The Prohibited Transaction Minefield: Rules to Keep Your Real Estate IRA Compliant

What Constitutes a Prohibited Transaction?

A prohibited transaction is any improper use of your IRA by you (the IRA owner) or a disqualified person. This includes buying, selling, or leasing property between the IRA and the disqualified person, as well as furnishing goods, services, or facilities.

Disqualified persons include:

- You (the IRA holder)

- Your spouse

- Your ancestors and descendants (parents, children, grandchildren)

- Any entities where you or a disqualified person owns 50% or more

IRS Basics: Understanding Prohibited Transactions (IRC §4975)

- What counts? Any improper use of IRA assets by you or any disqualified person—including selling, leasing, lending, or providing services between your IRA and such persons—can trigger a prohibited transaction.

- Who’s “disqualified?” You, your spouse, parents, children, grandchildren, plus any entity you/control or your relatives control are considered disqualified according to the NAREA.

- Consequences: If violated, your entire IRA is deemed distributed as of Jan 1 of the year, taxed as ordinary income, and subject to early withdrawal penalties if you’re under 59½.

Key Compliance Rules for Real Estate IRAs

According to expert guidance, here's how to stay compliant:

1. Use Only IRA Funds

- All purchases, deposits, repairs, and expenses must come from the IRA (or from a non-disqualified third party).

- No personal funds can be used—doing so would trigger a prohibited transaction.

2. Avoid Services by Disqualified Persons

- Neither you nor any disqualified person may perform services related to the real estate (e.g., repairs, property management).

- Passive investment only: you can make decisions as the IRA LLC manager, but no hands-on work.

3. Non-Recourse Financing Only

- If you finance a real estate purchase, it must be through a non-recourse loan, meaning the lender can only claim the property—not your personal assets—if the loan defaults.

4. Title in the IRA's Name

- The deed/title must be held by the IRA entity (e.g., “XYZ LLC,” not your personal name).

Real-Life Example

If your Checkbook IRA buys a property for $100,000 and later sells it for $300,000, $200,000 in gains would be tax free, but only if:

- Your Roth IRA is at least five years old

- You are over age 59½ at distribution

- You followed all prohibited transaction rules

Common Prohibited Transaction Types in Real-Estate IRAs

Sweat Equity & Services Provided by Disqualified Persons

- You or a family member cannot personally perform services, such as renovations, property management, repairs, for an IRA-owned property.

- Hiring a non‑related third‑party property manager and paying them through the IRA avoids service‑related violations.

Leasing or Selling to Disqualified Parties

- Selling, leasing, or renting an IRA property to yourself or a family member is prohibited—even if rent is charged at fair market value.

- Example cases: leasing to your child or spouse violates rules even if rent is paid.

Lending, Credit, or Loan Guarantees

- Your IRA cannot lend money to or be used as collateral for loans for yourself or relatives.

- Non‑recourse financing is permissible, but personal guarantees are expressly disallowed. Examples include Peek v. Commissioner and Kellerman cases.

Transfers or Use of IRA Income/Assets

- Any transfer of income or assets to or for the benefit of a disqualified person is prohibited—this includes dividends, rental income, or profit distributions.

Real-Life Case Studies That Illustrate the Risks

When it comes to Self-Directed IRAs, the IRS draws strict lines around what account holders can and cannot do. Court rulings help clarify these boundaries, especially in situations involving real estate and personal business dealings. Two notable cases, Cherwenka and Kellerman, illustrate how closely the courts examine whether an IRA owner receives any personal benefit from transactions.

- In Cherwenka (2014), the IRA owner flipped properties but never received payments, discounts, or personal gain. The court allowed the activity, emphasizing that improvements directed through the IRA are permissible if no personal benefit occurs.

- In Kellerman (2015), however, the IRA owner’s personal business was intertwined with the IRA’s assets. The court ruled this a prohibited transaction, citing self-dealing and improper benefit to the owner’s outside entity.

Real Estate IRA Compliance Best Practices

Compliance Checklist for Real Estate IRAs

- Title & Ownership: Deed should be in the IRA or IRA-owned LLC, not your personal name.

- Funding & Expenses: All capital, rent income, maintenance, repairs—must flow through the IRA or IRA custodian; never from your personal account.

- No services by you or disqualified persons, even unpaid "sweat equity" is prohibited.

- Hire independent property manager, paid via IRA, no family or related-party involvement.

- Non-recourse financing only: Avoid any scenario requiring personal guarantees.

- Do not lease to disqualified persons, even at fair market rent.

- Records & Reserve Funds: Create a maintenance reserve (e.g. 3–6 months of expenses) inside IRA; document every transaction and keep them separate.

Additional Considerations & Risk Awareness

- Custodian expertise matters: Traditional custodians like Schwab or Fidelity may not support Real Estate IRAs. Using a specialty SDIRA custodian like IRA Financial is vital.

- Hidden costs that erode returns: Custodial fees, illiquidity, inability to deduct depreciation or mortgage interest, and difficulty making RMDs on illiquid property.

- Not beginner-friendly: SDIRAs demand high diligence and working knowledge of IRS rules, risk avoidance, and documentation.

Summary

Staying compliant means respecting the line between you and your IRA. Avoid self-dealing. Keep funds and services entirely within the IRA structure. Use disinterested third parties. Rely on non‑recourse financing only. And document everything with clear separation. These measures protect the tax-advantaged status of the IRA (and avoid a distribution event under IRC §4975)

Take Control of Your Real Estate IRA Today

Avoid costly prohibited transactions and keep your Self-Directed Real Estate IRA fully compliant. Our specialists guide you through every step—from funding and account setup to property management—so you can confidently grow your retirement portfolio.

Schedule a Free Consultation to learn more about the rules

Confident and ready to begin? Open Your Self-Directed IRA Today.

Recommended Reading

What is a Prohibited Transaction?

Common Prohibited Transactions

Tired of Loan Rejections? How to Use ROBS to Start Your Business Debt-Free in 2025

You have the industry expertise, a solid business plan, and the drive to build something of your own. You also have a substantial nest egg from your years in the corporate world, sitting in a 401(k) or IRA. The only thing standing between you and your dream of entrepreneurship is capital. If you've faced frustrating rejections from traditional lenders or are unwilling to risk your family's home as collateral for a loan, you may feel like you've hit a dead end.

But what if the key to unlocking your business was already in your possession? There is a powerful, IRS-compliant method to fund your startup or franchise purchase using your existing retirement funds—without incurring taxes or early withdrawal penalties. It's called the Rollover as Business Startups (ROBS) solution, and for a methodical entrepreneur like you, it deserves a closer look. This guide will demystify the ROBS process and show you how it can be your path to launching a debt-free business in 2025.

Key Takeaways

- Use retirement savings without taxes or penalties to fund your business or franchise.

- Secure debt-free capital while keeping 100% ownership and control of your company.

- Ensure full IRS compliance by partnering with an experienced ROBS provider.

What is a ROBS Plan? (And What It's Not)

First, it’s important to understand what a ROBS arrangement is not. It is not a loan, so you’re not saddled with interest payments, monthly installments, or lender approval. It is also not a withdrawal from your retirement account, meaning you won’t trigger income taxes or face the 10% early withdrawal penalty if you’re under 59½.

Instead, a ROBS is a specialized funding strategy allowed under IRS rules. It allows you to roll over funds from an eligible retirement account into a newly created C Corporation, which then issues stock purchased by your retirement plan. In other words, your retirement plan becomes a shareholder in your new company.

This structure transforms a portion of your nest egg into working capital—without debt, without depleting personal savings, and without giving up equity to outside investors. For aspiring entrepreneurs who want to start, buy, or grow a business, it’s a way to put their retirement dollars to work in their own enterprise, while still keeping the investment inside a tax-advantaged retirement framework.

The ROBS Process: A Step-by-Step Breakdown

While the ROBS structure is complex, the process can be broken down into clear, manageable steps. This is where a diligent researcher like you can appreciate the mechanics.

- Form a C-Corporation: The ROBS structure can only be used with a C-Corp. This is a specific IRS requirement to ensure the investment is structured correctly.

- Create a New 401(k) Plan: Your new C-Corp establishes its own 401(k) plan. This plan must be designed to allow for rollovers and permit investments in private company stock (in this case, your company's stock).

