Beneficiary Forms: Self-Directed IRA & Solo 401(k)

IRA Financial is recognized as the leading facilitator of Self-Directed IRA and Solo 401(k) plans. As a result, we have come across many scenarios pertaining to Self-Directed IRA and Solo 401(k) plan beneficiary forms. It's important to know the rules so that your wishes upon your passing are followed. Read more to prepare your finances better.

- A beneficiary is the person or entity that will inherit the benefits of your retirement plan

- You should name at least one beneficiary for your retirement plan(s)

- Certain situations could cause confusion when it's time to distribute your plan funds

What is a Beneficiary?

An IRA or 401(k) beneficiary can be any person or entity the owner chooses to receive the benefits of a retirement account after he or she dies. Beneficiaries of a retirement account or traditional IRA must include in their gross income any taxable distributions they receive. In general, one can designate a primary beneficiary as well secondary beneficiaries.

Primary vs. Secondary Self-Directed IRA or Solo 401(k) Beneficiary

The primary beneficiary is the first party or parties that will receive the IRA funds upon the IRA owner’s death. While, a secondary beneficiary or beneficiaries would only receive the IRA or 401(k) assets if the all primary beneficiaries are no longer alive. In addition, an IRA owner can identify one or more primary or secondary beneficiaries, but the allocation percentage should equal 100%.

The primary beneficiary is most commonly a spouse. Whereas, the secondary beneficiary are typically children. However, for individuals that are not married or do not have children, they can basically nominate any individual, charity, or third-party they desire as primary or secondary beneficiary for their IRA or 401(k).

However, if the IRA owner resides in a community property state, community property law can dictate who gets your IRA after death. The following states are community property states:

- Arizona

- California

- Idaho

- Louisiana

- Nevada

- New Mexico

- Texas

- Washington

- Wisconsin

Therefore, if an IRA owner resides in a community property state, the Self-Directed IRA owner or Solo 401(k) plan participant must take the community property state rules into account when naming a retirement account beneficiary. For example, In a community property state, an IRA owner would need the consent of the spouse in order to identify a non-spouse as primary beneficiary of the retirement account.

Who Holds the Beneficiary Form?

In the case of a Self-Directed IRA, the IRA custodian, such as IRA Financial, will hold the IRA beneficiary form. Hence, if you need to revise the beneficiary form you will need to contact the IRA custodian. Whereas, in the case of a Solo 401(k) plan, the plan administrator would hold the beneficiary form. For example, as trustee and plan administrator, the individual business owner would generally be responsible for holding the beneficiary form. Although, with respect to an employer 401(k) plan with multiple employees, the plan record keeper or third-party administrator would generally be responsible for holding the beneficiary form.

The John Jones Self-Directed IRA Beneficiary Story

One of our clients (who we will call John Jones), worked at a privately owned construction company in a southern state for 22 years. The tradesman turned supervisor named Janet Jones, his wife of 38 years, was the beneficiary of his 401(k) account in the event he died before her.

As fate would have it, Janet died first, so John updated his account paperwork, naming their three adult children as beneficiaries of the 401(k) retirement plan. Eventually he got remarried to Betty Murphy, and was on the verge of retiring. Six weeks later, at the age of 67, John Jones died.

The Rightful Beneficiary

When Mr. Jones’ children from his first marriage tried to claim the assets, believing they were named on the most recent beneficiary form, they were rebuffed by the 401(k) administrator, who then asked a court to determine the rightful owner of the money.

Under the terms of the company’s 401(k) plan, if an employee dies, the employee’s spouse has the right to the account assets, unless the spouse waives that right in writing (the priority for spouses springs from federal law).

Betty Murphy Jones had never signed such a waiver.

The new Mrs. Jones filed a motion for summary judgment, and the matter eventually ended up in federal district court, which awarded the approximately $250,000 in the account to her, disinheriting the children.

“I think John would be shocked,” said the lawyer representing the children, who are currently appealing. Neither the plan administrator nor Betty Murphy Jones would comment.

Beneficiary Rules

Here are some key rules governing retirement accounts, and lessons on how to navigate the rules as families grow and change:

Rule No. 1

With 401(k)s, your spouse is the presumed beneficiary of your account upon your death—regardless of who is listed on the beneficiary form—unless he or she previously consented to your naming someone else beneficiary. These plans are governed by the federal Employee Retirement Income Security Act, also known as ERISA. Under this law, plans can provide for spousal rights to kick in immediately, or no later than a year after the marriage.

This general rule cannot easily be circumvented with a prenuptial agreement. Only a spouse can waive the right to 401(k) plan assets—those who are engaged cannot.

If you are contemplating remarrying and are concerned about providing for children from a prior marriage, consider rolling your 401(k) to an IRA, where you have more latitude to name beneficiaries of your choosing.

Rule No. 2

If you are single when you die, your 401(k) assets pass to the person designated on your beneficiary form—regardless of what your will says or what other agreements you made before your death.

Rule No. 3

Inconsistencies Between Will & IRA Beneficiary Form

Surprisingly, it is the IRA beneficiary form that eclipses a last will and testament in the case of a conflict. Most people would think that a signed will would end up trumping an IRA beneficiary form provided by a bank or financial institution. However, that line of reasoning is incorrect. The beneficiary designation is a legally binding document and will circumvent the will. In other words, no matter what your will says and what your current relationship is with your primary beneficiary at death, the IRA beneficiary form will direct who receives the IRA funds on death even it is in conflict with your will and estate plan. As you can imagine, this can cause some nightmare type probate scenarios for the deceased IRA owner’s family.

Tips for Preventing IRA Beneficiary Disputes

Below are several tips every Self-Directed IRA holder or Solo 401(k) plan participant should consider when completing a beneficiary form:

- Review your retirement account beneficiary form each year with the IRA custodian or plan administrator and make sure it properly reflects your estate planning intentions

- Share your retirement account beneficiary form with your estate planning attorney prior to the drafting of your will

- Talk to your spouse or primary beneficiary about your estate plans, in general terms.

- Keep a copy of your IRA or 401(k) beneficiary form with your will in a safe and secure place

- Provide your primary beneficiary with information on the IRA custodian and investments made so they have the relevant information in the case of death

- If you are going through a divorce, separation, or dispute with your primary beneficiary, you should consider changing the retirement account beneficiary form immediately, even if it is only temporary.

- If you are married and thinking of naming a primary beneficiary that is not your spouse, you may want to receive written consent from your spouse in order to avert any potential future litigation

With over 60 million IRAs totaling over $32 trillion dollars in retirement funds, it is important that every retirement account owner understand the importance of having an accurate and updated retirement account beneficiary form. Failure to do so, can lead to some nightmarish probate scenarios.

IRA Financial will take care of setting up your entire IRS compliant Self-Directed IRA or Solo 401(k) Plan. Our certified specialists can handle the process by phone, email, fax, or mail – whichever means is most convenient. This process typically takes between 7-21 days to complete, the timing largely depending on the state of formation and the custodian holding your retirement funds.

Our tax and ERISA attorneys are on site, which will reduce the set-up time and cost of establishment. Most importantly, each client of IRA Financial is assigned a tax attorney to help with the establishment of the retirement plan. You will find that our fee for this service is significantly less than other companies that perform the same or similar services.

Get in Touch

If you are currently in a similar predicament as the Jones’ children and would like assistance, contact IRA Financial directly at 800-472-0646.

Rollover as Business Startup Compliance Rules

The Employee Retirement Income Security Act of 1974 (otherwise known as ERISA) and the Internal Revenue Code clearly allow for the use of retirement funds to acquire or invest in a new or existing business as long as the transaction complies with IRS and ERISA rules and regulations. Business owners have legally been using retirement funds via ROBS to help acquire or invest in a business for a number of years.

A number of promoters have promoted these types of transactions under the name “ROBS”. Even though this type of transaction is permitted under IRS and ERISA rules, the IRS believed a significant number of the promoters were not taking the necessary steps to structure a transaction that is in full compliance with IRS and ERISA rules. The ROBS rules must be adhered to so that your business funding is compliant.

What is ROBS?

Rollover as Business Startup (ROBS) is a structure that allows entrepreneurs to remove funds from a 401(k) or IRA to purchase/fund a new/existing business or franchise. The arrangement often involves rolling over a prior IRA or 401(k) plan into a newly established 401(k). A C corporation business must sponsor the new 401(k). This structure is IRS and ERISA approved.

