Are Coverdell ESA Contributions Tax Deductible? Everything You Need to Know

Are Coverdell ESA contributions tax deductible? The straightforward answer is no; contributions to a Coverdell Education Savings Account (ESA) are not tax deductible. However, there are other substantial tax benefits associated with Coverdell ESAs. In this article, we’ll explore the tax treatment of these accounts, the benefits they offer, and the regulations you need to know.

Key Takeaways

- Coverdell Education Savings Accounts (ESAs) are designed for saving for a child’s educational expenses, allowing tax-free growth and withdrawals for qualified expenses, but contributions are not tax-deductible.

- Annual contributions to a Coverdell ESA are capped at $2,000 per beneficiary, with eligibility restrictions based on modified adjusted gross income, and funds must typically be withdrawn by the time the beneficiary reaches age 30.

- Coverdell ESAs cover a broad range of qualified educational expenses from preschool through college, providing families with flexibility in how they allocate funds while also allowing beneficiary changes and rollovers without tax consequences.

Understanding Coverdell ESAs

A Coverdell Education Savings Account is designed to help families set aside funds for a child’s educational needs. It provides a tax-advantaged way of saving that can be integral to preparing for the costs associated with schooling. The money saved in these accounts can only be used by the designated beneficiary and must go towards meeting education expenses.

These accounts are flexible, covering an array of qualified education expenses from elementary and secondary school costs through higher education expenditures. Due to this wide range, Coverdell ESAs become a comprehensive tool for parents who want to financially support their children’s learning path right from primary school up until college graduation.

Tax Treatment of Coverdell ESA Contributions

Grasping the tax implications associated with Coverdells is essential. In contrast to certain savings plans, money contributed into Coverdell ESAs doesn’t afford you a deduction on your taxes. While Coverdell ESA contributions won’t lower your taxable income, these funds are not subject to immediate taxation—a characteristic shared by similar educational saving vehicles such as qualified tuition programs where contribution deductions are also unavailable.

The real fiscal incentive of investing in Coverdell ESAs comes from the potential for earnings growth and withdrawals that remain untaxed when used for qualifying educational expenses. This feature can significantly amplify the value of your investment over time and compensate for the absence of an immediate tax break, making Coverdell ESAs an attractive option despite their non-deductible nature upon initial contribution.

Tax-Free Growth and Withdrawals

One of the prominent advantages of Coverdell ESAs is that earnings within these accounts are allowed to grow tax free. Provided that the funds are utilized for qualified education expenses, there will be no federal income tax applied to the growth of your contributions. Initiating contributions at an early stage can yield considerable savings thanks to this benefit.

Distributions from a Coverdell ESA made for qualified education expenses typically retain their status as being tax free. These distributions must not exceed the amount of qualified expenses incurred by the beneficiary in that same year in order to remain exempt from taxes. Utilizing this perk effectively can play a crucial role in managing educational costs which continue to escalate.

It’s imperative that withdrawals are used exclusively for qualified expenses if they’re meant to keep their tax-free advantage. Any withdrawals not meeting these criteria would attract both income taxes and possibly a 10% penalty on any earnings accumulated within your account, underscoring the need for strategic planning when administering funds held within your Coverdell.

Coverdell ESA Contribution Limits and Eligibility

It is important to know about the restrictions on contributions and eligibility criteria for Coverdells to take full advantage of their potential. For each beneficiary, total annual contributions made to a Coverdell ESA cannot exceed $2,000, regardless of how many individuals contribute. This cumulative limit encompasses all contributing parties.

The ability to make Coverdell ESA contributions is predicated upon specific income thresholds based on modified adjusted gross income (MAGI). Contributors are disqualified from adding funds if their MAGI exceeds the annual limit. The individual designated as the beneficiary must be under 18 years old at account inception unless they qualify due to special needs which permits extended participation in the program.

Lastly, adhering to withdrawal deadlines from a Coverdell ESA is crucial. Beneficiaries are expected to deplete these accounts by age 30 lest they incur tax liabilities and penalties. Should any money remain after reaching this age limit without being utilized for education expenses, it will then become taxable income for the recipient. Understanding how withdrawals work within these constraints ensures adherence to fiscal stipulations associated with these accounts.

Qualified Education Expenses

Coverdell ESA funds are applicable to an extensive array of qualified education expenses, offering considerable flexibility. Such expenses encompass not only tuition, fees, and textbooks, but also required materials for participation or attendance at a qualifying educational institution. This list is comprehensive.

These qualified expenses include academic tutoring services as well as those tailored to special needs students, computer technology and Internet connectivity costs. They can also be used for uniforms, travel expenses related to schooling, after-school programs and any other qualifying costs incurred during the academic period—allowing families from elementary through higher education levels access funding which may contribute towards securing an education credit.

In instances where higher learning isn’t pursued by the beneficiary of a Coverdell ESA account holder’s plan still retains value due its application toward a variety of eligible educational expenses thus enabling consistent support throughout various stages along one’s scholastic path regardless whether it culminates with university studies or another formative experience altogether—all whilst maintaining fluidity within this financial provision set up specifically with beneficiaries’ educations in mind.

Making Withdrawals from a Coverdell ESA

If you withdraw money from a Coverdell ESA for expenses related to education such as tuition, fees, books, supplies, and some K-12 expenditures, the process is simple. These withdrawals can be tax-free when they are utilized for both secondary and post-secondary educational costs, giving families flexibility in how to apply these funds.

To maintain the tax-free status of these withdrawals from a Coverdell ESA, it’s important that the funds are expended on qualified education expenses within the same calendar year that those costs arise. Speaking, beneficiaries need to use their Coverdell ESA assets before reaching age 30. If not used by this time frame, any leftover amounts will become taxable income unless transferred via rollover into another younger relative’s Coverdell account.

Book a free call with a self-directed retirement specialist

- Review your self-directed retirement options

- Learn about investing in alternative assets

- Get all of your questions answered

Non-Qualified Withdrawals and Penalties

Coverdells provide significant tax advantages when funds are used for eligible withdrawals. Distributions for non-qualified expenses result in penalties. The earnings portion of these non-qualified distributions is counted as part of gross income and is subject to the corresponding income taxes. A 10% federal penalty is levied on the earnings.

There are certain situations where this penalty can be waived, such as in the event that the beneficiary passes away or suffers a disability. These exceptions highlight why it’s critical to strategize properly so that Coverdell ESA resources are expended according to their designated educational purpose.

Beneficiary Changes and Rollover Options

Coverdell ESAs offer the adaptable option of reassigning beneficiaries. Should the original designated beneficiary have no need for the funds, they can be transferred, tax free, to another eligible family member or even a special needs beneficiary. This transferability ensures that educational funds within a family are utilized to their fullest potential.

In instances where the beneficiary has special needs, Coverdell ESA regulations permit them to maintain account funds beyond the age of 30 without incurring any penalties. These accounts allow for rollovers into another Coverdell ESA either for that same individual or another qualifying family member under age 30. It is important to complete these rollovers within a strict 60-day window and note that each recipient can only participate in one such transaction per year without triggering taxable events.