- Roll Over Your Existing Retirement Funds: You initiate a tax-free rollover from your existing retirement accounts (like an old 401(k), traditional IRA, or SEP IRA) into the new 401(k) plan sponsored by your business.

- The Plan Purchases Company Stock: The new 401(k) plan uses the rolled-over funds to purchase newly issued shares of stock in your C-Corporation.

- Your Business is Capitalized: The C-Corporation now has cash from the sale of its stock. This capital is on the company's balance sheet and can be used for any legitimate business expense, including startup costs, inventory, payroll, or franchise fees.

Book a free call with a self-directed retirement specialist

- Review your self-directed retirement options

- Learn about investing in alternative assets

- Get all of your questions answered

ROBS vs. Traditional Financing: A 2025 Comparison

For an aspiring entrepreneur weighing their options, seeing a direct comparison is essential. Here’s how a ROBS plan stacks up against an SBA loan and seeking private investors.

| Feature | ROBS Plan | SBA Loan | Private Investors |

| Debt-Free Capital | Yes | No | Yes |

| Retain Full Ownership | Yes | Yes | No |

| Credit/Collateral Required | No | Yes | No |

| Fast Funding | Yes (often 2-4 weeks) | No (can take months) | Varies |

| Flexible Use of Funds | Yes | Yes, with restrictions | Yes, with oversight |

| Personal Financial Risk | Yes (retirement funds) | Yes (personal guarantee) | No |

Addressing the Fear: Is ROBS Safe?

Your biggest concern is probably the complexity of a ROBS arrangement (and the fear that one misstep could trigger an IRS or Department of Labor audit). That’s a valid worry. The ROBS structure is incredibly powerful for funding a business, but it operates under a precise set of federal rules. Every stage, from the initial corporate setup to ongoing plan administration, must follow strict legal and tax guidelines. This is not a process to take on alone.

That’s why choosing a full-service ROBS provider is critical for your peace of mind. A trusted provider like IRA Financial not only manages the initial setup—forming your C corporation, establishing the ROBS 401(k) plan, and rolling over funds—but also stays with you for the long haul. We handle the ongoing annual compliance work, including Form 5500 filing, business valuations, and plan record-keeping.

Our ROBS 401(k) also includes guaranteed IRS audit protection, giving you the confidence to focus on running your business while we handle the regulatory details. With the right partner, you can use your retirement savings to launch your dream without losing sleep over compliance pitfalls.

The Verdict: Invest in Yourself, Debt-Free

For the right entrepreneur, a ROBS plan is a transformative funding solution. It allows you to bet on your own expertise and vision, launch your business on a solid, debt-free foundation, and retain full control of your company's future.

While it involves investing your retirement savings (a significant decision), it eliminates the need for high-interest loans and the dilution of ownership that comes with outside investors. With an expert partner to navigate the compliance, you can focus on what you do best: building your business.

Launch Your Business Debt-Free with ROBS

Stop letting loan rejections hold back your entrepreneurial dreams. With a ROBS plan, you can use your retirement funds to start or buy a business—without taxes, penalties, or giving up ownership. Our experts guide you through every step, from rollover to ongoing IRS compliance, so you can focus on building your business.

Schedule a Free Consultation to explore how ROBS works and to get started.

Frequently Asked Questions

Can I pay myself a salary with a ROBS plan?

What are the ongoing compliance requirements for a ROBS plan?

What happens if my business fails?

What types of retirement accounts can I use for a ROBS?

Can I use ROBS to fund a business with a partner?

How to Use the Roth IRA First-Time Home Buyer Strategy to Fund Your New Home

For many Americans, saving for a first home feels like running a marathon in heavy shoes. Between rising home prices and student loan debt, finding enough cash for a down payment can be a real challenge. But there’s a lesser-known IRS-approved strategy that can give first-time buyers a boost: using a Roth IRA to help fund your purchase.

This approach can provide a dual benefit. Your contributions grow tax-free inside the account. Furthermore, you can withdraw your contributions at any time, tax- and penalty-free—and in certain cases, even some earnings—without jeopardizing your retirement savings.

Let’s break down how this works, why it’s unique, and how it stacks up against saving in a traditional taxable account.

Key Takeaways

- The Roth IRA First-Time Home Buyer Rule lets you withdraw contributions anytime tax- and penalty-free, plus up to $10,000 in earnings tax-free if conditions are met.

- Using a Roth IRA for your down payment can save thousands in taxes compared to a taxable account, helping you reach home ownership faster.

- Strategic Roth IRA contributions allow you to cover your home purchase needs while keeping remaining funds invested for long-term, tax-free retirement growth.

Understanding the Roth IRA

A Roth IRA is a retirement account funded with after-tax dollars. That means you don’t get a tax deduction when you contribute, but your money grows tax free, and qualified withdrawals are also tax free. To withdraw Roth IRA funds tax- and penalty-free, the account must be open for at least five years and the withdrawal must be for a qualified reason, which is usually reaching age 59 ½. On the other hand, contributions can be withdrawn anytime regardless of age.

Two key features make the Roth IRA especially valuable for first-time home buyers. First, it offers contribution flexibility, allowing you to withdraw your original contributions at any time, for any reason, without taxes or penalties. Second, it includes a special first-time home buyer rule that lets you withdraw up to $10,000 in earnings tax- and penalty-free, if certain conditions are met, to buy or build your first home.

The First-Time Home Buyer Rule in Action

The IRS defines a “first-time home buyer” as someone (and their spouse, if married) who hasn’t owned a principle residence during the two-year period ending on the date of the new home purchase.

If you qualify, here’s how the rule works:

- Withdraw contributions first: No taxes, no penalties—regardless of age or reason.

- Withdraw up to $10,000 in earnings: Tax- and penalty-free if:

- The Roth IRA has been open at least five years.

- You use the funds within 120 days for the purchase or construction of your first home.

This $10,000 limit is lifetime per person. For a married couple, that could mean $20,000 total in earnings available for a first home purchase!

Roth IRA Contribution Strategy for Home Buyers

In 2026, Roth IRA contributions remain capped at $7,500 for individuals under 50, and $8,600 for those aged 50 and above, thanks to the catch‑up allowance. Your eligibility to contribute hinges on your Modified Adjusted Gross Income (MAGI). However, beginning in 2010, irrespective of income, anyone can make a Roth IRA contribution through the “Backdoor” Roth IRA strategy which entails making an after-tax IRA contribution and then making a tax-free Roth IRA conversion.

Unlike traditional IRAs, Roth contributions are made with after-tax dollars, so you don’t get a deduction up front. However, you can withdraw the contribution portion (the exact dollars you put in, not the investment earnings) at any time, for any reason, tax- and penalty-free. This is because you’ve already paid income tax on that money before contributing. Thus, if one makes annual Roth IRA contributions, the contributions can grow without tax and the contributions could then be taken out tax free. The earnings can remain in the Roth IRA and continue to grow tax free.

Book a free call with a self-directed retirement specialist

- Review your self-directed retirement options

- Learn about investing in alternative assets

- Get all of your questions answered

Why This Matters: The Down Payment Hurdle

According to recent housing market data, the average down payment on a home in the U.S. is around $35,000, though this varies widely by region. For first-time home buyers, the average is lower—closer to 6% of the home price, or roughly $20,000 on a $330,000 starter home.

For many buyers, coming up with that lump sum is the single biggest barrier to home-ownership. Using a Roth IRA can make a major difference—potentially covering all or most of the down payment without triggering extra taxes, which means you can get into your home sooner without draining your cash flow.

Example: Roth IRA vs. Personal Funds

Let’s say you’ve been diligently contributing $4,000 per year to a Roth IRA for eight years at an 8% annual return. At the end of eight years, you would have roughly $42,500—about $32,000 in contributions and $10,500 in earnings.

If you used the Roth IRA first-time home buyer strategy:

- You could withdraw the $32,000 in contributions tax- and penalty-free.

- If you qualify under the first-time home buyer rule, you could also withdraw up to $10,000 in earnings without tax or penalties.

- Any remaining earnings could stay invested in the Roth IRA, compounding tax free for your retirement.

Result: You have up to $42,000 available for your home without paying a dime in taxes—more than enough to cover the average first-time home buyer down payment.

Now compare this to using a taxable savings or investment account:

- You contribute the same $4,000 per year for eight years, earning the same 8% return.

- You end up with the same $42,500 total, but $10,500 of that is taxable investment gains.