The ongoing legal requirements of the Rollover as Business Startup structure make it difficult to ensure ROBS compliancy with the IRS. While the IRS does state that the ROBS solution is legal, it is important to receive proper legal guidance from a tax professional. The IRS has witnessed multiple instances where entrepreneurs have not been in full compliance with the IRS and ERISA rules and procedures.

Read More: Rollover Business Startups Frequently Asked Questions

Rollover as Business Startup Compliance

5 Steps to Keep Your ROBS Structure Compliant

Now that you have established the Rollover as Business Startup, you can use your retirement funds to acquire or finance a business. However, it is imperative that you keep your structure fully IRS compliant. We provide five steps to ensure complete rollover as business startup compliance.

Step 1 - Fidelity Bond

Acquire a fiduciary bond as trustee of the 401(k) plan. An ERISA fidelity bond is a form of insurance protection. In general, a fidelity bond will insure your business against losses caused by acts of fraud or dishonesty by your employees. It will protect you, as the employer, from any crimes committed by the employee.

Step 2 - Payroll

You must be an employee of the business when using 401(k) plan funds to purchase corporate stock. Your next step is to secure a payroll company to make automatic 401(k) plan contributions. Payroll companies include Paychex for HR and payroll solutions, and ADP for payroll, HR and tax services.

Step 3: Offer 401(k) Plan Benefits

If your employees are full-time (work greater than 1,000 hours/year), they should be eligible to receive 401(k) plan benefits. Depending on the features of the 401(k) plan, your company may have to make safe harbor matching contributions to eligible participants.

A Safe Harbor match is a type of 401(k) with an employer annual contribution match. With the Safe Harbor match, you will avoid most annual compliance tests. The employer will make a contribution on behalf of the employee, which is immediately vested. Contact IRA Financial about your company's Safe Harbor requirements.

Step 4: Year-End Company Valuation

Each year, you must file IRS Form 5500 for the 401(k) plan and report the value of the 401(k) plan. This is a requirement. The C corporation stock (qualifying employer securities) is owned by the 401(k) plan and typically makes up a large portion of the value of the 401(k) plan, therefore the C corporation stock must also be valued.

Consult with a qualified and independent specialist or firm to prepare the annual company fair market valuation for your company.

Step 5: Tax Returns (and other requirements)

- You must file federal and state tax returns for your C corporation by March 15.

- The annual company valuation as of 12/31 must be ready by May 1 of the following year.

- You must be on payroll and treated as an employee of the 401(k) plan and you must provide all employees with a W-2 Form.

- As trustee of the 401(k) plan, make sure you have your fidelity bond.

- Check with the state your C corporation was formed regarding annual report/fee requirements. A C corp. is a taxable entity which means you must file Form 1120.

- Have quarterly corporate board meetings and keep proper documentation of the meetings.

ROBS Rules for Clients

October 1, 2008 Memorandum

One of the ROBS rules is the ROBS Examination guidelines. On October 1, 2008, Michael Julianelle, Director of Employee Plans, signed a “Memorandum” approving IRS ROBS Examination Guidelines. The IRS stated that while this type of structure is legal and not considered an abusive tax avoidance transaction, the execution of these types of transactions, in many cases, have not been found to be in full compliance with IRS and ERISA rules and procedures. In the “Memorandum”, the IRS highlighted two compliance areas that they felt were not being adequately followed by the promoters implementing the structure during this time period.

The first non-compliance area of concern the IRS highlighted in the “Memorandum” was the lack of disclosure of the adopted 401(k) Plan to the company’s employees. The IRS believed that in too many instances the promoter was establishing a 401(k) Plan that was not adequately disclosed to all employees. Internal Revenue Code Section 401(a)(4) provides that under a qualified retirement plan, contributions or benefits provided under the plan must not discriminate in favor of highly compensated employees. In addition, the promoters were encouraging the business owner who had used their retirement funds to purchase company stock to not provide the same benefit to their employees.

The second non-compliance area of concern the IRS highlighted in the “Memorandum” was establishing an independent appraisal to determine the fair market value of the business being purchased.

Internal Revenue Code Section 4975(c)(1 )(A) defines a prohibited transaction as a sale, exchange or lease of any property between a plan and a disqualified person. Internal Revenue Code Section 4975(d)(13) provides an exemption from prohibited transaction consideration for any transaction that is exempt from ERISA Section 406, by reason of ERISA Section 408(e), which addresses certain transactions involving employer stock. ERISA Section 408(e), and ERISA Regulation Section 2550, 408e promulgated thereunder, provides an exemption from ERISA Section 406 for acquisitions or sales of qualifying employer securities, subject to a requirement that the acquisition or sale must be for “adequate consideration.”

Except in the case of a “marketable obligation”, adequate consideration for this purpose means a price not less favorable than the price determined under ERISA Section 3(18). ERISA Section 3(18) provides in relevant part that, in the case of an asset other than a security for which there is no generally recognized market, adequate consideration means the fair market value of the asset as determined in good faith by the trustee or named fiduciary pursuant to the terms of the plan and in accordance with regulations.

An exchange of company stock between the plan and its employer-sponsor would be a prohibited transaction, unless the requirements of ERISA Section 408(e) are met (the acquisition or sale of the qualifying employer securities must be for adequate consideration).

Therefore, valuation of the purchase corporate stock is a relevant issue. Since, in some cases, the company may be newly established, there could be a question of whether the stock is indeed worth the value of the purchase price exchanged. If the transaction has not been for adequate consideration, it would have to be corrected, for example, by the corporation’s redemption of the stock from the plan and replacing it with cash equal to its fair market value, plus an additional interest factor for lost plan earnings.

In addition, the IRS asserts that a valuation-related prohibited transaction issue may arise where the start-up enterprise does not actually “start-up.” Many promoters have been advising clients that they do not need to secure appraisal which would seemingly contradict the IRS’ position outlined in the “Memorandum”. In addition, the promoters who have provided clients with a valuation have been providing clients with a single line valuation statement generally approximating available retirement funds, which the IRS considers inadequate.

Compliance for ROBS - We're Here to Help

The Rollover a Business Startups Solution may have a few basic steps to get started, but don't let this trick you into thinking it is a simple structure to navigate. It is highly complex to operate prior to getting started and after you have employed the structure.

IRA Financial is always available to help guide you throughout the process and maintain Rollover as Business Startup compliance. Don't hesitate to contact us with any questions regarding the structure. Contact us via form or directly at 800-472-0646.

Romney vs. Thiel – Who is the King of the Self-Directed IRA?

The two most popular Self-Directed IRA investors are probably Mitt Romney and Peter Thiel. It is believed that Peter Thiel has a Roth IRA worth more than a billion dollars. Whereas Senator Romney is believed to have an IRA worth a few hundred million. However, in the case of Senator Romney, his IRA is pretax, while Mr. Thiel has a Roth IRA. Hence, it is not very controversial to make the case that Peter Thiel should be crowned alone as the king of the Self-Directed IRA. Nevertheless, understanding how Mr. Romney and Mr. Thiel built up their IRA wealth is a valuable exercise we can all learn from.

Romney’s Self-Directed IRA Story

Since 2019, Mitt Romney is a U.S. Senator from Utah. He served as the 70th governor of Massachusetts from 2003 to 2007 and was the Republican Party's nominee for president of the United States in the 2012 election. Prior to entering politics, Romney was a successful businessman and private equity investor. In 1984, he co-founded and led the spin-off company Bain Capital, a private equity investment firm, that became one of the largest and most successful in the country. Mr. Romney’s leadership role in Bain allowed him the opportunity, along with other executives, to co-invest alongside Bain Capital in various fund investments. Mr. Romney is believed to have been one of the first private equity-type investors to use a tax-deferred retirement account, such as an IRA, to make these investments.

Of note, at the time Romney was making his IRA investments into Bain Capital deals, the Roth IRA was not yet created, which limited Mr. Romney to pretax IRA investments.

The Roth IRA was created in 1997 by Senator Roth. Unlike a pretax IRA which provides for a tax deduction when making a contribution, IRA distributions would be subject to ordinary income tax. Whereas in the case of a Roth IRA, after the after age of 59 ½ and the Roth IRA has been open at least five years, all distributions would be tax free.