The process of transferring assets between Coverdell ESAs does not usually result in taxation nor require direct handling of cash by recipients. The inherent flexibility afforded by this structure guarantees uninterrupted tax-free growth and future availability for education-related expenses as required by students’ evolving needs.

Additional Benefits of Coverdell ESAs

ESAs provide a variety of advantages beyond simply financing educational pursuits. Their flexibility stands out as a major benefit, with the ability to apply funds towards academic costs from kindergarten up through higher education levels. This extensive scope renders Coverdell ESAs an essential tool for enduring educational financial planning.

Should the individual named as the designated beneficiary opt out of college attendance, any residual monies within their Coverdell ESA remain useful for covering alternative eligible educational expenses. Such a provision secures that no resources are squandered and can still be directed towards fostering the beneficiary’s learning requirements.

Comparing Coverdell ESAs with Other Education Savings Plans

Coverdell ESAs offer several unique advantages over other education savings plans like 529 plans. One primary benefit is the wider range of investment options with Coverdell ESAs, allowing for more personalized and potentially higher-yielding investment strategies.

Unlike 529 plans, Coverdell ESAs have no cap on tax-free withdrawals for qualified elementary or secondary education expenses. This makes them attractive for families looking to cover K-12 expenses without worrying about withdrawal limits. However, Coverdell ESAs must distribute any remaining funds when the beneficiary turns 30, while 529 plans allow funds to remain indefinitely if used for qualified educational expenses.

Coverdell ESAs generally receive favorable treatment in financial aid calculations, similar to 529 plans. However, financial aid eligibility may vary based on how ESA accounts are reported, particularly if listed under non-relatives. Assets in a parent’s name usually count less against financial aid than those in a grandparent’s name.

Another key difference is that 529 plans support a broader range of educational expenses, including K-12 tuition, which Coverdell ESAs do not cover. This distinction can influence a family’s decision when choosing between the two savings plans.

How to Open a Coverdell ESA

Starting a Coverdell at IRA Financial is a relatively simple procedure that any family member can undertake. You will need to furnish essential documentation, such as proof of the beneficiary’s date of birth, full legal name, and Social Security number during the process. Contact us to learn more about setting up an account. It is crucial that you designate the account specifically as a Coverdell ESA to adhere to IRS regulations. They offer comprehensive information regarding permissible contributions and distributions associated with these accounts. The official written agreement controlling the account must align with certain standards laid out by the IRS in order to maintain compliance.

Following closely to these guidelines allows one not only to create but also effectively contribute towards building savings within a Coverdell ESA intended for financing educational expenses for your designated recipient’s future learning endeavors.

Effect on Financial Aid

ESAs are treated favorably when it comes to financial aid calculations, akin to other education savings vehicles such as 529 plans. Consequently, the assets in a Coverdell ESA usually have little influence on a beneficiary’s ability to qualify for financial aid. Nevertheless, one must be aware that eligibility for financial aid may necessitate the disclosure of any ESA accounts owned by individuals who are not family members, potentially affecting the total assessment of financial support.

For both elementary and secondary schooling levels, qualified education expenses encompass items like tuition fees, academic tutoring services, accommodations necessary for special needs students and even room and board costs incurred by those enrolled at least half-time pursuing qualified higher education expenses. Such extensive applicability permits funds from Coverdell ESAs to meet an array of educational expenditures without substantially jeopardizing eligibility for student financial assistance programs.

Summary

Coverdell Education Savings Accounts offer a flexible and advantageous method for saving funds to finance a child’s education-related expenses. They allow for the growth of savings without incurring taxes, as well as tax-free withdrawals when these are utilized to cover eligible educational expenditures. This makes them an essential asset for families who are strategizing on how best to support their children’s scholastic future while remaining aware of contribution caps, qualifying criteria, and potential consequences associated with non-qualified disbursements.

Coverdell ESAs serve as an invaluable instrument for setting aside money dedicated to educational purposes. They facilitate substantial fiscal flexibility alongside perks that are linked with tax relief which can substantially alleviate the financial burden imposed by escalating educational fees. Whether commencing your savings plan or contemplating fund transfers within family members’ accounts, gaining comprehensive knowledge about the functions and regulations governing Coverdell ESAs is pivotal in ensuring sound decision-making that lays down a robust economic groundwork conducive to one’s child succeeding academically.

Support Your Family’s Education and Make Smart Savings Choices

A Coverdell ESA won’t get you a tax deduction today—but its real power lies in tax-free growth and withdrawals for eligible education expenses. If you’re planning ahead for your child’s schooling, you deserve a retirement-and-education strategy that works as hard as you do.

Schedule a Free Consultation

Open an Account

Frequently Asked Questions

Are contributions to a Coverdell ESA tax-deductible?

What is the annual contribution limit for a Coverdell ESA?

What happens if the funds in a Coverdell ESA are not used by the beneficiary's 30th birthday?

Can Coverdell ESA funds be used for expenses other than college tuition?

How does a Coverdell ESA impact financial aid eligibility?

Can I Buy I Bonds with a Self-Directed IRA or Solo 401(k)?

I Bonds have quickly become a powerful way for millions of Americans to generate strong guaranteed returns in a volatile investment marketplace. Electronic I Bonds can generally be purchased by individuals and entities, but the looming question persists, can I Bonds be purchased by a Self-Directed IRA or Solo 401(k) plan. In this article, I will address this question in detail.

- I Bonds offer a strong, guaranteed return

- Trusts, like an IRA or 401(k), can purchase I Bonds, but only electronic ones

- It is possible to use retirement funds to invest in I Bonds

What is an I Bond?

According to Treasury Direct, a Series I savings bond is a type of security that earns interest based on both a fixed rate and a rate that is set twice a year based on inflation. The bond earns interest until it reaches 30 years or you cash it, whichever comes first.

Who Can Own I Bonds?

In general, individuals and entities can only buy I Bonds. In the case of an individual, the individual must have a Social Security Number and must satisfy the following conditions:

- United States citizen, whether living in the US or abroad

- United States resident

- Civilian employee of the US, no matter where you live

For children under the age of 18, a parent or other adult custodian may open for the child a Treasury Direct account that is linked to the adult's Treasury Direct account.

In the case of entities, such as LLCs and corporations, and trusts, only electronic I Bonds, and not paper I Bonds, can be purchased.

Related: Can I Buy T-Bills in an IRA?

IRAs and I Bonds

Because an IRA is not an individual and does not have a social security number, in general, an IRA, Roth IRA, SEP IRA, or SIMPLE IRA cannot directly own an I Bond. Unfortunately, the Treasury Direct application process requires the applicant to have a social security number. Likewise, an IRA is not an entity. However, an IRA can be considered a trust under Internal Revenue Code Section 501.

Hence, so long as the IRA has a tax identification number, it could be possible for the IRA to apply for an I Bond using Treasury Direct. The application process does not request information on the IRA custodian, but simply requests information on the account manager, which can be the individual IRA owner.