- When you withdraw the money for your down payment, you could owe capital gains tax on those earnings—up to 15% or even 20% for high earners, plus state taxes in some cases. That’s $1,500–$2,000 (or more) lost to taxes.

Quick Comparison: Roth IRA vs. Personal Funds

| Feature | Roth IRA (First-Time Home Buyer) | Personal Taxable Account |

|---|---|---|

| Annual Growth | Tax-free | Taxable |

| Withdraw Contributions | Anytime, tax-free | Anytime, but no tax break |

| Withdraw Earnings | Up to $10,000 tax-free if qualified | Fully taxable |

| Impact on Retirement | Remaining funds grow tax-free | Remaining funds taxable |

| Tax on $10,500 in Earnings | $0 | Varies — up to $1,575 at 15% capital gains rate* |

| Total Net Proceeds | $10,500 | $8,925 |

*Assumes 2025 federal long-term capital gains rate of 15%, not including potential state taxes.

Conclusion

For first-time home buyers, the Roth IRA offers a rare combination of tax-free growth, flexible withdrawals, and a special IRS-approved home buyer perk. By strategically using your Roth IRA contributions—and possibly up to $10,000 in earnings—you can boost your down payment without triggering taxes or penalties, leaving more money in your pocket for your dream home.

Compared to saving in a taxable account, the Roth IRA can help you keep more of what you’ve earned, both for your home purchase and for your future retirement. With average down payments being one of the largest financial hurdles for first-time buyers, this strategy could be the key to making home-ownership a reality sooner.

Use Your Roth IRA to Make Homeownership a Reality

Don’t let the down payment hurdle slow you down. With the Roth IRA first-time home buyer strategy, you can access contributions—and potentially up to $10,000 in earnings—tax- and penalty-free. Our specialists help you understand your options, maximize your funds, and keep your retirement strategy on track.

Schedule a Free Consultation to see if using a Roth for your home purchase makes sense for you.

Ready to get started? Open Your Roth IRA Today.

Frequently Asked Questions

What is the Roth IRA First-Time Home Buyer Rule?

Who qualifies as a first-time home buyer under this rule?

What are the requirements for withdrawing Roth IRA earnings tax-free?

How much can I withdraw from a Roth IRA for my first home?

Disqualified Persons and Retirement Accounts: Rules & Restrictions

When it comes to self-directed retirement accounts—whether an IRA, Solo 401(k), or other plan, few topics are more critical (or more misunderstood) than the rules on disqualified persons. These rules are central to the IRS’s enforcement of prohibited transaction laws, and violating them can lead to severe tax consequences, including the immediate disqualification of your retirement account. But do the rules around disqualified persons change depending on the type of retirement account you use? And how do you stay compliant while investing in alternatives like real estate, private equity, or crypto?

This guide breaks down what a disqualified person is, how the rules apply across different plans, and where the distinctions lie depending on the account type.

Key Takeaways

- Whether you use a Self-Directed IRA or Solo 401(k) plan, the IRS definition of disqualified persons stays the same, but IRAs carry harsher penalties for violations, while 401(k)s may offer correction options.

- Personal use, payments, or services involving disqualified persons are prohibited and can trigger account disqualification, taxes, and penalties.

- Self-Directed IRAs offer flexibility, but Solo 401(k)s provide more control, the option for plan loans, and potentially more forgiveness if a mistake occurs—making them a smart choice for self-employed investors.

What Is a Disqualified Person?

In the context of retirement accounts, a disqualified person is someone who is too close to the retirement account owner, financially or familiarly, to be involved in transactions with the plan. The IRS created this designation to prevent self-dealing and abuse of tax-advantaged retirement funds.

Under IRC § 4975(e)(2), disqualified persons include:

- The IRA owner or plan participant

- Their spouse

- Lineal descendants and ascendants (children, parents, grandparents, etc.)

- Spouses of lineal descendants

- Entities (corporations, partnerships, LLCs, trusts, estates) owned 50% or more by disqualified persons

- Fiduciaries (e.g., a trustee or custodian)

- Service providers to the plan

In other words, you cannot use your retirement funds to benefit yourself or close family members either directly or indirectly.

What Is a Prohibited Transaction?

A prohibited transaction occurs when your retirement account engages in a deal with a disqualified person that benefits them personally—rather than serving the best interest of the retirement plan.

Examples include:

- Selling personal property to your IRA

- Buying a rental property and letting your child live in it

- Paying yourself a management fee from an IRA-owned business

- Using retirement funds to invest in a company you control

Prohibited transactions can result in disqualification of the plan, leading to immediate taxation of the account’s entire fair market value and possibly penalties.

Do the Rules Differ for IRAs and 401(k)s?

Here’s where things get interesting: The core definition of disqualified persons is the same across all retirement accounts, but the rules and consequences differ depending on whether you’re using an IRA (Traditional, Roth, SEP, SIMPLE) or a qualified plan like a Solo 401(k).

Let’s look at the key distinctions.

Disqualified Person Rules for IRAs

When using an IRA, including a Self-Directed IRA, the prohibited transaction rules are very strict.

If an IRA owner engages in a prohibited transaction:

- The entire IRA is disqualified as of January 1 of the year the transaction occurred.

- The account is treated as if all assets were distributed at their fair market value.

- This can result in income taxes, early withdrawal penalties, and loss of tax-deferred/tax-free status.

There is no grace period, and the IRS takes a hard line stance. Even minor indirect violations, like investing in an LLC partially owned by your child, can trigger disqualification.

Also, with IRAs, the account holder is not allowed to perform services for an asset held in the IRA (e.g., repairing a rental property), as that constitutes “sweat equity,” a form of indirect benefit.

Book a free call with a self-directed retirement specialist

- Review your self-directed retirement options

- Learn about investing in alternative assets

- Get all of your questions answered

Disqualified Person Rules for 401(k) Plans

Solo 401(k) plans follow the same definition of disqualified persons under IRC § 4975, but the rules and enforcement differ in key ways:

- Correction Opportunity

- If a prohibited transaction occurs in a 401(k) plan, the plan may not be immediately disqualified. The IRS allows certain violations to be corrected under EPCRS (Employee Plans Compliance Resolution System) if the mistake is unintentional.

- This is a huge advantage over IRAs, which have no such correction mechanism.

- Loan Option

- One key exception to the prohibited transaction rules for 401(k) plans is that a plan participant can borrow from the plan, as long as it follows strict rules:

- Maximum of $50,000 or 50% of account balance

- Repaid over 5 years

- Market interest rate

- IRAs do not allow loans to the account owner under any circumstances.

- One key exception to the prohibited transaction rules for 401(k) plans is that a plan participant can borrow from the plan, as long as it follows strict rules:

- Employer-Sponsored Flexibility

- A Solo 401(k) is treated as a qualified employer plan, even if the employer is a self-employed individual. This offers more administrative flexibility and potential insulation from certain prohibited transaction risks—provided the plan documents are written correctly and the plan sponsor acts prudently.

Real Estate Example: IRA vs. Solo 401(k)

Let’s say you want to invest in a rental property with your retirement funds. Here’s how disqualified person rules might play out:

| Action | Self-Directed IRA | Solo 401(k) |

|---|---|---|

| Buying a property your parent owns | Prohibited | Prohibited |

| Hiring your son to manage property | Prohibited | Prohibited |

| You do the plumbing yourself | Prohibited ("sweat equity") | Prohibited |

| Paying yourself a management fee | Prohibited | Prohibited |

| Borrowing from your retirement plan to buy the property | Not allowed | Allowed (via plan loan rules) |

| Mistakenly hiring a disqualified person, but catch the error | Immediate disqualification | May be correctable under EPCRS |

Common Misconceptions About Disqualified Persons

Let’s clear up some frequent misunderstandings:

- Cousins, siblings, and in-laws are not disqualified unless they fall into another category (e.g., a service provider).

- You can invest alongside a disqualified person in some cases (e.g., using your IRA to buy 50% of a property your brother owns the other 50% of), but there must be no pre-arranged deal and no shared benefit.

- Having your LLC do the deal does not remove disqualified person status if you or your family control the LLC.

- Just because something isn’t clearly listed in the Code doesn’t mean it’s allowed—the IRS looks at intent and indirect benefit.