As a result of information made publicly available concerning Mr. Romney’s wealth, Mr. Romney’s IRA value is estimated between $25 million and $125 million. With his wealth estimated to be at approximately $200 million dollars, his IRA investments make up a considerable percentage. The question then becomes, how was Mr. Romney able to increase his IRA wealth so considerably over the years.

Private equity firms, such as Bain Capital, typically act as the general partner for each fund they create. The firms collect an annual management fee equal to approximately 2% of the fund during the period it is buying and restructuring companies. When companies are resold, the firm’s partners also split a percentage of the profits, known as a carried interest, which is about 20% of the returns after certain thresholds have been met.

According to several articles that reported on Mr. Romney’s IRA wealth over several years, his IRA was able to take advantage of Bain Capital's successes over the years. Romney and his co-workers invested their own money in most of the deals to increase their personal returns. Based on research performed by the Wall Street Journal, Bain Capital allowed its employees to co-invest in Bain deals with personal, as well as tax-deferred retirement accounts, such as an IRA. According to former employees, Bain Capital allowed certain employees to invest their tax-deferred IRAs into special share class that cost little but yielded much larger gains than other shares when Bain deals proved successful. According to another Wall Street Journal report, this unique investment structure allowed Bain employees to recognize a tax-deferred gain of approximately 583-fold compared to a 36-fold gain recognized by Bain over the same period.

According to internal documents and securities filings, Bain Capital investments that involved tax-deferred retirement accounts were typically structured as follows:

Bain Capital would offer two classes of stock, usually called Class L and Class A. Mr. Romney and Bain Capital would typically use their IRAs to purchase the Class A shares. Because Bain Capital controlled the investment companies, it had flexibility in assigning values to the classes. For example, Class L shares, akin to preferred stock, were safer and had a higher initial value. They had priority if the company paid dividends, and holders of these shares were the first to receive proceeds from a sale or liquidation. The shares also accrued interest, often at 10% to 12%. Whereas, Bain Capital assigned a much lower value to Class A shares, which were riskier but potentially more profitable.

If Bain Capital sold or liquidated a company it had taken over for less than was owed to Class L shareholders, the Class A shares lost all their value. But once Class L shareholders got their money, Class A shareholders received the bulk of additional gains, often as much as 90% of them, according to the documents and former employees. In successful deals, the A shares could skyrocket and if they were owned by a tax-deferred arrangement, such as an IRA, the gains would be tax-deferred.

Based on the above structure, Mr. Romney and certain Bain executives were able to use their IRA to invest in low-valued Class A shares that had very high upside on a capital or liquidation event. This structure allowed Mr. Romney to generate significant IRA returns in conjunction with the investment into Class A shares. Mr. Romney reportedly used this type of structure in multiple occasions, which contributed to the surge in value of his IRA.

Thiel's Self-Directed Roth IRA Story

Peter Thiel, a Stanford law graduate, ran a small hedge fund in the late 1900s. In 1999, single taxpayers were only allowed to contribute to a Roth if they made less than $110,000. Thiel’s income that year was $73,263, IRS records show. Like many startups, PayPal offered its top executives low initial salaries and large stock grants. While SEC filings describing that time don’t mention Thiel’s Roth, they show that he bought his first slice of the company in January 1999. Thiel paid $0.001 per share for 1.7 million shares. At that price, he was able to buy a large stake for just $1,700 of Roth IRA funds.

According to a Pro Publica article on Mr. Thiel’s IRA, all PayPal employees got the same “below fair market value” pricing which is what the IRS acknowledged when they audited Thiel in 2012. And soon after the company sold him the shares, investors invested millions of dollars into the company. In just a month’s time, the company sold a slice of itself to investors for $500,000. That June and August, another $4.5 million poured in from the venture fund arm of telecom giant Nokia and other investors, those records show.

In just a year’s time, the value of his Roth jumped from $1,664 to $3.8 million — a 227,490% increase. Then in 2002, eBay purchased PayPal. That same year, Thiel sold the shares, still inside his Roth. The tax-free proceeds poured into his account. By the end of 2002, Thiel’s Roth was worth $28.5 million.

In 2003, Thiel and colleagues founded Palantir, a data analytics company. Thiel used his Roth to buy shares of Palantir when it was still a private company, years before it was listed on the New York Stock Exchange, according to a ProPublica analysis of tax records.

In 2004, Thiel met Mark Zuckerberg, a Harvard undergraduate who had come to Silicon Valley for the summer to work on growing the company that would become Facebook. Thiel invested $500,000, Facebook’s first large outside infusion of cash. Thiel invested in Facebook using his Roth IRA. By the end of 2008, the Roth was worth $870 million.

Ironically, the IRS and many of Thiel’s adversaries spent time focusing on his PayPal investment, however, it was his Palantir and Facebook investments that generated the largest returns for his Roth IRA.

Did Romney or Thiel Violate the IRS Prohibited Transaction Rules?

An IRA is an individual retirement account taxed under Internal Revenue Code Section 408, when it comes to using IRA funds to invest in transactions involving a “disqualified person," one must first examine the prohibited transaction rules. In general, these rules state that the IRS has restricted and imposes a penalty on certain transactions between the IRA and a disqualified person. The rationale behind these rules was a congressional assumption that certain transactions between certain parties are inherently suspicious and should be disallowed.

The definition of a disqualified person extends into a variety of related party scenarios, but generally includes the IRA owner, any ancestors or lineal descendants of the IRA holder, and entities in which the IRA holder holds a controlling equity or management interest. To trigger the prohibited transaction rules, a direct transfer of funds between the IRA and a disqualified person need not occur. A disqualified person could trigger a prohibited transaction by either engaging in a self-dealing or conflict of interest transaction.

In the case of a transaction involving private stock, based off the GAO Report from 2014, there are essentially only two ways the IRS can attack the transaction and argue it violated the IRS prohibited transaction rules. The first is if the company is controlled 50% or more by the IRA owner of any disqualified person. The second is if the price paid for the shares by the IRA was below market.

The Case for Mr. Romney

Mr. Romney was a disqualified person with respect to his IRA because he was a fiduciary of his IRA. The question then becomes was Romney’s use of his IRA funds to co-invest with Bain Capital as a self-dealing or conflict of interest transaction under the rules. It is believed that he owned less than 50% of Bain Capital and, thus, Bain Capital or any of its controlled companies would likely not be considered a disqualified person.

Bain Capital allowed certain employees to invest their tax-deferred retirement accounts (IRA) into special Class A shares that cost little but yielded much larger gains than other shares when Bain deals proved successful. Could this investment structure be construed by the IRS has creating a conflict of interest for Mr. Romney since the Class A shares would benefit at the expense of the Class L shareholders.

The key analysis here is whether all investors paid the same price for Class A shares. Based on the information reported, the Class A shares had different economic terms than the Class L shares, including higher risk, but also higher upside, and the Class L shares were structured more like preferred shares. Preferred shares have a higher initial value because holders of this share class are more likely to be repaid if the portfolio company is not successful. Additionally, holders of preferred shares are the first to receive proceeds from the private equity fund’s sale of the portfolio company. In contrast, the riskier common shares can end up worthless if the private equity fund sells the portfolio company for less than it paid. But if the portfolio company is sold for a higher price than expected, holders of the riskier common shares may receive the bulk of any additional proceeds once preferred shareholders have received their proceeds.

That being said, it would seem plausible that if the IRS was able to audit the Romney IRA transactions within the three-year statute if limitations, an argument could have been made that the Class A shares were structured to provide Mr. Romney’s and other IRA holders’ a financial advantage at the expense of Bain Capital investors, which could be considered a conflict of interest. Thankfully for Romney, the IRS apparently did not have the opportunity to audit those transactions.

The Case for Mr. Thiel

In general, an IRA should not be used to invest in a business if the IRA owner or disqualified person owns greater than 50% of the business interests or stock. Although, even if the Roth IRA owns less than 50% of the business, including personal and IRA interests, the IRS could still potentially argue that the Roth IRA investment was a self-dealing or conflict of interest prohibited transaction under IRC 4975. However, that would be highly difficult in the case where the IRA was investing a trivial amount of money into a company with numerous founders and investors. In the case of Thiel, based on the information reported by Pro Publica, he owned less than 50% of the shares of PayPal, Facebook, and Palantir. In addition, the amount invested in all three companies were relatively minor.