Learn more: Buying T-Bills in a Retirement Account

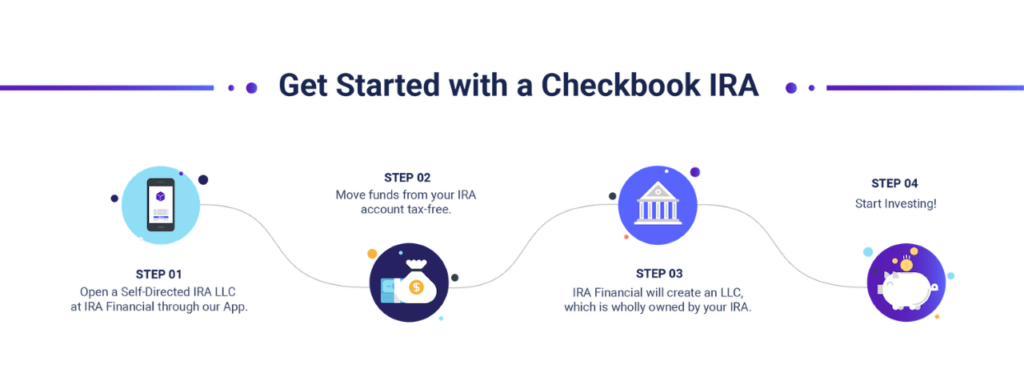

Self-Directed IRA LLC & I Bonds

Just like an IRA can technically be treated as a trust and use Treasury Direct to purchase I Bonds, a retirement investor can establish a Self-Directed IRA LLC to purchase I Bonds.

Under the Self-Directed IRA LLC, also known as the Checkbook IRA, a limited liability company (“LLC”) is created which is funded and owned by the IRA and managed by the IRA holder.

Therefore, using Treasury Direct, the IRA owner can apply using the LLC name and LLC tax identification number. Treasury Direct does not request information on the owner of the LLC (the IRA) but simply requests info on the account manager, who can be the individual IRA owner.

There is no guarantee that Treasury Direct will accept the submitted application in the name of the IRA or the Self-Directed IRA LLC. However, many IRA Financial clients have successfully purchased I Bonds with a Self-Directed IRA using Treasury Direct. IRA Financial clients using a Checkbook IRA to purchase I Bonds have had greater success with the account application process on Treasury Direct.

Solo 401(k) & I Bonds

Like an IRA, a 401(k) plan is defined as a trust. Hence, technically a 401(k) should be able to purchase I Bonds via the Treasury Direct platform. However, establishing a Treasury Direct account for a 401(k) plan with multiple employees could prove cumbersome because the account would have to be established for all interested participants and the plan trustee would need to be involved in the account opening process.

Whereas, in the case of a Solo 401(k), also known as an Individual 401(k) plan, there is only one interested participant - you.

Using the Treasury Direct portal, a Solo 401(k) plan can establish an account in the name of the 401(k) trust, and the plan participant can serve as the account manager. For purposes of Treasury Direct, it would be helpful if the plan name included the word “trust” in the title. For example, the ABC 401(k) Trust, or the ABC Inc. Trust. A business has quite a bit of flexibility in naming a 401(k) plan.

For example, if John Smith wanted to purchase, I Bonds for the John Smith 401(k) Trust, he would submit the application using Treasury Direct as John Smith, Trustee of the John Smith 401(k) Trust. John Smith would then include his personal info under “Account Manager.”

Like in the case of an IRA, there is no guarantee that Treasury Direct will accept the submitted application as a “trust” in the name of the Solo 401(k). However, many IRA Financial clients have successfully purchased I Bonds with a self-directed solo 401(k) using Treasury Direct.

How Much Does an I Bond Cost?

In a calendar year, one can acquire:

- up to $10,000 in electronic I Bonds in Treasury Direct

- up to $5,000 in paper, I Bonds using your federal income tax refund

Items to Consider:

- The limits apply separately, meaning one could acquire up to $15,000 in I Bonds in a calendar year

- Bonds you buy for yourself and bonds you receive as gifts or via transfers count toward the limit. Two exceptions:

- If a bond is transferred to you due to the death of the original owner, the amount doesn't count toward your limit

- If you own a paper bond issued before 2008, you can convert it to an electronic bond in your account in Treasury Direct regardless of the amount of the bond.

How can I Buy IBonds?

The most popular way to buy I Bonds, and the only way they can be purchased using an LLC or trust, is in electronic form using the TreasuryDirect online portal. Interest on I Bonds are subject to federal income tax.

Why Are I Bonds So Popular?

With financial markets in flux in 2022, gaining the ability to earn almost 10% on an investment seems almost too good to be true. Add the fact that the bonds are secured by the US Government, you can understand why so many Americans are looking to find ways to get more of their savings into I Bonds.

The downside to the I Bond investment strategy is that one is capped at $15,000 a year. Although, the limit would be $10,000 for entities and trusts.

Conclusion

It is unclear whether the Treasury intended for IRA and 401(k) plans to be eligible to purchase I Bonds using Treasury Direct. There does not seem to be any clear prohibition, although there is no direct endorsement of the use of retirement accounts to purchase IBonds. That being said, many IRA Financial clients either using a Self-Directed IRA LLC or Solo 401(k) plan find it worth their time to apply to purchase I Bonds using Treasury Direct.

Invest in I Bonds Through Your Self‑Directed Retirement Account

While I Bonds aren’t directly purchased through a traditional IRA or 401(k), a self‑directed structure can open the door. With the right setup, you can potentially add this low‑risk, inflation‑protected investment to your retirement portfolio. Our IRA Financial specialists can guide you through the process and ensure compliance every step of the way.

Schedule a Free Consultation

Open an Account

Alternative Investments to Consider for Your Portfolio

Looking for good alternative investments? This article covers options like real estate, private equity, and cryptocurrencies. These can offer higher returns and diversify your portfolio. Read on to find what suits your investment goals.

Key Takeaways

- Alternative investments encompass a variety of assets beyond traditional stocks and bonds, offering unique opportunities but also increased risks and illiquidity.

- Diverse options such as real estate, private equity, hedge funds, and cryptocurrencies can enhance portfolio diversification, though they require careful consideration and due diligence.

- Investors should align alternative investment strategies with their financial goals and risk tolerance, gradually increasing exposure to manage risks effectively.

Understanding Alternative Investments

Alternative investments are assets outside traditional categories like stocks, bonds, and cash. They encompass a diverse range of options, including real estate, private equity, commodities, and various asset classes. Unlike traditional investments, which are often publicly traded and highly liquid, alternative investments are typically more complex and less regulated. This can lead to higher potential returns, but also increased risk and illiquidity in different types of alternative assets, including alternative funds.

One of the key attractions of alternative investments is their ability to offer unique opportunities that are not available in public markets. For instance, private equity and venture capital can provide access to early-stage companies with significant growth potential. Hedge funds, another popular form of alternative investment, use sophisticated strategies to generate returns regardless of market conditions.

These investments are generally more accessible to high-net-worth individuals and institutional investors who seek to reduce portfolio volatility and achieve higher returns while aligning with their investment objectives. However, the landscape is evolving, and individual investors are increasingly exploring traditional stocks and bond investments to diversify their portfolios and enhance their long-term financial prospects.