To keep your retirement plan safe from disqualification, follow these tips:

- Understand who counts as a disqualified person

- Avoid any personal benefit from retirement plan assets

Do not provide services or labor to your IRA investments - Use third-party service providers instead of family

- Review operating agreements carefully if investing in LLCs or partnerships

- Work with professionals who understand self-directed retirement rules

- Keep detailed records of all transactions and documents

When in doubt, it’s better to walk away from a deal than to risk the entire retirement account.

Conclusion: Same Core Rules, Different Consequences

In summary, the definition of disqualified persons remains consistent across retirement plan types, but the impact of prohibited transactions differs. IRAs are zero-tolerance: one prohibited transaction equals total disqualification. 401(k) plans, especially Solo 401(k)s, offer more flexibility and correction options but still require strict adherence to the rules. If you’re investing in alternative assets with a retirement account, it’s essential to understand these distinctions. A well-structured Solo 401(k) may offer more leeway, but no plan is immune from IRS scrutiny.

When in doubt, ask yourself: Would this deal exist without my retirement account? If not, it’s probably a problem.

Protect Your Retirement and Invest with Confidence

Understanding disqualified persons and prohibited transactions is critical to keeping your retirement funds safe and IRS-compliant. With the right guidance and a self-directed account, you can invest in real estate, private equity, or other alternative assets without risking disqualification.

Schedule a Free Consultation to discuss the prohibited transaction rules.

Confident and ready to start? Open Your Account Today.

Frequently Asked Questions (FAQs)

Who is considered a disqualified person under IRS rules?

Do disqualified person rules apply differently to IRAs and 401(k)s?

Can I live in or use a property owned by my Self-Directed IRA or Solo 401(k)?

Can I invest in a business I own or control with my retirement account?

Can I correct a prohibited transaction if I made a mistake?

Real Estate Investing with a Self-Directed IRA

Real estate investing with a Self-Directed IRA allows you to diversify your retirement and invest in something you know and love. However, to invest in real estate with your IRA or any retirement account, you need to “self-direct” it. While there are variations in terms of eligibility and contributions for each of these plans, they all allow you to invest in real estate and other alternative investments such as gold, silver, cryptocurrencies, and private placements.

Additionally, you can invest in traditional investments such as stocks, bonds, and mutual funds. Hence, a Self-Directed IRA for real estate is a great way to secure your financial future by diversifying your retirement portfolio. However, owning real estate within an IRA can limit tax benefits like depreciation and interest write-offs, and incur additional costs such as appraisals and maintenance, which can affect the long-term value of the investment.

Key Takeaways

- A Self-Directed IRA lets you invest in real estate with tax-deferred or tax-free growth, helping diversify and grow your retirement savings beyond traditional assets.

- You must follow IRS rules, avoid prohibited transactions, and watch for UBIT if using loans. All income and expenses must flow through the IRA.

- Success starts with the right custodian. Options like checkbook control give you faster access to deals and more flexibility in managing your investments.

Introduction to Self-Directed IRAs

A Self-Directed IRA is a type of retirement account that allows investors to take control of their investments and make their own investment decisions. Unlike traditional IRAs, which typically limit investment options to stocks, bonds, and mutual funds, self-directed IRAs offer the flexibility to invest in a wide range of assets, including real estate, precious metals, private placements, and more.

Self-directed IRAs are particularly popular among real estate investors. These accounts enable investors to use their retirement funds to purchase investment properties, such as rental properties, commercial properties, and raw land. By leveraging a Self-Directed IRA for real estate investments, investors can potentially earn rental income, benefit from property appreciation, and enjoy significant tax advantages. Depending on whether the account is a traditional or Roth IRA, these benefits can include tax-deferred growth or even tax-free withdrawals in retirement.

The ability to diversify into real estate and other alternative investments makes self-directed IRAs an attractive option for those looking to enhance their retirement savings and align their investments with their financial goals and risk tolerance.

What is a Self-Directed IRA for Real Estate?

A Self-Directed IRA for real estate, also known as a Real Estate IRA, allows you to invest in any type of asset that is not prohibited by the IRS. The only prohibited transaction that you need to worry about with a real estate investment is the disqualified person’s rule. You (the IRA owner), your spouse, your lineal ascendants and descendants, their spouses, and entities controlled by such persons are not allowed to benefit from the investment. The Self-Directed IRA should be the only thing that receives a benefit, which are the tax advantages of the plan. It is crucial to understand real estate IRA rules to ensure compliance with regulations and guidelines, protecting your retirement savings and maintaining the tax-advantaged status of the account.

The Self-Directed IRA is one of the few choices for those wishing to invest in alternatives. Traditional plans offered by banks and other institutions limit your investment choices. Typically, you can only invest in stocks, bonds, mutual funds, and the like. Therefore, you must first set up a Self-Directed IRA to make real estate investments. Further, when using the right custodian, such as the IRA Financial Trust Company, you can gain checkbook control of your funds by using a Checkbook IRA. You never have to ask IRA Financial when you wish to make an investment. Other custodians require custodial consent for every investment you wish to make. This is bad for real estate investors. Delays in the process could cause you to lose out on a property you wish to purchase.

Benefits of Real Estate Investing with a Self-Directed IRA

Real estate is one of the most popular retirement investments among self-directed investors. One primary reason is that real estate is a tangible asset that produces steady income. For many investors, particularly those with real estate experience, it has been an integral investment in building retirement wealth.

Investing in real estate with a Self-Directed IRA has the following benefits:

- The potential to generate higher returns compared to traditional investment options.

- Helping to diversify your retirement savings. Real estate has traditionally generated high returns. However, with a Self-Directed IRA, you are not limited solely to real estate. You can also invest in other things such as traditional investments, precious metals, and cryptocurrencies.

- Tax-free or tax-deferred growth, depending on if the account is a traditional IRA or a Roth IRA.

- If you have a Self-Directed Roth IRA for real estate, you can move into the property after turning 55 ½ and the account has been open for five years.

- The ability to invest in different types of real estate such as commercial properties, rentals, multifamily homes, land, fractional real estate, and more!

- The variety of real estate assets available for investment, offering flexibility and potential for generating returns while benefiting from tax advantages.

- Depending on the investment you pursue, real estate may provide you with a steady stream of income flowing back to your retirement account.

- You can purchase, sell, and flip properties at your discretion.

Setting Up a Real Estate IRA

Setting up a Real Estate IRA involves several steps, including choosing the right IRA custodian, opening and funding the account, and selecting the investment property. Here are some key considerations to keep in mind when setting up a real estate IRA:

Choosing the Right IRA Custodian

When choosing an IRA custodian, it’s essential to select a reputable and experienced company that specializes in Self-Directed IRAs. The custodian will be responsible for holding and administering the IRA assets, ensuring compliance with IRS rules and regulations, and providing customer support. Look for a custodian that offers competitive fees, flexible investment options, and excellent customer service. A good custodian can make the process of managing your IRA smoother and more efficient, allowing you to focus on your investment strategy.

Opening and Funding the Account

To open a Real Estate IRA, investors will need to complete an application and provide required documentation, such as identification and proof of income. All of this can be done on the IRA Financial app. Once the account is open, investors can fund it with a rollover from an existing IRA or 401(k) plan, or with annual contributions. The account can be funded with cash, and investors can also use non-recourse loans to finance the purchase of investment property. It’s important to ensure that all funding methods comply with IRS regulations to avoid any potential penalties.

What Real Estate Investments Can I Make with a Self-Directed IRA?

Your Self-Directed IRA offers flexibility to hold a wide variety of real estate-related assets, subject to IRS rules. Some common real estate investment types include:

- Residential rental properties (single-family homes, duplexes, condos)

- Commercial properties (office, retail, warehouse)

- Raw land

- Vacation rentals / short-term rentals (if managed passively and following IRS rules)

- Real estate notes or mortgages

- Tax lien certificates and tax deed investments

- Fractional real estate offerings or crowdfunded real estate funds

Because the investment is held inside the IRA (not personally), all income, expenses, and capital gains stay within the IRA. You cannot receive direct benefit or personal use of the property, and all day-to-day costs must be paid from IRA funds.

How Does a Self-Directed IRA for Real Estate Work?