In Notice 2004-8, the IRS highlighted a type of transaction involving a Roth IRA and company stock that they have listed as abusive. In general, the transactions were structured as follows: an individual owns a preexisting business and sells substantially all the company shares to a Roth IRA owned by the business owner. The acquisition of shares is far below fair market value and thus have the effect of shifting value into the Roth IRA. The IRS is very concerned with a taxpayer’s ability to shift taxable assets into a tax-free account and, thus, shielding the gains on the stock appreciation from tax.

For Mr. Thiel’s acquisition of PayPal shares, the ProPublica article stated that the SEC filings revealed that his PayPal founders’ shares were among those the company sold to employees at “below fair value.” However, the record revealed that all employees got the same “below fair market value” pricing which is what the IRS acknowledged when they audited Thiel in 2012. Hence, since all employees were able to buy the PayPal shares at that time for the same price, Thiel’s Roth IRA did not get a below market deal on the investment.

In the case of his Facebook investment, his Roth IRA paid the fair value price offered by the company at that time. Since Mr. Thiel's Roth IRA invested into companies, he, nor any disqualified person, owned more than 50%, and paid value for the shares purchased, like any other employee/investor at that time, his Roth IRA investments into PayPal, Facebook, and Palantir were likely not prohibited transactions under the Code.

Conclusion

Mr. Romney and Mr. Thiel are surely two or the ore prominent members of the Self-Directed IRA Hall of Fame, but they are not alone. More than 28,600 taxpayers held IRAs larger than $5 million in 2019, according to a Joint Committee on Taxation analysis published in July, although they account for less than a tenth of 1% of the roughly 70 million taxpayers with a traditional or Roth IRA, according to most recent IRS figures. Almost 500 people have IRAs larger than $25 million in which the accounts average about $150 million.

Understanding how Romney and Thiel built up their IRA values is a worthwhile experience. This is especially true of Mr. Thiel who used the power of the Roth IRA to build a billion-dollar tax-free dynasty. In contrast, since Mr. Romney is now over the age of 73, he is obligated to take required minimum distributions on his pretax IRA, which would be subject to ordinary income tax. However, Thiel's Roth will enjoy tax-free distributions and no RMD requirement.

Overall, Peter Thiel is the king of the Self-Directed IRA for understanding the enormous tax benefits of using a Roth for private stock investments. Imagine being a founder or early investor into three successful publicly-traded companies, including Facebook, and making all these investments with a tax-free retirement account. Pretty amazing!

Mr. Romney still has a lot to be proud of. He was one of the first private equity investors to use a tiered class structure that potentially could create extraordinary upside to its IRA class investors. Unfortunately, Mr. Romney has the misfortune of making most of his IRA investments prior to the creation of the Roth IRA. Nevertheless, all IRA investors can learn a lot from both Mr. Romney and Mr. Thiel.

Self-Directed Coverdell ESA vs. the 529 Plan

With the price of education soaring in this country, it is more important than ever for parents and family members to think about saving for educational costs for their children or loved ones. The good news is that Congress has come up with two types of specific educational savings plan that can help Americans better save for education costs, including elementary, secondary, college, and even graduate school.

This article will explore the advantages and disadvantages of the Coverdell Education Savings Account (ESA) and the 529 plan. Both plans have great tax and savings benefits, but have different eligibility requirements, as well as distinct restrictions. Hence, it is important that everyone understands the power of saving for education via a Coverdell or 529 plan, and fully comprehends which plan may be the better fit.

- With education costs at an all-time high, Americans need ways to save

- Tax-advantaged accounts, such as the Coverdell ESA and 529 Plan, offers one the ability invest funds earmarked for education

- Although the plans are similar, each have their own advantages (and drawbacks)

The Coverdell ESA

A Coverdell ESA is custodial account set up solely for paying qualified education tuition and expenses for the designated beneficiary of the account. Like an IRA, the account must be set up with a bank, financial institution, or state-chartered trust company, such as IRA Financial. The savings benefit associated with a Coverdell applies not only to qualified higher education expenses, such as a university, but also to qualified elementary and secondary education expenses.

Who Can Set Up a Coverdell?

A Coverdell account can only be established by a beneficiary that is under the age of 18. In other words, the account must be established for the sole benefit of the child. Coverdell assets are not revocable. As discussed above, the Coverdell must be established by a custodian, such as IRA Financial, much like an IRA.

How Much can I Contribute to a Coverdell Annually?

The primary purpose of making contributions to a Coverdell is to help finance the beneficiary's qualified education expenses. Contributions must be made in cash and are not tax deductible. For both 2023 and 2024, the maximum contribution amount is $2,000. There's no limit to the number of accounts that can be established for a particular beneficiary under the age of 18, however, the total contribution to all accounts on behalf of a beneficiary in any year may not exceed $2,000.

In addition, to make an annual Coverdell contribution, one’s income must be below $110,000 for a single taxpayer and $220,000 for a married couple filing jointly. Coverdell contributions must be made by April 15.

What Investments Can I Make with a Coverdell?

A Coverdell account may be self-directed just like an IRA. Therefore, other than life insurance, collectibles, and certain transactions involving a “disqualified person” under Internal Revenue Code Section 4975, the Coverdell is permitted to make any investment. For example, a Coverdell may invest in stock, bonds, real estate, gold, cryptos, private business investments, and much more. Also, like an IRA, all income and gains from the investment would flow back to the Coverdell without tax. This is known as tax-deferral.

Coverdell Distributions

Distributions from a Coverdell must always be paid to the beneficiary and must only be used for qualified education purposes. They cannot come back to the individual that made the contributions or set up the account. Unspent Coverdell funds remaining in the account when the beneficiary reaches the age of 30 must be distributed at that time, subject to tax and a 10% penalty on the account growth if he or she does not have qualified education expenses in that year. However, the Coverdell beneficiary can be changed to another family member below the age of 30 without triggering tax or penalty.

The 529 Plan

A 529 Savings plan is also known as a “qualified tuition program.” Unlike a Coverdell, which is a federal savings plan, a 529 plan is a state-sponsored savings plan that provides a few tax benefits. There are two main types of 529 plans: Section 529 prepaid programs and Section 529 savings programs. The 529 prepaid plan is not as popular as it is currently only offered in 10 states.

Who Can Set Up a 529 Plan?

Unlike a Coverdell plan which has income restrictions, anyone can establish a 529 plan; there are no income restrictions. One of the primary advantages of a 529 plan is its flexibility. It has only minor limitations, offer tax benefits like a Coverdell, and is designed to help families pay for college, as well as elementary and secondary school tuition, but not expenses.

How Much Can I Contribute to a 529 Plan?

Unlike an IRA or a Coverdell, the IRS does not set annual contribution limits for 529 Plans. Conversely, the annual contribution limits for 529 plans are set by the state. In general, contribution limits for 529 plans typically range from $250,000 to around $500,000 per beneficiary. In other words, the total amount of contributions that can be made to a beneficiary’s 529 plan is capped in the aggregate by the state. This is a lifetime contribution limit and not an annual limit. In addition, earnings from the contributions can exceed the state annual contribution limit. It is also important that the state annual contribution limit is per child.

What Investments Can I Make with a 529 Plan?

Unlike a Coverdell, a 529 plan cannot be self-directed; the states require that a 529 plan can only be invested in traditional investments, such as stocks, bonds, ETFs, and mutual funds. To this end, 529 plans are typically professionally managed by experienced investment managers at large financial institutions.

How do 529 Plan Distributions Work?

A 529 plan works much the same way as a Roth IRA and Coverdell. All contributions to a 529 plan are after-tax and are not tax deductible. All income and gains generated by the investments are not subject to tax, which allows the plan account to grow at a faster rate since the gains are not subject to tax.

Like a Coverdell, all 529 plan funds must be used to pay for qualified education costs, specifically tuition and expenses for higher education costs, but only education costs for elementary or secondary education.

Beginning in 2024, the SECURE Act 2 allows unused funds from a 529 plan to be transferred to a Roth IRA tax- and penalty-free. However, there are several limitations to keep in mind. The total lifetime amount eligible for transfer from a 529 plan to a Roth IRA is $35,000 per beneficiary. The Roth IRA must be established in the name of the 529 beneficiary. Annual contribution limits apply to transfers. For 2024, the contribution limit for IRAs, including Roth IRAs, is $7,000.