Real Estate Investments

Real estate is a prominent form of alternative investments. It is known for being both tangible and widely favored. The allure of owning property lies in its potential for steady income generation and long-term appreciation. Investors can dive into real estate through various avenues such as direct property ownership, Real Estate Investment Trusts (REITs), real assets, or real estate funds.

Direct ownership involves purchasing residential or commercial properties and earning rental income. This approach provides hands-on control but requires significant capital and management effort. On the other hand, REITs and real estate funds offer a more hands-off investment strategy, allowing investors to benefit from the real estate market without the hassles of property management.

However, real estate investments are not without risks. Market fluctuations, changes in interest rates, and the potential for over-concentrating capital in a single property can pose significant challenges. Despite these risks, the potential for complex tax structures and diverse income generation makes real estate an appealing choice for many investors.

Private Equity and Venture Capital

Private equity entails making investments in private companies that are privately held. These companies are not listed on public exchanges. This can include buyouts, growth equity, and private debt investments, as well as private equity investments. Venture capital, a subset of private equity, focuses on early-stage companies with high growth potential. These investments are highly speculative but can yield substantial returns if the companies succeed.

Venture capitalists often play an active role in mentoring and advising portfolio companies, enhancing their chances of success. These investments are typically long-term and require a high tolerance for risk and patience. Sectors like technology and biotech are popular among venture capitalists due to their innovative potential and market impact.

While the potential rewards are enticing, it’s crucial to understand the risks and illiquidity associated with private equity and venture capital investments. These investments are not easily sold, and investors must be prepared for the possibility of losing their entire investment. However, the prospect of tapping into groundbreaking companies and disruptive technologies makes them a compelling option for those with the right risk appetite.

Book a free call with a self-directed retirement specialist

- Review your self-directed retirement options

- Learn about investing in alternative assets

- Get all of your questions answered

Hedge Funds

Hedge funds are investment funds that pool resources from multiple investors. They use a variety of strategies to generate active returns. These strategies can range from long/short equity to market neutrality and global macro, each designed to capitalize on different market conditions. The flexibility and sophistication of hedge funds allow them to navigate market volatility and aim for positive returns in both rising and falling markets.

Hedge funds often come with higher fees and are less regulated than mutual funds, leading to concerns about transparency. This makes thorough due diligence essential before investing. Evaluating a hedge fund’s strategy, performance history, and risk management practices can help investors make informed decisions.

Moreover, hedge funds typically require a high minimum investment, sometimes ranging from $100,000 to several million dollars. While this may limit accessibility for some individual investors, those who can meet the requirements may find hedge funds a valuable addition to their investment portfolio, offering diversification and the potential for significant returns.

Commodities and Precious Metals

Commodities and precious metals are notable alternative investments that can help hedge against rising inflation and protect portfolios during market volatility. Commodities include raw materials like oil, gas, and agricultural products, while precious metals encompass gold, silver, and platinum. These assets often move independently of traditional markets, providing critical diversification for investors.

Investing in commodities can be particularly lucrative during periods of geopolitical tension or supply constraints, offering substantial returns. Precious metals, especially gold, are sought after during economic uncertainty, serving as a secure store of value. Investors can purchase these assets directly through bullion, coins, or jewelry, or indirectly through commodity-focused funds.

However, investing in these tangible assets poses challenges such as storage and liquidity. Despite these hurdles, the potential benefits of incorporating commodities and precious metals into an investment portfolio make them a compelling choice for those looking to diversify and hedge against economic downturns.

Cryptocurrencies

Cryptocurrencies represent a new frontier in alternative investments, characterized by digital currencies secured by cryptography. Supported by blockchain technology, cryptocurrencies offer a decentralized and transparent way of transferring value. Popular examples include Bitcoin and Ethereum, which have garnered significant attention and investment.

The volatile nature of cryptocurrency prices can lead to substantial gains or losses, making them a highly speculative investment. Regulatory concerns and the lack of a regulatory framework add to the complexity and risk of investing in cryptocurrencies. Nonetheless, the potential for high returns attracts investors willing to navigate these uncertainties.

Investors can engage in cryptocurrency trading through online brokerages or crypto wallets. For those with a high tolerance for risk and a deep understanding of the technology involved, cryptocurrencies can offer exciting investment opportunities. With platforms like IRA Financial, investors can even enjoy tax-advantaged investment opportunities in cryptocurrencies.

Collectibles and Tangible Assets

Collectibles and tangible assets include art, antiques, wine, and rare coins. These items provide a distinctive option for alternative investment. These items possess intrinsic value and can appreciate over time, providing a hedge against market volatility and inflation. The market for collectibles as an asset class can be influenced by trends and cultural shifts, adding an element of unpredictability.

Investing in collectibles typically involves purchasing these items through auctions or private sales. While the secondary market can be less liquid and more challenging to navigate, the potential for significant appreciation and the enjoyment of owning valuable items make collectibles an attractive option for discerning investors.

Crowdfunding and Peer-to-Peer Lending

Crowdfunding and peer-to-peer lending have revolutionized the way individuals and businesses raise capital. Crowdfunding platforms allow projects to attract funding from a large audience, offering rewards or equity in return. Peer-to-peer lending connects borrowers directly with lenders, often resulting in better interest rates for both parties.

The U.S. peer-to-peer lending market has grown significantly, driven by technological advancements that enhance credit evaluation processes. This growth presents opportunities for investors to diversify their portfolios and earn attractive returns. However, it’s essential to recognize the default risks associated with peer-to-peer loans, where borrowers may fail to repay their loans.

Platforms like IRA Financial make it easier for individual investors to participate in crowdfunding ventures, including hard money loans. While these investments carry risks, the potential for high returns and the democratization of investment opportunities make them an appealing choice for many investors.

Promissory Notes

Promissory notes allow investors to purchase the right to receive payments from a borrower, rather than acquiring the underlying property directly. This investment can offer higher yields, especially if the note is purchased at a discount below its stated value. Platforms like IRA Financial provide access to promissory notes, making them a viable option for investors seeking fixed-income returns.

However, the risk of borrower default is a significant concern, potentially resulting in loss of income or principal. It’s crucial to have a clear exit strategy, whether through selling the note or foreclosing on the property, to manage this type of investment effectively.

Foreign Currencies (Forex)

Forex trading involves the speculative investment of buying and selling different currencies. This market operates 24/7 and is the largest financial market globally. To start trading Forex, investors need to engage a registered broker dealer and may benefit from using demo accounts to practice without real financial risk.

Investing in Forex can be highly volatile and requires a deep understanding of global economic factors that influence currency values. Platforms like IRA Financial offer access to Forex investments, providing opportunities for diversification and potential returns.

Unique Investment Opportunities

Unique investment opportunities such as pre-IPO investments, farm animals, and vineyards offer unconventional ways to diversify a portfolio. These investments can lead to significant returns, especially if the companies or assets perform well. Platforms like IRA Financial enable investors to explore these unique options, adding a layer of diversification and potential growth.