The process of investing in real estate with a Self-Directed IRA is relatively simple. First, you need to open an account. You will need to decide whether you want to open a Custodian Controlled Self-Directed IRA or a Checkbook IRA. Generally, individuals buying fractional real estate open a Custodian Controlled IRA due to the low frequency of investments. However, individuals seeking to invest in rentals, fix and flips, or commercial properties tend to open a Checkbook IRA, which gives the investor the freedom to write checks directly from his or her IRA. It is important to have a custodian to manage real estate transactions, ensuring compliance with IRS regulations and facilitating the process efficiently.

Next, the individual will need to select the type of retirement account he or she is seeking to open. A Self-Directed IRA for real estate can be a traditional IRA or a Roth IRA. IRA Financial also allows individuals to open other types of accounts such as a Solo 401(k), SEP IRA, HSA, or Coverdell which can also be used for real estate investments.

After opening your new Self-Directed IRA, you will need to decide how to fund the account. Common ways to fund a Self-Directed IRA include:

- Transferring an existing IRA or 401(k)

- Rolling over existing retirement accounts.

- Making annual contributions. These contributions can be made yearly with contribution limits established by the IRS.

How to Buy Real Estate with Your IRA: Step-by-Step

Investing in real estate through your IRA involves more steps than traditional investing, because of IRS rules and the need for proper structuring. Here’s a step-by-step guide:

- Set up a Self-Directed IRA aligned with real estate investing

Choose a custodian, such as IRA Financial, that allows alternative assets (like real estate). - Fund the IRA

Use transfers, rollovers, or contributions to move money into the IRA so it has purchasing capacity. - Identify the property

Do due diligence: location, condition, market rates, zoning, title. - Make the purchase in the IRA’s name

The property deed must read “XYZ IRA, custodian as trustee” — never in your personal name. - Use nonrecourse financing if borrowing

If the IRA needs a loan, it must be nonrecourse. This ensures the lender cannot go after IRA other than the property itself. - Close and title properly

The IRA (or IRA-owned entity) handles all documentation. No personal funds or signatures can be used. - Manage and maintain through the IRA

All expenses—repairs, taxes, insurance—must be paid from the IRA. All income (rent) must flow back into the IRA. - Plan for exit or sale

When selling, profits remain in the IRA; if debt was used, the portion of gain tied to borrowing may trigger UBTI/UDFI.

Ways to Purchase Real Estate with a Self-Directed IRA

Direct Purchases

Retirement investors who want to invest directly in rental properties must have the knowledge to form the following plans:

- Finding the property

- Verifying that it is a good deal

- Financing the property

- Managing the property

It is crucial to understand IRS rules that prevent self-dealing when investing in a rental property through a self-directed IRA.

Indirect Purchases

Retirement investors who do not feel equipped for the rigors of direct real estate investing can invest indirectly through REITs (real estate investment trusts), crowdfunding websites, private notes, or through a silent partnership such as Seller Financing.

Strategies for Real Estate Investing with a Self-Directed IRA

When using a Self-Directed IRA or Checkbook IRA to make a real estate investment, there are a number of ways you can structure the transaction:

1. Use your Self-Directed IRA funds to make 100% of the investment

If you have enough funds in your Self-Directed IRA to cover the entire real estate purchase (including closing costs, taxes, fees, insurance, etc.) you may make the purchase outright using your IRA. You pay all ongoing expenses relating to the real estate investment out of your IRA bank account. All income or gains relating to your real estate investment must return to the IRA.

For the new real estate investor, it is crucial to explore various real estate assets that align with your industry knowledge and investment goals, as these investments can offer significant advantages, such as tax benefits.

2. Partner with family, friends, and colleagues

If you don’t have sufficient funds in your IRA to make a real estate purchase outright, your Self-Directed IRA can purchase an interest in the property along with a family member who is a non-disqualified person. You can also purchase with a friend or colleague. The investment will not be made into an entity owned by the IRA owner. Instead, it’s invested directly into the property.

For example, your Self-Directed IRA can partner with a non-disqualified family member, friend, or colleague to purchase a piece of property for $150,000. Your Self-Directed IRA can purchase an interest in the property (for example, 50% for $75,000) and your family member, friend, or colleague can purchase the remaining interest (50% for $75,000).

All income or gain from the property will be allocated to the parties in relation to their percentage of ownership in the property. Likewise, all property expenses must be paid in relation to the parties’ percentage of ownership of the property.

Based on the above example, for a $2,000 property tax bill, the Self-Directed IRA will be responsible for 50% of the bill ($1,000). The family member, friend, or colleague is then responsible for the remaining $1,000 (50%).

We’ll discuss more on partnering with family, friends, and colleagues later in this article.

3. Borrow money for your Self-Directed IRA

You may obtain financing through a loan or mortgage to finance a real estate purchase using a Self-Directed IRA. However, you must consider two important points when selecting this option:

Option 1

1. If the IRA purchases real estate and secures a mortgage for the purchase, the loan must be non-recourse. Otherwise, there will be a prohibited transaction. A non-recourse loan only uses the property for collateral. In the event of default, the lender can collect only the property and cannot go after the IRA itself.

Option 2

2. Tax is due on profits from leveraged real estate. If your IRA uses non-recourse debt financing (i.e., a loan) on a real estate investment, some portion of each item of gross income from the property is subject to Unrelated Business Income Tax (UBTI). This is pursuant to Code Section 514. “Debt-financed property” refers to borrowing money to purchase real estate. For example, a leveraged asset is held to produce income.

In such cases, only the income attributable to the financed portion of the property is taxed. Gain on the profit from the sale of the leveraged assets is also UDFI. However, it is not Unrelated Debt Financing Tax (UDFI) if the debt is paid off more than 12 months before the property is sold.

There are some important exceptions from UBTI. Those exceptions relate to the central importance of investment in real estate from the sale of real estate. This includes:

- Dividends

- Interest

- Annuities

- Royalties

- Most rentals from real estate

- Gains/losses

However, rental income the real estate generates that is “debt-financed” loses the exclusion. That portion of the income becomes subject to UBTI. Thus, if the IRA borrows money to finance the purchase of real estate, the portion of the rental income attributable to that debt will be taxable as UBTI.

Let’s assume the average acquisition indebtedness is $50: the average adjusted basis is $100.50 percent of each item of gross income from the property is included in UBTI.

Real Estate IRA Loans & UBTI / UDFI Consequences

Using leverage (a mortgage or loan) inside a real estate IRA is allowed—but comes with critical constraints and tax implications:

- Loan must be nonrecourse: The lender’s only recourse in default is the property itself, not other IRA assets.

- Debt-financed portion triggers UDFI / UBTI: Income or gains tied to the financed portion is subject to Unrelated Debt-Financed Income (UDFI), a subset of UBTI.

- Proportionate allocation: If you borrow 40% of the purchase price, 40% of rental income and gain is considered UBTI.

- 12-month rule for sales: If debt is fully paid off more than 12 months before sale, the gain attributable to that debt is excluded from UDFI.

- Liquidity requirement: Your IRA must hold cash to pay interest, taxes, maintenance, and UBTI tax — you can’t use personal funds.

Example: Your IRA buys a $200,000 rental property with $80,000 nonrecourse debt (40% leverage). If annual gross rent is $12,000, then $4,800 (40%) may be treated as UBTI, subject to tax after expenses.

Book a free call with a self-directed retirement specialist

- Review your self-directed retirement options

- Learn about investing in alternative assets

- Get all of your questions answered

Why Tax-Free Beats Tax Deductions

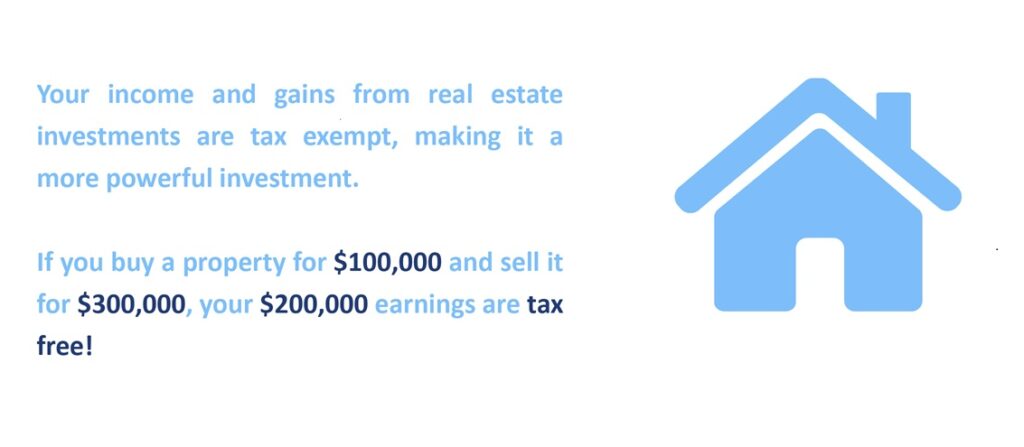

For years, real estate investors have focused on tax deductions like depreciation and long-term capital gains treatment when buying property with personal funds. But a Self-Directed Roth IRA offers something even more powerful: the ability to eliminate taxes altogether—both on rental income and future appreciation. By using retirement dollars to buy real estate outright, investors can sidestep capital gains taxes and depreciation recapture, resulting in dramatically higher after-tax profits over time.