Which Plan is Best for Me?

Now that you have a solid understanding of the primary advantages of both the Coverdell and 529 Plan, below are some important considerations to keep in mind:

- If you have income above the Coverdell income threshold, then you will be limited to selecting the 529 plan.

- If you wish to make annual contributions of greater than $2,000, the 529 plan will be your best option.

- If you wish to make contributions for a beneficiary over the age of 18, then the 529 plan is better.

- If you wish to invest the educational saving funds in alternative assets, then you must go with the Coverdell.

- If you live in a state that offers a state tax deduction for 529 plan deductions, such as California, that might be better for you.

- If you are focused on saving for elementary and secondary education and are concerned with saving for tuition and related expenses, then Coverdell may be a better option since the 529 plan only covers tuition for elementary and secondary education.

Conclusion

Using a tax deferred plan to save for your child or loved one’s education costs makes the most tax sense, whether one can contribute under $2,000 a year or more, both the Coverdell and 529 plan offer tax efficient ways to build savings to cover educational costs from elementary through college and beyond. For those savers focused on gaining the opportunity to make alternative asset investments, IRA Financial is one of the few companies that offer self-directed options for Coverdell plans.

Although, for individuals seeking to make more meaningful annual contributions to an educational savings plan, the 529 plan becomes the more attractive option, especially if your state of residence offers a state tax deduction for plan contributions.

How to Lower Your Bitcoin IRA Custodial Fees

As a tax attorney and author of the leading book on Bitcoin IRA, How to Use Retirement Funds to Purchase Cryptocurrencies, I am often asked about the benefits of using a Self-Directed IRA or Solo 401(k) plan to buy Bitcoin or other cryptocurrencies.

If you're a Bitcoin investor, you want to invest in Bitcoin and other cryptocurrencies without high commissions. It's likely that you also want control over the private key, which is vital to the purchase and holding of cryptocurrencies securely.

Now there is a great way to invest in Bitcoin, reduce your Bitcoin IRA custodial fees and control your private key - simply reduce the middle man.

- Bitcoin and other cryptos still remain a popular alternative investment choice among retirement savers

- There are several ways you can use retirement funds to invest

- The direct exchange solution is the best way to lower Bitcoin IRA custodial fees

Bitcoin IRA Investors

The price of Bitcoin has fluctuated wildly since the start of COVID, and as of December 2022 sits at around $16,500. But Bitcoin isn’t alone – most cryptocurrency, such as Litecoin and Ethereum, have also fluctuated madly over the last several year. However, as a result of the fallout from the FTX cryptocurrency exchange and the ongoing crypto winter, many Bitcoin and crypto investors are waiting for the right time to jump back into the crypto market.

Many IRA investors understand that an IRA is able to purchase cryptocurrencies, such as Bitcoin without triggering the prohibited transaction rules. The IRS confirms that cryptocurrencies will be treated as property for federal income tax purposes as per IRS Notice 2014-21. As a result, just like stocks and real estate, you can purchase Bitcoin with your retirement funds.

So the question becomes, what are the best ways to lower Bitcoin IRA custodial fees?

There are generally three ways you can purchase Bitcoin with IRA funds:

- The broker/custodian controlled approach

- Wallet Control IRA LLC solution

- Direct Exchange Solution

Each structure has both advantages and disadvantages of using them.

1. Bitcoin IRA Broker/Custodian Controlled

With the Bitcoin IRA Broker/Custodian Controlled approach, you must purchase the cryptocurrency through brokers associated with a Bitcoin IRA facilitator. Typically, a cryptocurrency investor will open a Self-Directed IRA account with a custodian.

You, the IRA investor, will then transfer or rollover your retirement funds tax-free to the new IRA custodian. The custodian will then transfer the funds to a broker who will purchase the cryptocurrencies for the IRA investor. The cryptocurrencies are typically purchased by phone. In this structure, you will be limited to investing in the cryptocurrencies the broker offers.

When the broker purchases the cryptocurrencies, they are stored in a digital wallet, and that typically requires multiple signature verification. However, you do not control the cryptocurrency wallet or the associated private key.

Additionally, if you want to sell or exchange the cryptocurrency, this requires interaction with the broker. You cannot complete this online. Furthermore, you have to pay commissions on each side of the transaction.

Will this structure help lower your Bitcoin IRA custodial fees? Let us take a look at the advantages and disadvantages of using a Bitcoin IRA broker/custodian.

Advantages

- Very Hands-off

- No need to interact with cryptocurrency exchanges

Disadvantages

- High fees – commissions can range from 5%-15% of IRA funds invested.

- You have no control over the cryptocurrency wallet.

- No access to wallet private key.

- You lack the ability to trade cryptocurrencies 24/7, which is how the cryptocurrency market operates.

- All cryptocurrency trades must go through the broker, which is typically done by phone and only during business hours.

- IRA custodian fees are based on the value of the IRA assets invested.

If you wish to lower your Bitcoin IRA custodial fees, as you can see, the high fees associated with a broker or custodian make it an unpractical option.

2. Wallet Control IRA LLC

The Wallet Control IRA LLC allows you to establish an IRA account with a self-directed IRA custodian. You then roll over your retirement funds tax-free to the new custodian. The IRA assets will then be transferred to a newly established limited liability company (LLC) tax-free in exchange for 100% interest in the newly established LLC.

The LLC will be wholly owned by the IRA, and you become the manager. Since the individual retirement account owns 100% of the LLC, it is a disregarded entity for tax purposes. The advantage of this is that all income and gains from the cryptocurrency investment flow back to the IRA without tax.

You, as manager of the LLC, will then open a cryptocurrency exchange account at the exchange of your choice. Next, you will link the account to the IRA that the LLC bank account owns. The IRA LLC funds will then be wired to the cryptocurrency exchange account, which is to be opened in the name of the LLC. You now have the ability to invest in Bitcoin and other cryptocurrency, as well as trade the cryptos anytime. In addition, by using a Wallet Control IRA LLC solution you will be able to open an account at a foreign crypto exchange in the name of the LLC and purchase XRP and other cryptos not available on many U.S. exchanges.

Probably the biggest advantage of buying and holding cryptos in a Wallet Control IRA LLC solution is that you will have the ability to hold the cryptos you purchase inside a digital or hard wallet that you hold off the internet. You control the wallet, because you’re the manager of the LLC. In light of the FTX bankruptcy and some of the lingering macro crypto exchange problems surfacing, more and more crypto IRA investors are looking for a way to hold their crypto private keys for security purposes.

Let’s take a look at whether the Wallet Control IRA LLC structure will help reduce the cost of your IRA custodian fees.

Advantages

- You can invest in all cryptocurrencies.

- Provides the ability to control costs by selecting cryptocurrency exchange of your choice.

- You’re in control of the cryptocurrency wallet and control over private key.

- Ability to buy, sell, or exchange cryptocurrencies at anytime, including XRP, through a PC or mobile application.

- Flat low annual IRA custodian fee – no asset valuation fees.

Disadvantages

- LLC set-up cost

- There’s more involvement on your part – you must open the cryptocurrency exchange and control the crypto wallet

From a financial perspective, this structure is more preferable than using a broker or custodian. However, keep in mind that the LLC set-up cost can be as high as $1,000. If you’re willing to set up an LLC and wish to lower fees associated with Bitcoin investments, we recommend the Wallet Control IRA LLC over a Bitcoin broker or custodian.

3. Direct Exchange Solution

IRA Financial has a partnership with leading crypto exchange Bitstamp that allows our clients to have their IRA or 401(k) funds invested directly into the exchange without the need for a broker or LLC.

Bitstamp was founded in 2011 and aims to bring secure access to crypto to all corners of the world. Bitstamp supports 65+ cryptocurrencies.

Bitstamp operates under a payment institution license in the EU, BitLicense in New York, and we’re subject to regular audits by the Big Four, the four largest accounting firms in the world. Bitstamp is building the financial infrastructure of tomorrow through transparency for all. As others are keeping an eye on us, you don’t have to. 98% of Bitstamp’s assets are stored offline, crime insurance against theft or fraud, and 2 Factor Authorization.