Investing in non-traditional assets requires careful consideration of the market dynamics and potential risks involved. However, the prospect of tapping into unique and innovative investment avenues can be highly rewarding for those willing to take on the challenge.

Risk Factors and Due Diligence

Alternative investments often operate under less regulatory oversight, making due diligence crucial for investors. Understanding the higher risks and potential losses involved is essential for making informed investment decisions. Evaluating factors such as investment strategy, track record, fees, exit strategy, and speculative investment practices can mitigate some of the risks associated with these investments.

Conducting thorough due diligence involves a comprehensive assessment of the significant risks related and benefits of each high risk investment opportunity. Investors should be vigilant and informed, ensuring they align their investments with their financial goals and risk tolerance.

With proper research and careful planning, many alternative investments and alternative strategies can be a valuable addition to a diversified portfolio.

Making Alternative Investments Work for You

It’s important to align your investment strategy with your financial goals. Additionally, you should consider your risk tolerance when exploring alternative investments. Diversifying beyond traditional assets can lead to more consistent returns and better alignment with long-term financial goals. Starting with a smaller allocation to alternative investments and gradually increasing it over time can help manage risk effectively.

Regular consultations with a financial advisor are vital for reassessing investment strategies and adapting to changing financial goals. Creating a tailored financial plan for an alternative investment portfolio involves selecting from multiple funds and strategies based on individual investor preferences, including investment advice.

With the right approach, incorporating alternative investments can enhance portfolio diversification and generate income.

Summary

Alternative investments offer a myriad of opportunities for diversifying portfolios and achieving higher returns. From real estate and private equity to cryptocurrencies and unique investment options, these assets can provide significant benefits if approached with careful planning and due diligence.

As you explore the world of alternative investments, remember to align your investment strategy with your financial goals and risk tolerance. Regularly consult with financial advisors, and be prepared to adapt to changing market conditions. By doing so, you can unlock the full potential of alternative investments and create a robust, diversified portfolio.

Ready to Expand Beyond Stocks and Bonds?

Alternative investments — from real estate and private equity to cryptocurrencies and commodities — can enhance diversification, access unique growth opportunities, and position your retirement portfolio to win when traditional markets struggle. But they also carry unique risks and require deeper due diligence. Let our specialists help you evaluate which alternative asset types fit your goals, structure your self-directed retirement account correctly, and stay IRS-compliant.

Schedule a Free Consultation

Open an Account

Frequently Asked Questions

What are alternative investments?

What are the benefits of investing in real estate?

What are the risks associated with private equity and venture capital?

How do hedge funds differ from mutual funds?

What are the risks of investing in cryptocurrencies?

The Complete Guide to the Self-Directed Coverdell ESA

Investing in education is one of the most important financial decisions a family can make. The rising cost of tuition, books, and other educational expenses has driven many parents and guardians to explore different options for saving money. One of the most flexible and powerful ways to save for education is through a Self-Directed Coverdell ESA (Education Savings Account). Think Self-Directed IRAs and add in the ability to cover education-related expenses.

This guide will break down everything you need to know about the Self-Directed Coverdell ESA, including its benefits, rules, and strategies for maximizing savings.

What Is a Coverdell ESA?

A Coverdell Education Savings Account is a tax-advantaged investment account designed to help families save for a child's education expenses. The Coverdell ESA allows for contributions of up to $2,000 per year per beneficiary. These funds can be used for a wide range of educational expenses, including tuition, books, supplies, and even room and board at eligible schools.

The primary feature of the Coverdell is that contributions are made with after-tax dollars, but the earnings grow tax free. When the funds are withdrawn for qualified educational expenses, they are also tax free, making it an effective way to save for future education costs.

Key Features of a Coverdell ESA:

- Annual contribution limit: $2,000 per beneficiary

- Contributions grow without tax

- Tax-free withdrawals for qualified educational expenses

- Can be used for both K-12 and post-secondary education expenses

What are "Qualified Education Expenses?

Qualified education expenses include costs that are necessary for a student’s enrollment or attendance at an eligible educational institution. These expenses must be used for educational purposes, and they can apply to both K-12 schooling and post-secondary (college or university) education. Here’s a breakdown of what’s considered qualified:

K-12 Expenses

- Tuition and fees: For public, private, or religious schools (K-12)

- Books, supplies, and equipment: That are required for education

- Academic tutoring: If required or necessary for the student’s education

- Special needs services: For students with special needs

- Computer technology or internet access: If used by the student for educational purposes (including for elementary or secondary school)

- Room and board: If the child is enrolled at least half-time in an eligible school

Postsecondary (College or University) Expenses

- Tuition and fees: Required for enrollment at an eligible post-secondary institution

- Books, supplies, and equipment: Needed for a student’s coursework

- Room and board: If the student is enrolled at least half-time (subject to limits)

- Computer technology: Including internet access or related equipment for education

- Special needs services: For a student with special needs that are related to attendance or enrollment at an institution

How does a Self-Directed Coverdell ESA Work?

A Self-Directed Coverdell ESA operates similarly to a traditional Coverdell, but with one crucial difference: the investor has complete control over the types of investments made within the account. While traditional Coverdells often limit you to stocks, bonds, and mutual funds, the self-directed version offers a wider array of investment options, such as real estate, private equity, metals, cryptos, small businesses, and commodities.

The expanded range of investments can lead to higher potential returns, although it comes with additional risks. Be sure to work with a professional financial advisor to make sure your investments align with your goals and risk tolerance.

Key Differences in a Self-Directed Coverdell ESA:

- Full control over investment choices

- Access to alternative investments (real estate, precious metals, etc.)

- Higher risk, but the potential for greater rewards

Eligibility and Contribution Rules

Before opening a Self-Directed Coverdell ESA, it’s important to understand the rules regarding eligibility and contributions.

Eligibility:

- The beneficiary (typically the child or student) must be under 18 when contributions are made.

- Contributions can be made by parents, guardians, grandparents, or other family members, provided they meet income requirements.

Income Limits for Contributors:

- Single filers with a modified adjusted gross income (MAGI) below $110,000

- Joint filers with a MAGI below $220,000

Contribution Limits:

- The total annual contribution for each beneficiary cannot exceed $2,000.

- Contributions must be made by the tax filing deadline, typically April 15 of the following year.

Contributions are not tax-deductible, but the earnings grow tax free, and qualified withdrawals are also tax free.

Investment Options in a Self-Directed ESA

One of the most attractive features of a Self-Directed Coverdell ESA is the flexibility it offers in choosing investments. Unlike standard accounts, where investment options may be limited to mutual funds or stocks, a self-directed account opens the door to a variety of alternative investments.

Investment Options:

- Real Estate: You can invest in residential or commercial property through a self-directed ESA, which could appreciate in value over time and provide rental income.

- Precious Metals: Gold, silver, and other metals are considered safe-haven assets that can hedge against inflation.

- Cryptocurrency: For those with a higher risk tolerance, investing in Bitcoin, Ethereum, or other digital currencies is an option.