While personal ownership provides short-term tax benefits, those gains are often offset by long-term liabilities. With a Self-Directed Roth IRA, your returns grow tax-free, your profits remain untouched, and your wealth compounds without tax drag. Even Traditional IRAs offer tax-deferred growth and potentially lower taxes in retirement. The bottom line: smart investors aren't just chasing deductions—they're building permanent, tax-free income for the future.

A Real-World Example

Let’s say you buy a $300,000 rental property with cash. It earns $24,000 in rent annually and costs about $6,000 a year to maintain. You sell it in 10 years for $450,000. You’re in the 35% tax bracket and 20% capital gains bracket.

Scenario A: You use a Self-Directed Roth IRA

- All rental income is tax-free ($18,000/year x 10 = $180,000)

- Appreciation gain of $150,000 is also tax-free

- Total taxes paid: $0

- Total after-tax profit: $330,000

Scenario B: You use personal funds

- After depreciation, you’re taxed on $7,000/year of income

- You pay ~$2,450/year in taxes = $24,500 over 10 years

- When you sell, you owe ~$30,000 in capital gains + ~$27,500 in depreciation recapture

- Total taxes paid: $82,000

- Total after-tax profit: $248,000

Net difference: $82,000 more in your pocket with the Roth IRA

Managing Real Estate Investments

Once the Real Estate IRA is set up and funded, investors will need to manage the investment property to ensure it generates rental income and appreciates in value. Here are some key considerations to keep in mind when managing real estate investments:

Property Management

Property management involves overseeing the day-to-day operations of the investment property, including collecting rent, handling maintenance and repairs, and managing tenant relationships. Investors can hire a property management company to handle these tasks, or they can manage the property themselves. It’s essential to ensure that the property is managed in compliance with IRS rules and regulations, and that all income and expenses are properly reported.

Investors should also consider hiring a real estate attorney to review the property purchase agreement and ensure that the transaction is structured correctly. Additionally, consulting with a tax professional can help ensure that you are taking advantage of all available tax benefits and complying with IRS rules and regulations. By following these steps and considering these key factors, investors can successfully set up and manage a real estate IRA, potentially earning rental income, appreciating in value, and enjoying tax benefits.

UBTI Tax Rates

In most cases, when you use a retirement plan to make investments, you do not generate tax in the case of a Roth IRA, or the taxes will be deferred until a distribution, such as a Traditional or Self-Directed IRA. However, there are certain instances where you will trigger a tax known as the Unrelated Business Taxable Income (UBTI) tax. If you use retirement funds in a real estate transaction that involves a non-recourse loan, you will trigger the UBTI tax. In that case, it’s important to note that a Self-Directed IRA subject to UBTI is taxed at the trust tax rate. This is because an IRA is considered a trust. For 2025, a Self-Directed IRA LLC subject to UBTI is taxed at the following rates:

- $0 – $2,550 = 10% of taxable income

- $2,551 – $9,150 = $255 + 24% of the amount over $2,550

- $9,151 – $12,500 = $1,839 + 35% of the amount over $9,150

- $12,501 + = $3,011.50 + 37% of the amount over $12,500

Partnering with a Family Member in a Real Estate Transaction – Prohibited Transaction?

Partnering with a family member is likely not prohibited if the transaction is structured correctly. Investing in an investment entity with a family member and investing in an investment property directly are two different transaction structures that impact whether the transaction will be prohibited under Code Section 4975.

The different tax treatment is based on who currently owns the investment. Using a Self-Directed IRA to invest in an entity that a family member owns (and is a disqualified person) will likely be treated as a prohibited transaction.

However, partnering with a family member that is a non-disqualified person directly into an investment property is likely not a prohibited transaction. It’s important to note that if you, a family member, or another disqualified person already owns a property, then investing in that property with your Self-Directed IRA would be prohibited.

What Disqualifies Real Estate Held in an IRA?

Not all real estate strategies are allowed inside an IRA. Be careful to avoid disqualified/prohibited transactions, which can void the tax benefits.

Some key disqualifying activities include:

- Personal use or occupancy: You or any disqualified person (spouse, ancestors, descendants) cannot live in or use the property.

- Selling to or buying from you or disqualified persons: The IRA cannot transact with the account holder or close family.

- Direct benefits to disqualified persons: No lease, favorable terms, or improvements that benefit disqualified persons.

- Commingling funds: You cannot mix personal money with IRA property; all expenses and income must flow through the IRA.

- Unauthorized improvements with personal funds: You can’t personally pay for repairs or improve the property with personal funds; IRA must cover these.

If a prohibited transaction is declared by the IRS, the IRA’s real estate investment could be disqualified, causing taxes and penalties.

Common Pitfalls to Avoid in Real Estate IRA Investing

While investing in real estate via your IRA offers compelling tax benefits, it also comes with traps. Watch out for these common mistakes:

- Lack of proper planning at sale: Timing debt payoffs and understanding UDFI implications on gains is essential.

- Underestimating maintenance or vacancy costs: The IRA must cover all property expenses—even in vacancy periods.

- Insufficient liquidity: Without cash in the IRA, you may be forced to liquidate assets for taxes or repairs.

- Triggering UBTI/UDFI unexpectedly: Using leverage or active business operations without planning can cause tax surprises.

- Violation of prohibited transaction rules: Personal benefit, commingling, or dealing with disqualified persons can cause severe penalties.

- Poor due diligence: Not checking title, zoning, liens, or property condition is risky—especially since the IRA is the owner.

- Failure to title properly: The deed must always list the IRA or IRA-owned entity—if titled incorrectly, you risk personal liability or disqualification.

Conclusion

Investing in real estate with a Self-Directed IRA gives you the power to diversify your portfolio, take control of your retirement, and invest in assets you understand best. Whether you’re drawn to rental properties, commercial buildings, or raw land, a Real Estate IRA allows your investments to grow tax-deferred—or even tax-free—while staying within IRS rules.

While real estate inside an IRA offers tremendous long-term potential, it also requires careful planning and strict compliance. Understanding prohibited transactions, UBTI, and the role of a qualified custodian ensures that your investments remain protected and fully tax-advantaged.

At IRA Financial, we’ve helped thousands of investors unlock the flexibility and tax benefits of self-direction. With the right structure—such as checkbook control through an IRA LLC—you can act quickly on opportunities, eliminate unnecessary custodial delays, and build lasting wealth on your terms.

Ready to Put Your IRA to Work in Real Estate?

Real estate remains the most common investment in a Self-Directed IRA. At IRA Financial, our experts are here to help. We have helped over 24,000 clients take back control of their retirement. However, investing in real estate can be complicated.

Schedule a Free Consultation to discuss your real estate investing goals with an expert.

Confident and ready to start? Open Your Account Today.

Frequently Asked Questions

Can I buy real estate with my IRA?

What types of real estate can an IRA own?

Can I borrow money to buy real estate in my IRA?

Can I live in or use property owned by my IRA?

Are there tax benefits (depreciation, interest deductions) when holding property in an IRA?

When I sell, how are gains taxed?

What happens if the IRS deems a prohibited transaction?

Turn Your Crypto Gains into Tax-Free Retirement Wealth with a Roth IRA in 2026

As a tech-forward investor, you see the world differently. You’re not following the herd into index funds or the next trendy ETF. Instead, you're looking ahead—at decentralized finance (DeFi), smart contracts, AI-driven assets, and blockchain protocols that promise to reshape entire industries. You thrive in volatility because you know that outsized returns require stepping outside the norm. But as you execute trade after trade on Coinbase, Kraken, or IRAfi Crypto, the excitement of profit quickly fades when you realize the IRS is taking a cut—every single time.