Bitstamp is present in over 100 countries, with offices in UK, Luxembourg, USA, Singapore, and Slovenia. Now catering to over 4 million customers across the globe.

How Does the IRAFI-Bitstamp Crypto Solution work?

Best and cheapest way to buy

Step 1: Open an IRA or Solo 401(k) account at IRA Financial Trust.

Step 2: Move IRA or 401(k) funds to new IRA Financial account tax free.

Step 3: Funds are moved From IRA Financial to Bitstamp

Step 4: Begin buying and selling cryptos 24/7 on your own without the need for any broker or the use of an LLC on the IRA Financial app.

With the Direct Exchange Account solution, you control the purchase and sale of Bitcoin (and other cryptocurrencies) directly. In other words, you do not need a costly broker or LLC. In addition, the cryptos will be held in the name of the IRA custodian. This will be in the benefit of the IRA holder. As a result, it’s much cleaner from a tax reporting perspective.

Advantages

- No requirement to use broker

- No requirement to use LLC

- Ability to buy, sell, or exchange cryptocurrencies at anytime through a PC or mobile application

- Flat low annual IRA custodian fee – no asset valuation fees

Disadvantages

- You can only purchase the most popular cryptocurrencies.

- The cryptos must be held on the Bitstamp exchange.

Which Structure will Save You More?

If you want to use your IRA funds to invest In Bitcoin and other cryptocurrency, you have options. From a cost perspective, the Direct Exchange solution is seemingly the most cost effective solution to lower any Bitcoin IRA fees. However, if you want total freedom, the LLC solution may be the best way to invest.

Get in Touch

Do you still have question about how you can lower your Bitcoin IRA custodial fees that we did not cover in this article? Feel free to contact IRA Financial directly at 800-472-0646. You can also fill out a contact form to speak with a self-directed retirement specialist.

Excess Roth IRA Contributions - Are They Worth the Risk?

In almost all cases, the penalties for violating IRS rules end up overriding any potential value derived from the transaction. The one exception may be the act of making excess Roth IRA contributions.

With a Traditional IRA, contributions are tax deductible and earnings grow tax-deferred until they are distributed. If a distribution is taken before the IRA holder reaches the age of 59 1/2, a 10% early distribution penalty applies in addition to tax on the amount of the distribution. Moreover, a Traditional IRA is subject to required minimum distributions when the IRA holder reaches the age of 73. Whereas, in the case of a Roth IRA, contributions are after-tax and not tax deductible, but so long as the Roth IRA holder is over the age of 59 1/2 and the Roth IRA has been open and funded for at least five years, all Roth IRA distributions are tax-free and are not subject to the required minimum distribution rules.

In general, an excess Roth IRA contribution occurs if one:

- Contributes more than the contribution limit.

- Makes a regular IRA contribution to a traditional IRA at age 73 or older.

- Makes an improper rollover contribution to an IRA.

The taxation on excess contributions differs if the excess contribution is made to a Traditional or Roth IRA.

Over Contributing to a Roth IRA

In the case of a Traditional IRA, excess contributions would be subject to a 6% tax per year as long as the excess amounts remain in the IRA. In addition, if the IRA holder is under the age of 59 1/2, a 10% early distribution penalty would apply to the amount of the excess contribution. Furthermore, the excess contribution would be subject to income tax, although the earnings generated from the excess contributions would remain in the Traditional IRA.

For a Roth IRA, excess contributions would be subject to a 6% tax per year as long as the excess amounts remain in the Roth IRA. However, unlike a Traditional IRA, there would be no 10% early distribution penalty or tax on the excess contribution amount. Moreover, the earnings from the excess Roth IRA contributions would remain in the Roth IRA.

The tax on an excess IRA contribution cannot be more than 6% of the combined value of all IRAs as of the end of the tax year. In other words, the 6% tax is payable each year that the excess contribution has not been withdrawn or applied toward an allocable contribution for a future year.

Learn More: Converting a Traditional IRA to a Roth IRA

How to Avoid the Roth IRA Excess Contributions Tax

Withdraw the excess contributions from the IRA by the due date of the individual income tax return (including extensions); and withdraw any income earned on the excess contribution.

In addition, an individual can apply an excess contribution to a traditional IRA to a later year by the amount that the maximum deductible amount for the later year exceeds the amount contributed to an IRA (including a Roth IRA) for that year. However, an individual cannot reduce an excess contribution by applying it against an earlier year for which less than the maximum amount allowable was contributed.

Read This: What You Need To Know Before Establishing A Roth IRA For Your Kids

The Strategy

A strategy that has been gaining some popularity as of late surrounds the concept of making excess contributions to a Roth IRA in order to generate additional tax-free returns in the Roth IRA. Since the 6% excise tax only applies to the amount of the Roth IRA excess contribution and no 10% penalty or income tax would apply to the amount of the excess contribution, in addition to the earnings on the excess contribution remaining in the Roth IRA and able to grow tax-free, the idea is that the 6% excise tax on the excess Roth IRA contribution will end up being considerably less than if the investment was made with personal funds subject to the individual income tax rates.

Hence, the excess Roth IRA contribution strategy is based on the notion that paying a 6% tax on excess contributions to a Roth IRA, while gaining the tax advantage of having the earnings from the excess contribution remain in the Roth IRA so it can grow tax-free, is a great deal compared to making the same investment with personal funds and having to pay income tax on the earnings and gains.

The IRS has not yet publicly commented on how they will specifically attack the Roth IRA excess contribution strategy, but it is conceivable that the IRS could end up imposing additional penalties. The IRS would receive notification of the IRA excess contributions through its receipt of Form 5498 from the bank or financial institution where the IRA or IRAs were established.

Making inadvertent excess contributions to an IRA occurs frequently and is typically corrected before the filing of the individual’s income tax return. However, purposely violating the IRA excess contribution rules to receive a tax benefit is not advisable and could lead to an IRS audit.

Contact Us

If you feel you have made excess Roth IRA contributions, please contact us @ 800.472.0646 so we can help you correct the mistake!

What is a Solo 401(k) Prohibited Transaction?

The Internal Revenue Code (IRC) & ERISA does not describe what a Solo 401(k) Plan can invest in, only what it cannot invest in. Internal Revenue Code Sections 408 & 4975 prohibits Disqualified Persons from engaging in certain type of transactions. The purpose of these rules is to encourage the use of qualified retirement plans for accumulation of retirement savings and to prohibit those in control of Solo 401(k) qualified retirement plans from taking advantage of the tax benefits for their personal account. In the following, you will learn about the Solo 401(k) Prohibited Transaction Rules.

Who is a “Disqualified Person?"

The IRS has restricted certain transactions between the Solo 401(k) plan and a “disqualified person." The rationale behind these rules was a congressional assumption that certain transactions between certain parties are inherently suspicious and should be disallowed.

The definition of a disqualified person (IRC Section 4975(e)(2)) extends into a variety of related party scenarios, but generally includes the plan participant, any ancestors or lineal descendants of the Plan Participant, and entities in which the Plan Participant holds a controlling equity or management interest. In essence, under Code Section 4975, a disqualified person means:

- A fiduciary (e.g., the Solo 401k Plan Participant, or person having authority over making 401(k) plan investments),

- A person providing services to the plan (e.g., the trustee or custodian),

- An employer, any of whose employees are covered by the plan (this generally is not applicable to Solo 401k Plans but does include the owner of a business that establishes a qualified retirement plan),

- An employee organization any of whose members are covered by the plan,

- A 50 percent owner of C or D above,

- A family member of A, B, C, or D above (family members include the fiduciary’s spouse, parents, grandparents, children, grandchildren, spouses of the fiduciary’s children and grandchildren (but not parents-in-law),

- An entity (corporation, partnership, trust or estate) owned or controlled more than 50 percent by A, B, C, D, or E. Whether an entity is a disqualified person is determined by considering the indirect stockholdings/interest which would be taken into account under Code Sec. 267(c), except that members of a fiduciary's family are the family members under Code Sec. 4975(e)(6) (lineal descendants) for purposes of determining disqualified persons.

- A 10 percent owner, officer, director, or highly compensated employee of C, D, E, or G,

- A 10 percent or more partner or joint venturer of a person described in C, D, E, or G.