- Private Equity: Invest in private companies, startups, or venture capital, potentially yielding high returns.

- Stocks and Bonds: You can still invest in traditional assets like individual stocks and bonds, allowing for diversification within the account.

This wide range of investment choices allows for potentially higher returns but also increases the complexity of managing the account.

Advantages of a Self-Directed Coverdell ESA

Choosing a Self-Directed Coverdell ESA provides unique benefits for savvy investors. Here are some of the key advantages:

Investment Flexibility

You are not restricted to the limited options of mutual funds or standard portfolios. The ability to invest in real estate, private equity, or even cryptocurrencies opens doors to more lucrative opportunities.

Tax-Free Growth

Like traditional Coverdell ESAs, all investment earnings grow tax free, and withdrawals for qualified expenses are also tax free, making it a very tax-efficient investment tool.

Broader Educational Expense Coverage

Unlike 529 plans, which are mostly for college expenses, Coverdell ESAs can be used for K-12 educational expenses as well. This includes tuition, books, and even technology required for schoolwork.

Control and Customization

A self-directed account allows you to tailor your investments according to your risk tolerance and financial goals. Whether you’re conservative or aggressive, you can find investments that fit your strategy.

Limitations and Risks

While the Self-Directed Coverdell ESA offers incredible flexibility, it’s not without its limitations and risks.

- Low Contribution Limits: At just $2,000 per year per beneficiary, the contribution cap can be restrictive. Compared to a 529 Plan, which often allows much higher contributions, this can limit the growth of your savings.

- Complexity of Self-Directed Investing: Managing a Self-Directed ESA is more complex than a traditional ESA or 529 Plan. You may need to do more research, and there’s often an administrative cost involved. Make sure you are working with a competent custodian that specializes in self-directed solutions.

- Investment Risk: With higher rewards come higher risks, especially with alternative investments like cryptocurrencies or real estate. There’s no guarantee of a positive return, and significant losses could occur.

- Age Limitation: The beneficiary must use the funds by age 30, or they will face penalties. This rule can make it challenging if the funds aren’t fully used for educational expenses.

Tax Benefits and Considerations

One of the primary reasons to consider a Self-Directed Coverdell ESA is the tax advantages. All earnings in a Coverdell ESA grow tax free, similar to a Roth IRA. You won’t owe any taxes on dividends, interest, or capital gains within the account. If the funds are used for qualified educational expenses (such as tuition, fees, books, and room and board), the withdrawals are also tax free. However, if you use the funds for non-educational purposes, you’ll face taxes and a 10% penalty on the earnings portion of the withdrawal, making it critical to plan carefully.

Strategies to Maximize Your Coverdell ESA

To make the most of your Self-Directed Coverdell ESA, consider the following strategies:

- Start Early: The earlier you start contributing, the longer your investments have to grow. Compounding interest can significantly boost your account’s value over time.

- Diversify Investments: Diversification reduces risk. Instead of placing all your funds in one asset, spread them across a mix of traditional and alternative investments to balance risk and reward.

- Maximize Contributions: While $2,000 might not seem like much, contributing the maximum every year can still add up. Try to make regular contributions to maximize your investment’s potential.

- Use for K-12 Expenses: Unlike a 529 plan, Coverdell ESAs can be used for K-12 educational expenses. If your child attends private school, using the funds early can offer immediate tax advantages.

What Happens After the Beneficiary Reaches the Age of 30?

Amounts in the Coverdell ESA must be distributed when the designated beneficiary reaches age 30, unless the beneficiary is a special needs beneficiary. Additionally, certain transfers to members of the beneficiary's family are permitted, including:

- Son, daughter, stepchild, foster child, adopted child, or a descendant of any of them.

- Brother, sister, stepbrother, or stepsister.

- Father or mother or ancestor of either.

- Stepfather or stepmother.

- Son or daughter of a brother or sister.

- Brother or sister of father or mother.

- Son-in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law, or sister-in-law. The spouse of any individual listed above.

- First cousin.

Conclusion: Is a Self-Directed Coverdell ESA Right for You?

The Self-Directed Coverdell ESA is a powerful tool for parents or guardians who want more control over how they save for their child's education. With its wide range of investment options, tax benefits, and flexibility for covering K-12 and post-secondary education expenses, it offers advantages that are unmatched by other education savings accounts.

However, it’s not for everyone. The lower contribution limits, the complexity of managing a self-directed account, and the risks involved with alternative investments can be drawbacks. If you are financially savvy and comfortable with risk, this account can be a fantastic way to maximize your education savings. Otherwise, a traditional ESA or 529 plan might be a better fit.

Ultimately, the choice depends on your financial goals, risk tolerance, and the educational needs of your beneficiary.

Expand Beyond Traditional Education Savings — Discover Self-Directed Options

Whether you're saving for college, private school, or future educational goals, a Self-Directed Coverdell ESA lets you invest beyond the limits of traditional savings plans. From real estate and precious metals to private equity and crypto, IRA Financial can help you create a tax-advantaged, diversified strategy for your child’s education.

Schedule a Free Consultation

Open an Account

Private Placement Investments and the Self-Directed IRA Rules

In general, a traditional financial institution will not allow investors to use their IRA to invest in private placement investments. The reason for this is that a financial institution or brokerage firm does not make money when clients invest in alternative assets, such as private placements.

Whereas, a self-directed IRA is a type that allows IRA investors to make alternative investments, such as private placements. A self-directed IRA is not a legal term that you will find in the Internal Revenue Code. Today, the Retirement Industry Trust Association (RITA) estimates anywhere between 4-7% of all IRAs are invested in alternative assets. Accordingly, the self-directed IRA is the only way one can purchase alternative assets in an IRA.

What is a Private Placement?

Private Placement Pros and Cons

Why Invest in Private Businesses or Private Placements

Advantages of Investing in Private Placements in an IRA

Who is an Accredited Investor?

As you will lean from reading this article, the majority of the most popular types of private placement investments typically require the individual to be an accredited investor. The reason for this is that the Securities Exchange Commission (SEC), which regulates the sale of private and public type securities, believe only certain group of investors with a set of minimum income levels or net worth are in a position to require less protection provided by regulatory disclosure filings.

In general, one would satisfy the definition of an accredited investor if any of the following are true:

- An annual income of at least $200,000 for an individual or a combined annual income of $300,000 for a couple.

- A net worth of least $1,000,000 either for a single individual or combined with its spouse, excluding the value of its primary residency

- A trust that manages at least $5,000,000 in total assets, that is operated by a sophisticated individual (business-savvy)

- A legal entity whose shareholders are all accredited investors

In the case of a Self-Directed IRA, if the individual IRA or Roth IRA owner satisfies the SEC accredited investor definition, the Self-Directed IRA would then be permitted to make a private placement investment.

Types of Private Placements

The most common type of private placement investments are structured as Regulation A and Regulation D. The primary reason businesses, and funds seeking to raise capital, are committed to complying with either the Reg A or Reg D SEC regulations is because it offers less restrictive SEC regulatory requirements and offers a high level of comfort that the offering will comply with all applicable SEC rules.