Every gain, no matter how small, triggers a taxable event. It’s death by a thousand paper cuts—short-term capital gains can take up to 37% of your profit if you’re in a high tax bracket. Even long-term gains don’t escape, slicing away 15–20% or more of your upside. What if there was a way to keep all of that exponential growth?

Key Takeaways

- A Self-Directed Roth IRA lets your crypto grow tax-free, avoiding capital gains on every trade and maximizing long-term returns.

- Unlike regular plans, SDIRAs give you full control to buy, hold, and trade real crypto—not just ETFs or related stocks.

- If you’re bullish on crypto’s future, a Roth IRA is the smart, long-term strategy to turn belief into lasting, tax-free wealth.

The Problem with Standard Crypto Trading: The Inevitable Tax Bill

Crypto can reward strong returns, but taxes can reduce them quickly. The IRS treats cryptocurrency as property, so selling or exchanging it typically triggers a taxable event.

If you buy Ethereum (ETH) at $1,800 and sell at $2,400, the $600 gain is taxable. If held for one year or less, it is taxed at ordinary income rates, up to 37% depending on your bracket. If held longer than one year, it qualifies for long-term capital gains rates, generally 0%, 15%, or 20% based on income.

Even swapping one cryptocurrency for another can create a taxable gain. Without proper planning, taxes can take a meaningful share of your returns before they have the opportunity to compound.

Now imagine you’re an active trader, flipping tokens weekly or even daily. Maybe you're rotating out of BTC into ETH, then taking a shot on a small-cap gem like INJ, AVAX, or RUNE. Each profitable move triggers a new tax liability—even if your entire portfolio ends the year in the red. That’s the kicker: you can owe taxes on realized gains while losing money overall.

This is the paradox of active crypto investing in a taxable environment. Your strategy may be airtight, your timing perfect—but after-tax, your gains shrink. What should’ve been a breakout year becomes just an expensive lesson in tax inefficiency.

Worse still, this constant tax friction changes behavior. It discourages long-term thinking and tempts investors into short-term trading based on tax seasons instead of conviction. And in a space where asymmetric returns reward patience, that's a losing game.

Without a tax-sheltered vehicle, you’re essentially growing someone else’s wealth—the government’s!

The Roth IRA: Your Ultimate Weapon for Tax-Free Growth

Enter the Roth IRA, the most misunderstood but powerful wealth-building vehicle in the U.S. tax code. While traditional IRAs offer an up-front tax deduction, the Roth flips that script. You pay taxes now on contributions, but from there, all gains grow—and are withdrawn—completely tax-free assuming certain conditions are met.

Think about that for a moment: If your $5,000 Roth contribution grows into $500,000 from early Etherum investments—or the next Solana, Chainlink, or Ordinals play—you’ll never owe a cent of tax on it. Not today, not ever.

That’s why Roth IRAs are the secret weapon of the financially literate. For those who believe in the exponential future of decentralized technologies, putting crypto in a Roth IRA is like turbocharging your retirement—without handing your upside to the IRS.

Unlocking Crypto with a Self-Directed Roth IRA

But here’s the frustrating reality: most traditional financial institutions still treat crypto like a liability, not an opportunity. These are the same firms that were slow to embrace online trading, skeptical of ETFs in their early days, and now—predictably—skeptical of digital assets. Try opening a Roth IRA at Vanguard, Fidelity, or Schwab and buying actual Bitcoin. Spoiler: you can’t.

At best, you’ll find crypto-themed products—think ETFs or funds that hold stock in crypto-adjacent companies like Coinbase or Nvidia. But let’s be honest: that’s not the exposure you want. Buying a Blockchain ETF is like investing in a gold mining company when what you really want is physical gold. It’s indirect. It's diluted. And it’s disconnected from the decentralized revolution you believe in.

That’s where the Self-Directed IRA flips the script. It gives you full autonomy over your retirement capital—no gatekeepers, no narrow menus, and no watered-down exposure. Want to buy and hold Bitcoin long-term? No problem. Interested in Ethereum's future as the foundation for DeFi and NFTs? You got it. Looking to speculate on high-upside Layer 1s like Solana, Avalanche, or other altcoins? That’s on the table too.

With a provider like IRA Financial, which helped pioneer crypto investing inside tax-advantaged accounts, you're not just opening an IRA, you’re unlocking a customizable, blockchain-native portfolio that grows tax-free. This isn’t a traditional financial product retrofitted for crypto—it’s a crypto-first strategy designed to take full advantage of the Roth IRA’s power.

Best of all, you maintain control—not just of your investment decisions but also of custody. Many investors choose secure, institutional-grade custodians who handle private key management and cold storage, while others prefer to use multi-signature wallets for added control. And the reward? If your crypto thesis plays out—if that $10,000 Bitcoin investment grows into $500,000 over the next decade? You keep it all! No capital gains tax. No selling-season calculations. Just clean, compounding growth that stays in your hands, not the IRS’s.

This is what a true forward-thinking financial structure looks like—freedom, control, and zero tax on upside.

Traditional vs. Roth Crypto IRA: A Quick Comparison

Here’s a deeper breakdown of which structure may work best for you:

| Feature | Traditional SDIRA | Roth SDIRA |

|---|---|---|

| Tax on Contributions | Pretax (lowers taxable income today) | After-tax (no deduction) |

| Tax on Growth | Tax-deferred | Tax-free |

| Tax on Withdrawals | Ordinary income rates | 100% tax-free assuming they are qualified |

| Best For | High earners wanting immediate deduction; shorter time horizons | Long-term investors expecting high growth and higher future tax brackets |

| Crypto Use Case | Conservative, stablecoins or yield strategies | High-growth plays like altcoins, NFTs, DeFi |

Bottom line: If you're 20–40 years old and bullish on crypto’s long-term trajectory, a Roth SDIRA can be a generational wealth-building engine!

Addressing Your Concerns: Security and Simplicity

Security: You’ve read the headlines: exchanges getting hacked, users losing private keys, rug pulls. Security is non-negotiable. That’s why institutional-grade custody is at the core of any serious crypto IRA platform. IRAfi leverages regulated custodians and battle-tested wallet technology to store your assets safely—offline, in cold storage, and away from prying eyes.

Simplicity: Worried that this sounds complicated? It’s not. A quality SDIRA provider makes on-boarding easy. Account setup, rollover paperwork, compliance—handled. You focus on the part that matters: identifying high-conviction crypto opportunities. Think of it like Coinbase meets Fidelity—crypto-native trading in a tax-advantaged wrapper.

Book a free call with a self-directed retirement specialist

- Review your self-directed retirement options

- Learn about investing in alternative assets

- Get all of your questions answered

The Verdict: Don’t Just Invest in the Future—Secure Its Gains

You already believe in the future. You’ve put in the time—reading whitepapers, listening to podcasts, following the dev updates on GitHub. You've stayed up during overnight market cycles, held through volatility, and placed bold bets on the technologies reshaping finance, identity, and ownership. But bold investing without smart tax planning? That’s like racing a Ferrari with the parking brake on—powerful potential, constantly held back by unnecessary friction.

That’s where the Self-Directed Roth IRA comes in. It’s not just a retirement account, it’s an optimization engine. A vehicle purpose-built for those who think long-term, believe in exponential growth, and don’t want to share the upside with the IRS. It’s the bridge between your investment vision and the kind of wealth that changes not just your future, but your freedom.

When you invest through a Roth IRA, you're not just hoping crypto will moon, you’re positioning yourself so that if it does, every dollar of that growth stays yours. No tax drag. No forced sales to cover IRS bills. Just clean, compounding returns inside one of the most powerful tax structures ever created. A Roth IRA that lets you own your crypto directly? That’s a wealth-building tool and a personal freedom statement all in one.

You already understand the power of decentralization. Now it’s time to apply that same philosophy to your wealth strategy: own your assets, eliminate unnecessary taxes, and invest like the future is already here.

Turn Your Crypto Gains into Tax-Free Retirement Wealth

Stop giving a cut of your profits to the IRS on every trade. With a Self-Directed Roth IRA, you can buy, hold, and trade real crypto inside a tax-advantaged account—keeping every dollar of growth for yourself.

Schedule a Free Consultation to discuss crypto in a Roth IRA.

Confident and ready to start? Open Your Account Today.