Note: brothers, sisters, aunts, uncles, cousins, step-brothers, step-sisters, and friends are NOT treated as disqualified persons.

Solo 401(k) Prohibited Transaction Rules

The types of prohibited transactions can be best understood by dividing them into three categories: Direct Prohibited Transactions, Self-Dealing Prohibited Transactions, and Conflict of Interest Prohibited Transactions.

Direct Prohibited Transactions

Subject to the exemptions under Internal Revenue Code Section 4975(d), a “Direct Prohibited Transaction” generally involves one of the following:

4975(c)(1)(A): The direct or indirect Sale, exchange, or leasing of property between a Plan and a “disqualified person”

Example 1: Joe sells an interest in a piece of property owned by his Plan to his son.

Example 2: Beth leases real estate owned by her Solo 401k Plan to her daughter.

Example 3: Mark uses his Solo 401k Plan funds to purchase an LLC interest owned by his mother.

4975(c)(1)(B): The direct or indirect lending of money or other extension of credit between a Plan and a “disqualified person”

Example 1: Ted lends his wife $70,000 from his Plan.

Example 2: Mary personally guarantees a bank loan to her Solo 401k Plan to purchase real estate.

Example 3: Dan uses his Solo 401k Plan funds to lend an entity owned and controlled by his father $18,000.

4975(c)(1)(C): The direct or indirect furnishing of goods, services, or facilities between a Solo 401k Plan and a “disqualified person”

Example 1: Andrew buys a piece of property with his Solo 401k Plan funds and hires his father to work on the property.

Example 2: Rachel buys a condo with her Solo 401k Plan funds and personally fixes it up.

Example 3: Betty owns an apartment building with her Plan and hires her mother to manage the property.

4975(c)(1)(D): The direct or indirect transfer to a “disqualified person” of income or assets of a Plan

Example 1: Ken is in a financial jam and takes $32,000 from his Plan to pay a personal debt.

Example 2: John uses his Solo 401k Plan to purchase a rental property and hires his friend to manage the property. The friend then enters into a contract with John and transfers those funds back to John.

Example 3: Melissa invests her Solo 401k Plan funds in a real estate fund and then receives a salary for managing the fund.

Self-Dealing Prohibited Transactions

Subject to the exemptions under Internal Revenue Code Section 4975(d), a “Self-Dealing Prohibited Transaction” generally involves one of the following:

4975(c)(1)(E): The direct or indirect act by a “Disqualified Person” who is a fiduciary whereby he/she deals with income or assets of the Plan in his/her own interest or for his/her own account

Example 1: Debra who is a real estate agent uses her Solo 401k Plan funds to buy a piece of property and earns a commission from the sale.

Example 2: Ben wants to buy a piece of property for $120,000 and would like to own the property personally but does not have sufficient funds. As a result, Ben uses $110,000 from in his Solo 401k Plan and $10,000 personally to make the investment.

Example 3: Nancy uses her Solo 401k Plan funds to invest in a real estate fund managed by her son. Heidi’s father receives a bonus for securing Nancy’s investment.

Conflict of Interest Prohibited Transactions

Subject to the exemptions under Internal Revenue Code Section 4975(d), a “Conflict of Interest Prohibited Transaction” generally involves one of the following:

4975(c)(i)(F): Receipt of any consideration by a “Disqualified Person” who is a fiduciary for his/her own account from any party dealing with the Plan in connection with a transaction involving income or assets of the Plan.

Example 1: Jason uses his Solo 401k Plan funds to loan money to a company in which he manages and controls but owns a small ownership interest in.

Example 2: Cathy uses her Plan to lend money to a business that she works for in order to secure a promotion.

Example 3: Eric uses his Solo 401k Plan funds to invest in a fund that he manages and where his management fee is based on the total value of the fund’s assets.

Statutory Exemptions

Congress created certain statutory exemptions from the prohibited transaction rules outlined under IRC Section 4975(c). For these certain transaction, Congress believed there is a legitimate reason to permit them. For these transactions, Congress has issued a blanket statutory exemptions permitting these transactions assuming that certain requirements specified are satisfied.

Below is a list of some of the statutory exemptions that apply to Solo 401(k) plans:

- Any contract with a disqualified person for office space, legal, accounting or other services necessary for the operation of the Plan as long as reasonable compensation is paid. Note – this exemption does not apply to a Plan fiduciary (the Plan trustee) as per Treasury Regulation Section 54.4975-6(a)(5).

- The provision of ancillary services to a Solo 401(k) plan by a bank trustee.

- receipt by a disqualified person of any benefit to which he may be entitled as a participant or beneficiary in the plan, so long as the benefit is computed and paid on a basis which is consistent with the terms of the plan as applied to all other participants and beneficiaries.

S Corporation Stock

Because of the shareholder restrictions imposed on “S” Corporations, an Solo 401(k) cannot own stock in an S Corporation. Note – a Solo 401(k) can own stock in a “C” Corporation.

Plan Asset Rules

The Department of Labor’s (DOL) Plan Asset Rules essentially define when the assets of an entity are considered ‘Plan" assets. Under the rules, 401(k) qualified plans are frequently viewed as pension plans subjecting them to the Plan Asset Rules. Under the Plan Asset Rules, if the aggregate plan ownership of an entity is 25% or more of all the assets of the entity, then the equity interests and assets of the “investment entity” are viewed as assets of the investing plan for purposes of the prohibited transactions rules, unless an exception applies. Also, if a Solo 401(k) or group of related qualified plans owns 100% of an “operating company," the operating company exception will not apply and the company's assets will still be treated as plan assets.

In summary, the Plan Asset Rules can be triggered if:

- 100% of an “operating company” is owned by one or more 401(k) plans and disqualified persons, in which case all the assets of the “operating company” are deemed Plan assets (assets of the 401(k)), or

- If 25% or more of an “investment company” is owned by 401(k) plans and disqualified persons, in which case all the assets of the “investment company” are deemed Plan Assets (assets of the 401(k)). In determining whether the 25% threshold is met, all 401(k) owners are considered, even if they are owned by unrelated individuals.

Exceptions to the DOL Plan Asset Regulations

The Plan Asset look-through rules do not apply if the entity is an operating company or the partnership interests or membership interests are publicly offered or registered under the Investment Company Act of 1940 (e.g., REITs). They also do not apply if the entity is an “operating company,” which refers to a partnership or LLC that is primarily engaged in the real estate development , venture capital or companies making or providing goods and services, such as a gas station, unless the “operating company” is owned 100% by a 401(k) qualified plan or IRA and/or disqualified persons. In other words, if a 401(k) owns less than 100% of an LLC that is engaged in an active trade or business, such as a restaurant or manufacturing plant, the Plan Asset Rules would not apply. However, the plan investment may still be treated as a prohibited transaction under IRC Section 4975. In addition, the Unrelated Business Taxable Income may apply to subject to the 401(k) to tax on the income or gains generated from the operating business.

Note: The fact that a transaction does not trigger the Plan Asset Rules does not mean that the transaction may not be deemed a prohibited transaction. In other words, a transaction that does not fall under the Plan Asset Rules can still be treated as a prohibited transaction pursuant to IRC Section 4975.

The following are a number of examples that demonstrate the scope of the Plan Asset Rules.

Example 1: A general partner of a hedge fund wishes to invest his Solo 401(k) plan in the hedge fund he manages. If the percentage of 401(k) ownership, including what it would be after the General Partner invests his Solo 401(k) in the fund, equals or exceeds 25% of the equity interests, then the fund's assets are considered "plan asset." That means that a transaction between the general partner, as a disqualified person, and the fund, could be deemed a prohibited transaction because the assets of the fund are viewed as assets of his plan, since a disqualified person cannot transact with the assets of his plan. Accordingly, the General Partner cannot receive personal benefits from his 401(k) investment into the fund. Thus, the General Partner would not be permitted to receive any management fees associated with the ownership interest in the fund because he would be receiving a personal benefit from his Solo 401(k). Note – the General Partner’s plan investment in the fund may also be deemed a direct or indirect prohibited transaction under IRC Section 4975.

Example 2: Jane ‘s Solo 401(k) plan owns 100% of ABC, LLC, which operates a retail store. ABC, LLC makes a loan to Jane. The loan is subject to the Plan Asset Rules and will also be considered a prohibited transaction. Note – any income generated by ABC, LLC that is allocated to the plan would also likely be subject to the Unrelated Business Income tax.