Regulation A

According to the SEC, Regulation A allows companies to offer and sell securities to the public, but with a reduced level of disclosure requirements than what is required for publicly reporting companies.

Regulation A allows companies to raise money under two different tiers.

Tier 1

Under Tier 1, a company can raise up to $20 million in any 12-month period. The financial statements disclosed in a Tier 1 offering do not have to be audited.

Tier 2

Under Tier 2, a company can offer up to $75 million in any 12-month period. Financial statements disclosed in a Tier 2 offering must be audited by an independent accountant. In a tier 2 offering, if an investor, including a Self-Directed IRA, is not an accredited investor and the securities are not going to be listed on a national securities exchange upon qualification, there are some investment limitations.

Regulation D

In general, a Reg D offering does not have any monetary limit on the amount of the offering. Companies that satisfy the requirements of Reg D do not have to register their offering of securities with the SEC, but they must file electronically “Form D” with the SEC after they first sell their securities. Reg D can b broken down further into two categories: Reg D – 506(b) and Reg D 506(c).

506(b)

Under paragraph ‘b’, a Reg D company can’t solicit or advertise the offering, but it can sell the offering to an unlimited number of accredited investors and up to 35 non-accredited investors, as long as they proved to be sufficiently knowledgeable of business matters to the extent that they understand the risks associated with investing in the business.

506(c)

Paragraph ‘c’ allows a Reg D business to solicit and advertise its offering, if all the parties investing in it are considered ‘accredited investors’.

Keys to Investing in a Private Placement with a Self-Directed IRA

Understand the UBTI Rules: If a Self-Directed IRA invests in a private placement and the underlying company or investment fund is structured as a pass-through entity, such as an LLC or partnership, and not a C Corporation, the UBTI rules could be triggered

In other words, if the private placement involves investing in a business or fund that is operated via an LLC or a partnership, and the income generated by that business or fund is over $1,000 annually on a net basis, then the UBTI tax would apply. The highest UBTI tax rate is 37%, which is triggered at a low annual income threshold, of approximately $15,000.

In the case of a Self-Directed IRA, even though the IRS itself will not be the direct investor in the underlying business if the private placement investment is operated as a pass-through vehicle, the income from the underlying business or investment fund would be attributable to the Self-Directed IRA investor and could trigger the application of the UBTI tax. However, if the underlying business associated with the private placement is set up as a C Corporation, the UBTI tax rules will not apply.

Do Your Research: Anytime one makes an investment into a private placement investment, it is important to do your research on the underlying business or fund. It is advisable that, before investing your hard-earned retirement funds in a private placement that is not public, you should examine the investment documentation, the company’s management, and the financial terms of the investment.

Consider the Prohibited Transaction Rules: Internal Revenue Code Sections 408 & 4975 prohibit disqualified persons from engaging in certain types of transactions. A “disqualified person” is generally defined as the IRA holder, any ancestors or lineal descendants of the IRA holder, and entities in which the IRA holder holds a controlling equity or management interest.

In the case of most private placement investments, the IRS-prohibited transaction rules typically do not play a major role since it typically involve hundreds of shareholders, which makes the likelihood of an IRA owner owning more than 50% of the entity or fund very likely. However, if the IRA owner and any disqualified person owned more than 50% of the underlying business or fund associated with the private placement investment, the IRS prohibited transaction rules could kick in and prevent the IRA investment.

Conclusion

Private placement investments continue to be the most popular way for private businesses and investment funds to raise capital. With over $13 trillion dollars of IRA funds, Self-Directed IRAs will remain an important source of capital for these investments. It is important for Self-Directed IRA investors to appreciate the accredited investor rules, while concurrently understanding the far reach and potential impact of the UBTI rules before electing to invest in a private placement investment.

Invest in Private Placements While Staying IRS-Compliant

Investing in private placements through a Self-Directed IRA can open access to unique opportunities—but it also requires navigating rules like accredited investor status, UBTI, and prohibited transactions. Let our specialists guide you through the process and help you structure your retirement investment strategy correctly.

Schedule a Free Consultation

Open an Account

Best Long-Term Investment Strategy - Traditional vs. Alternatives?

When it comes to building a robust portfolio for the future for your retirement account, the argument between investing in traditional investments, such as stocks and bonds, or alternative assets, such as real estate, continues to ensue. While stocks have historically been the go-to for long-term wealth accumulation in one's IRA, the volatility and market dependency of stocks have prompted many investors to look elsewhere for more stable and diversified growth. Enter alternative assets - a category that includes real estate, private business stock, private equity, investment funds, cryptos, gold, and more.

In this article, we'll explore why using a Self-Directed IRA to invest in alternative assets can be a better long-term investment strategy compared to traditional investments, especially for those looking to reduce risk, maximize returns, and achieve greater portfolio diversification.

Lower Volatility, Higher Stability

Stocks are infamous for their market volatility. No one really knows why stocks go up or down. Even solid companies can experience significant stock price fluctuations based on market sentiment, economic events, or industry disruptions. For long-term investors, the constant ups and downs can be worrying and harmful to wealth-building goals for ones retirement, especially when markets take a downturn.

Alternative assets, on the other hand, tend to offer greater stability. For instance, real estate is typically less sensitive to stock market movements and tend to hold or increase in value over time, even during periods of market turbulence.

Why Stability Matters for Your Retirement:

- Real Estate: Properties, especially in strong markets, provide stable cash flow through rental income, and their value often appreciates regardless of stock market swings.

- Precious Metals: Investments in gold, silver, and other commodities often act as safe-haven assets during stock market crashes.

- Investment Funds: These investments, such as private equity, are insulated from daily market volatility, offering more predictable, long-term growth.

Enhanced Diversification and Risk Management

Diversification is a key principle of any successful investment strategy. This is especially true when it comes to one’s retirement investment plan. Relying too heavily on stocks can expose your portfolio to unnecessary risk, as stocks tend to be highly correlated with the overall market. In a market downturn, even a well-diversified stock portfolio can suffer significant losses.

Whereas alternative assets provide diversification benefits that can help mitigate this risk. By spreading investments across different asset classes, Self-Directed IRA investors can reduce their overall exposure to stock market volatility. Many "alts" have a low correlation to traditional equities, which means they may perform well when stocks are underperforming.

Benefits of Diversification for IRA Investors:

- Dissimilar Returns: Assets like real estate don’t move in tandem with the stock market, reducing overall portfolio risk.

- Risk Sharing: Holding a mix of asset types means that when one asset class declines, another may increase in value, balancing losses.

- Strong Hedge: Alternative investments can perform well during market downturns, providing a buffer against large losses in stock-heavy portfolios.

Potential for Higher Returns

While stocks can provide meaningful short-term gains, they also come with higher risks. Alternative assets, on the other hand, offer the potential for higher returns over the long term, which is perfect for IRA investors, often without the wild variations that come with equities.

For example, private equity investments have historically outperformed public markets. By using an IRA to invest in privately-held companies, investors can access high-growth opportunities that may not yet be available to public market participants. Additionally, real estate investments can provide consistent rental income, tax benefits, and long-term appreciation, all of which contribute to superior returns over time.