Frequently Asked Questions

What cryptocurrencies can I trade in a Self-Directed IRA?

What are the contribution limits for a Roth IRA in 2025?

What are the fees associated with a Crypto IRA?

Is my crypto insured like money in a bank?

Can I roll over an existing IRA or 401(k) into a Roth Crypto IRA?

JP Morgan vs. IRA Financial: Choosing the Right Solo 401(k) for Self-Employed Investors

In the world of self-employment, planning for retirement isn’t just a good idea, it’s a necessity. For sole proprietors, freelancers, and small business owners without full-time employees, the Solo 401(k) stands out as one of the most powerful tools for building long-term wealth. It offers high contribution limits, potential Roth benefits, and in some cases, unmatched investment flexibility.

In 2025, JP Morgan entered the Solo 401(k) space with a new offering aimed at capturing the growing market of self-employed professionals. Known for its name recognition and investment management tools, JP Morgan promises a low-cost and streamlined experience. On the other hand, IRA Financial has spent years establishing itself as a leader in the self-directed retirement plan space, offering a Solo 401(k) plan that prioritizes control, alternative investment opportunities, and IRS compliance support.

So, which one is right for you? The answer depends on how you plan to use your retirement savings—and how much control you want over your investments.

Key Takeaways

- JP Morgan’s Solo 401(k) is simple and cost-effective but limited to traditional investments like stocks and mutual funds.

- IRA Financial offers greater flexibility, flat fees, alternative asset investing, checkbook control, and advanced tax strategies.

- Choose based on your investment goals—traditional investors may prefer JP Morgan, while active or alternative investors will benefit more from IRA Financial.

JP Morgan’s New Entry Into the Solo 401(k) Market

On July 16, 2025, JP Morgan Chase expanded its Everyday 401(k) platform with a Solo 401(k) plan targeted at sole proprietors and self-employed individuals. The plan is designed to let participants set up the plan online and offers flexible investment options, ranging from JP Morgan Asset Management portfolios to custom selections.

JP Morgan’s Solo 401(k) is designed to appeal to the average investor, someone who wants to make consistent contributions into a mix of mutual funds, ETFs, or individual stocks. It integrates seamlessly with JP Morgan's existing investment platform and mobile app, providing a cohesive user experience for those already familiar with its brokerage services.

There is a $350 start-up fee for a new 401(k) plan. Additionally, there’s a $540 annual fee with a 0.15% asset fee. You can add an eligible spouse to the plan for an extra $150 yearly. Investors may still encounter trading fees, fund expense ratios, or other costs tied to the investments they select. For those focused solely on publicly traded securities and seeking a low-maintenance plan, it’s a solid option.

What the plan doesn’t offer, however, is flexibility. Because the JP Morgan Solo 401(k) is fully custodial, all investments must be made through its brokerage platform. That means no real estate, no private equity, no crypto, and no direct access to plan funds through checkbook control. For more advanced investors—or those looking to diversify beyond traditional markets—these limitations can be significant.

IRA Financial’s Self-Directed Solo 401(k): A Flexible, Open-Architecture Alternative

In contrast to JP Morgan’s simplified approach, IRA Financial’s Self-Directed Solo 401(k) is built for investors who want more control over where and how their retirement funds are used. This open-architecture plan allows for a much broader range of investment options, including real estate, private loans, tax liens, private businesses, precious metals, and even cryptocurrency. The plan also supports traditional market investments, so it’s not a matter of choosing one or the other. You can have both!

One of the key features of IRA Financial’s plan is “checkbook control.” Once the plan is set up, you can open a dedicated 401(k) bank account in the name of your plan. This gives you the ability to write checks or initiate wires directly for investments, without waiting for a custodian to approve or process transactions. For real estate professionals, private lenders, or anyone investing in time-sensitive opportunities, this direct access is a major advantage.

IRA Financial charges a flat one-time setup fee and a fixed annual maintenance fee, regardless of the size of your account or the number of investments you hold. This fee structure appeals to those with larger balances or multiple investments, especially when compared to providers who charge asset-based fees. And because there are no transaction or AUM (Assets Under Management) fees, your costs won’t increase just because your portfolio grows.

Contributions, Roth Options, and Loans: What’s the Same (and What’s Not)

Both the JP Morgan and IRA Financial Solo 401(k) plans adhere to the same IRS rules regarding contributions. For 2026, plan participants under age 50 can contribute up to $24,500 as an employee deferral. Those 50 or older can take advantage of an additional $8,000 in catch-up contributions, for a total of $32,500. In addition to the employee portion, the sponsoring business can make a profit-sharing contribution of up to 25% of compensation, with a combined maximum of $72,000 (or $80,000 for those age 50+).

Both providers also offer the ability to make Roth contributions on the employee side, which allows your contributions to grow tax free. But IRA Financial takes it a step further by including an optional in-plan Roth conversion feature. This allows you to convert pretax funds within the plan to Roth at any time—giving you more control over your tax strategy. Plus, IRA Financial allows for the Mega Backdoor Roth Solo 401(k) strategy if you want to supercharge your after-tax savings.

Another area where the two plans differ is the loan feature. JP Morgan’s Solo 401(k) currently does not support participant loans. IRA Financial’s plan includes a loan option that allows you to borrow up to $50,000 or 50% of your plan balance, whichever is less, with repayment over a five-year term. For some business owners, this flexibility can be extremely helpful when managing cash flow or seizing opportunities.

Features and Plan Flexibility

| Feature | JP Morgan Solo 401(k) | IRA Financial Solo 401(k) |

| Roth Option | ✅ | ✅ |

| In-Plan Roth Conversion | ❌ | ✅ |

| Mega Backdoor Roth | ❌ | ✅ |

| Loan Provision | ❌ | ✅ |

| Prohibited Transaction Guidance | ❌ | ✅ |

| Alternative Asset Record-Keeping | ❌ | ✅ |

| Tax Reporting | Some | ✅ |

| IRS & DOL Audit Support | ❌ | ✅ |

Technology, User Experience, and Support

From a user experience standpoint, JP Morgan benefits from its sleek, modern brokerage platform and integrated mobile app. The interface is familiar, intuitive, and ideal for investors sticking to stocks and funds. However, it lacks the tools and infrastructure needed to manage alternative assets or complex transactions.

IRA Financial’s mobile platform is tailored to self-directed investors. Through its app and web portal, users can manage plan documents, initiate investments, track contributions, request loans, and even log real estate purchases. For cryptocurrency investors, they have IRAfi Crypto, a dedicated app for buying and selling more than 40 of the most popular cryptos like Bitcoin and Ethereum. While the user interface may not be as polished as a major brokerage’s, it’s built for function and flexibility—reflecting the needs of investors using their Solo 401(k)s beyond Wall Street.

Support is another key differentiator. JP Morgan offers general customer service for its accounts but does not provide specialized guidance on Solo 401(k) compliance, prohibited transactions, or complex tax questions. IRA Financial, on the other hand, specializes in retirement plans and offers support from CPAs, ERISA experts, and specialists who understand the intricacies of self-directed investing. This is especially important when dealing with real estate transactions, disqualified persons, or IRS reporting requirements.

Learn Why IRA Financial is the Better Choice for the Self-Employed!

- Review your Solo 401(k) plan options

- Learn about investing in alternative assets

- Get all of your questions answered

Who Should Choose Which Plan?

Choosing between JP Morgan and IRA Financial ultimately comes down to your investment strategy, comfort level, and need for control.

If you want a no-fuss, low-cost plan that allows you to invest exclusively in traditional assets through a familiar brokerage, JP Morgan’s Solo 401(k) is worth considering. It’s ideal for investors with relatively simple goals who value brand recognition and digital convenience.

However, if you’re looking for a retirement vehicle that can accommodate real estate, private equity, or crypto, and you want the ability to act quickly on investment opportunities without custodian delays, then IRA Financial offers far more versatility. For experienced investors and entrepreneurs who want to maximize their tax advantages while expanding beyond stocks and bonds, the Self-Directed Solo 401(k) with checkbook control is hard to beat.

Final Thoughts

JP Morgan’s entry into the Solo 401(k) space is a welcome addition for traditional investors who want a basic, affordable retirement plan. But for investors who think beyond the stock market, especially those in real estate or other alternative spaces, IRA Financial’s Solo 401(k) stands out as the more powerful and customizable solution.