Example 3: Steve’s Solo 401(k) owns 15% of ABC, LLC, an investment company. Allan’s IRA owns 20% of ABC, LLC. Steve and Allan are unrelated. Since a 401(k) qualified plan and an IRA (Plans) own greater than 25% of ABC, LLC, an “investment company," assets of ABC, LLC are Plan Assets and deemed owned by each plan. Thus, if ABC, LLC makes a loan to Steve’s father, the loan would be a prohibited transaction.

Example 4: Robert’s Solo 401(k) plan invests in ABC, LLC, which will purchase a gas station, an “operating company." Robert will take an annual salary of $50,000 to run the gas station. The payment of the salary would be a self-dealing indirect prohibited transaction. Note – any income generated by the gas station that is allocated to the plan would also likely be subject to the Unrelated Business Income tax.

Determining Whether a Specific Transaction is a Prohibited Transaction

Through an arrangement between the IRS and the Department of Labor (DOL), it is the DOL’s responsibility to determine whether a specific transaction is a prohibited transaction and to issue prohibited transaction exemptions. When the IRS discovers what appears to be a prohibited transaction in an individual’s IRA, it turns the matter over to the DOL to make the determination. The DOL reviews the situation and responds to the IRS, which in turn responds to the taxpayer. If the IRA grantor wants to apply for a prohibited transaction exemption, he or she must apply to the DOL. The DOL has the authority to issue prohibited transaction exemptions. Some, known as “prohibited transaction class exemptions” (PTCEs), are available for anyone’s reliance, while others, called “individual prohibited transaction exemptions” (PTEs), are issued only to the applicant.

How to Correctly Achieve Retirement Portfolio Diversity

Asset allocation has been a proven investment strategy for half a century. You can choose from several retirement plans, including the popular choice of an employer-sponsored retirement plan. However, very few plans offer the virtues of diversification as a Self-Directed retirement plan, such as the Solo 401(k) for owner-only businesses, and the Self-Directed IRA for everyone else. In this article, we will explain how retirement investors can achieve retirement portfolio diversity the right way.

Why is Investment Diversity Important?

While investors may know the importance of diversification, not all know how to achieve retirement portfolio diversity correctly. But before we get into that, what is diversification and why is it so important?

Let us explain:

Diversification is a risk mitigation strategy. It combines a wide variety of investments within a portfolio (for example, a retirement portfolio) that have different correlation aspects, or in other words, do not move in the same direction. That way, as one investment falls, the other investment may rise.

Brad Blazar, a contributor to Real Assets Adviser and alternative investment expert, explains the premise of investment diversification. "When some investments zig, the others will zag...balancing the portfolio's volatility over time and providing more stable, predictable returns."

Blazar goes on to say that "zig-zag" refers to the non-correlation of assets. For example, if the US equities markets are underperforming, the real estate sector may be on the rise.

"The fact that one sector is doing well while another is lagging tends to mitigate downside risk," explains Blazar, "and more evenly balance long-term returns."

How You Can Benefit with a Self-Directed Retirement Plan

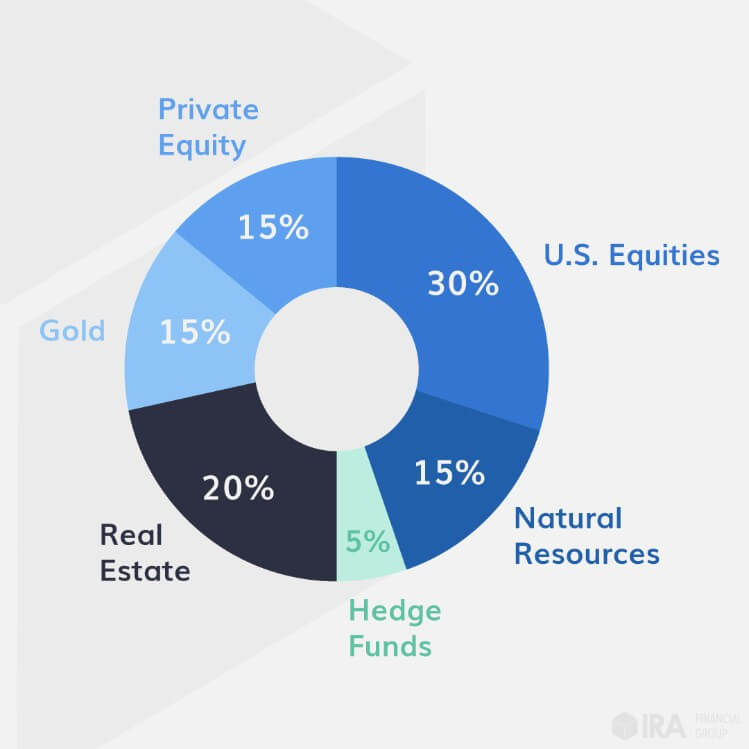

Investors who establish a Self-Directed retirement plan with a passive custodian will be able to invest in popular asset categories, such as stocks and bonds, but also mitigate risk with alternative investments, such as private equity, precious metals, and hard assets, like real estate and gold. Ultimately, you have a greater chance of achieving retirement portfolio diversity.

Whereas, if you establish a Self-Directed retirement plan at a bank or financial institution, your asset allocation will be limited to the financial products they sell. This includes stocks, bonds, mutual funds, and ETFs. If you wish to invest in cryptocurrency, you would not be able to do so with most banks/financial institutions because they do not sell cryptocurrency. Additionally, if you want to invest in real estate, or have rental income, your local bank will not allow you to have these investments in your retirement account.

Asset Allocation - It's a Tricky Practice

The Wrong Way to Diversify Your Investments

A fairly common misconception among investors is, that by owning hundreds of different stocks or owning several mutual funds, they have achieved retirement portfolio diversification.

"What [industry experts] find is a tremendous overlay of similar holdings," says Blazar. "[Investors] might have two or three mutual funds...thinking that having three provides greater diversification."

However, this is not the way to achieve retirement portfolio diversity correctly. And here's why:

By purchasing, for example, two funds in the same sector, both funds will essentially own the same securities, says Blazar. For example, Fund A may hold Apple, and Fund B may hold Microsoft. Fund A and Fund B hold virtually the same securities because they are within the same sector. Now here's how you should diversify your retirement portfolio:

Correctly Achieve Retirement Portfolio Diversity

True diversification comes from the types of investments you purchase. Rather than investing in three mutual funds, purchase only one. Utilize your additional retirement funds to invest in real estate, private equities, natural resources, etc.

Blazar also recommends looking to the "Endowment Model" for systemic risk management. The endowment model illustrates the importance of using retirement funds, such as a Self-Directed IRA to purchase stocks and mutual funds, but also asset classes outside of this sector (real estate, cryptocurrency, venture capital, etc.). This will reduce the risk of correlation, thus your retirement portfolio has a greater chance of performing successfully.

Steps to Achieve Retirement Portfolio Diversity Correctly:

- Invest in multiple sectors - Don't purchase multiple mutual funds, instead, diversify into other investments, such as precious metals, tax liens, or real estate.

- Avoid Banks and Financial Institutions - If you want true control over the types of investments you can make with your retirement funds, such as the ability to make alternative investments, re-consider working with a bank, such as Wells Fargo, or a financial institution, like Fidelity.

- Establish a Self-Directed retirement plan - It is possible to achieve retirement portfolio diversity correctly with a flexible plan that allows for traditional and alternative investments, like the Solo 401(k) or Self-Directed IRA.

Related: Open a Self-Directed IRA Online

*Before opening a Self-Directed IRA, we recommend that you check fees, and what alternative investments the company offers. IRA Financial offers a true Self-Directed IRA, allowing you countless investment options. We also charge a flat fee per year, with no transaction fees or account valuation fees.

Self-Directed IRA and Solo 401(k) Retirement Plans

At IRA Financial, we offer two self-directed retirement plans that give investors the freedom to use their retirement funds to make almost any type of investment:

- Solo 401(k), which is uniquely designed for owner-only businesses and individuals who generate some form of self-employment income.

- Self-Directed IRA, which allows all other investors to utilize retirement funds for both traditional and non-traditional investments in a tax-advantaged manner.