stock trading functionality rather than operating separately.

Through the platform, a single IRA or Solo 401(k) can hold:

- Real estate: Direct ownership of residential or commercial property, participation in syndications, hard money loans secured by real property

- Private equity and venture capital: Direct investments in private companies, participation in PE or VC funds, pre-IPO placements

- Private lending: Promissory notes, bridge loans, hard money lending to real estate developers

- Precious metals: Physical gold and silver held in IRS-approved depositories

- Cryptocurrency: Direct ownership of Bitcoin, Ethereum, and other digital assets through IRA Financial’s platform, with 24/7 trading capability

All of these assets sit alongside the account’s stock and ETF holdings on a single dashboard, reported under a single set of annual IRS filings handled by IRA Financial’s in-house tax team.

The Fee Structure: One Flat Annual Fee Regardless of Account Size

The Unified Platform operates on IRA Financial’s established flat fee model. Account holders pay one annual fee regardless of how many assets the account holds or how large the account grows. There are no asset-based fees, no percentage of assets under management, and no per-transaction charges for alternative asset investments.

The practical implication of a flat fee compounds over time. A $500,000 account growing at 8% annually pays the same annual custodian fee as a $100,000 account. As the account appreciates, the custodian’s fee does not grow with it. This is structurally different from asset-based models where the custodian’s revenue increases automatically as the account grows, with no additional service being provided in return.

For a detailed comparison of flat fee versus asset-based custodian models and what the difference means over a ten-year holding period, see IRA Financial’s guide to Self-Directed IRA Custodian Fee Structures.

Book a free call with a self-directed retirement specialist

- Review your self-directed retirement options

- Learn about investing in alternative assets

- Get all of your questions answered

Why the 2025 Executive Order Matters

On August 7, 2025, President Trump signed an Executive Order directing the Department of Labor to reexamine its guidance on alternative assets in defined-contribution retirement plans and to develop safe harbors that allow fiduciaries to offer alternative asset allocations to plan participants.

The order explicitly states that it is the policy of the United States that every American preparing for retirement should have access to funds that include investments in alternative assets when the relevant plan fiduciary determines that such access provides an appropriate opportunity.

This represents a formal policy shift at the federal level, one that aligns with what IRA Financial has offered individual investors for sixteen years. The regulatory environment that previously created friction for 401(k) plans offering alternative assets is now being actively addressed by the Department of Labor under the direction of the Executive Order.

For self-directed IRA and Solo 401(k) investors, the practical implication is a more favorable regulatory environment for the strategy the Unified Platform is built to execute.

Who the Unified Platform Is Designed For

The platform is designed for investors who want to build a diversified retirement portfolio that includes both traditional and alternative assets, and who want to manage that portfolio without the operational complexity of maintaining accounts at multiple institutions.

Specifically, it is well suited for self-employed investors using a Solo 401(k) who want both checkbook control over alternative investments and direct stock trading capability in the same account, for investors rolling over a 401(k) from a former employer who want to deploy a portion into alternatives without giving up public market access, and for existing IRA Financial clients who previously managed their stock holdings at a separate brokerage and want to consolidate.

Final Thoughts

The Unified Platform is not a product update.

It is a structural change in what a retirement account can do. For the first time, investors who want both the liquidity and growth of public markets and the higher returns of alternative assets do not have to choose between them or manage the complexity of holding both in separate places.

One account, one flat fee, and the full investment universe the tax code has always permitted.

Related Articles

How IRA Financial’s New Platform Works

IRA Financial's Unified Platform combines stock and ETF trading, alternative asset investing, and cryptocurrency access inside a single retirement…

Self-Directed Retirement Providers That Let You Invest in Both Crypto and Private Equity

Can you invest in cryptocurrency and private equity inside the same retirement account? Yes! With the right self-directed retirement plan, you can…

Can You Trade Stocks Inside a Self-Directed IRA?

If you invest in alternative assets through a Self-Directed IRA, real estate, cryptocurrency, private equity, you've probably had to maintain a…

Alternative Investment IRA Options for Diversification

If you are still holding only stocks, mutual funds, and ETFs inside your IRA, you are investing with one hand tied behind your back. Most…