Why Alternative Assets Can Offer Better Returns:

- Private Investments: Offers access to high-growth companies before they go public, often delivering higher returns than stocks.

- Real Estate: Provides both income from rents and potential for capital appreciation, often outpacing inflation.

- Precious Metals: Can offer strong returns during inflationary periods or economic uncertainty, outperforming many stock sectors.

Inflation Hedge

One of the greatest challenges for long-term investors, including retirement investors, is inflation, which corrodes the purchasing power of money over time. Stocks can sometimes struggle to keep pace with inflation, particularly during periods of economic uncertainty.

Alternative assets, on the other hand, often serve as a natural hedge against inflation. Real estate, for example, tends to increase in value alongside inflation, and rents can be modified to keep up with rising costs. Precious metals like gold and silver also tend to rise in value during inflationary periods, making them a valuable addition to any inflation-conscious portfolio.

How Alternative Assets Hedge Against Inflation:

- Real Estate: Property values and rents tend to increase with inflation, helping investors maintain purchasing power.

- Metals: Gold, oil, and agricultural products often rise in price when inflation surges, providing a hedge against devaluing currencies.

- Private Company Investments: Investments in private business, such as utility and other industrial businesses tend to offer inflation-protected, stable income streams, as many contracts are tied to inflation adjustments.

Access to Exclusive Investment Opportunities

Private placements, venture capital, and hedge funds often provide access to exclusive opportunities that the average stock investor cannot reach. These asset classes are typically available only to accredited investors or through specialized investment platforms, and they offer exposure to early-stage companies, niche markets, or unique real estate projects that have the potential for significant upside. An accredited investor is an individual with at least a $1 million in net worth, excluding a primary residence, or $300,000 of annual income if married filing jointly.

By investing in alts, you gain access to assets that can deliver unique growth opportunities that are often not available in public markets.

Benefits of Exclusive Access:

- Early-Stage Investment Opportunities: Private placements and venture capital allow investors to get in early on companies with high growth potential.

- Unique Private Real Estate Projects: Investments in commercial properties, multi-family units, or real estate developments offer unique advantages over traditional real estate or REITs.

- Bespoke Market Exposure: Hedge funds and private investments allow access to niche markets and strategies, such as distressed assets, that stocks can’t provide.

Conclusion

Investing in traditional assets like stocks, bonds, and mutual funds offers liquidity, transparency, and regulatory oversight. These investments are well-established, offering investors historical data for analysis, and are typically traded on public exchanges, making them accessible. Traditional investments are relatively easy to understand and monitor, suiting both novice and experienced investors.

In contrast, alternative investments encompass assets such as real estate, private equity, hedge funds, commodities, and cryptocurrencies. These investments often offer higher returns but come with some risk and less liquidity. Alternative investments are sought for portfolio diversification and are typically favored by experienced investors seeking to hedge against market volatility.

In a perfect world, your retirement holdings should balance each other with a mix of traditional investments and alternative assets. As always, be sure to consult with a financial advisor to ensure your goals and risk levels are at a level you are comfortable with.

Expand Beyond Stocks & Bonds — Discover Alternative Assets

Whether you're sticking with traditional stocks and bonds or exploring alternative assets like real estate, private equity or crypto, choosing the strategy that fits your long-term goals matters. Our specialists at IRA Financial can help you build a diversified, tax-efficient retirement portfolio.

Schedule a Free Consultation

Open an Account

How is UBTI Applied to an IRA that Invests in a Real Estate Syndicate?

Investing in real estate through Self-Directed IRAs (SDIRAs) has gained popularity, especially with the growth of alternative investments like real estate syndicates. However, for investors using tax-advantaged retirement accounts, certain types of income generated within the IRA may trigger a tax known as Unrelated Business Taxable Income (UBTI). This article explores how UBTI applies to IRAs investing in real estate syndicates, including what UBTI is, how it’s calculated, and the implications for investors.

Understanding UBTI: What It Is and Why It Matters

UBTI is a tax levied on income that a tax-exempt entity, such as a Self-Directed IRA, earns from activities unrelated to its core purpose. IRAs are typically tax-exempt, meaning they allow funds to grow tax-deferred (in the case of a Traditional IRA) or tax-free (in the case of a Roth IRA). However, the IRS established UBTI rules to prevent tax-exempt entities from gaining an unfair competitive advantage over taxable businesses.

- UBTI Sources: UBTI is triggered when an IRA earns income from unrelated business activities, which can include:

- Operating a business

- Leveraged investment income, such as income derived from debt-financed properties

- Certain types of passive income from partnerships or LLCs

- Purpose of UBTI in IRAs: The UBTI rules aim to ensure that tax-deferred entities do not accumulate wealth through business activities in a way that undermines taxable businesses. For investors using an IRA to invest in real estate, UBTI can be a significant consideration, particularly when investments involve debt-financing or partnerships that produce operational income.

Real Estate Syndicates and IRAs: An Overview

A real estate syndicate pools funds from multiple investors to acquire properties that may be too costly or complex for an individual investor to buy alone. These syndicates often use a partnership structure, such as a Limited Liability Company (LLC) or Limited Partnership (LP), which can generate types of income that trigger UBTI in IRAs.

- Structure of Real Estate Syndicates: Syndicates are typically structured as pass-through entities, meaning that profits and losses flow through to the individual investors, who report them on their own tax returns. For IRAs, this pass-through income could potentially become subject to UBTI.

- Types of Income in Real Estate Syndicates:

- Rental Income: Generally considered passive and not subject to UBTI if there is no debt financing.

- Capital Gains: Typically not UBTI as it falls under investment income.

- Operational or Business Income: If the syndicate operates a business (e.g., a hotel or commercial property), income from operations may be considered UBTI.

- Debt-Financed Income: When syndicates use debt to acquire or improve properties, the income generated from the debt-financed portion is subject to UBTI.

How UBTI is Triggered in Real Estate Syndicate Investments

Investing in real estate syndicates through a Self-Directed IRA can trigger UBTI primarily in two situations:

- Debt-Financed Real Estate Investments: If the syndicate uses leverage, any income from debt-financed property could result in UBTI. For example, if 60% of a property was financed with a loan, then 60% of the income generated from that property is subject to UBTI.

- Business or Operational Income: If a real estate syndicate operates a business within the property, such as a commercial retail space or hotel, the income generated from these operations may be classified as UBTI. However, if the property is merely rented out without any substantial additional services, the rental income might not trigger UBTI.

Debt-Financed Income and UDFI (Unrelated Debt-Financed Income)

A specific form of UBTI called Unrelated Debt-Financed Income (UDFI) applies to IRAs when income is generated from debt-financed investments. UDFI requires the IRA to pay taxes on the portion of income related to the leveraged or debt-financed portion of the investment. The UDFI rules apply if:

- The property was acquired with debt, meaning the syndicate used a mortgage or other loan to purchase the property.

- The property generates income, a portion of which is attributable to the debt financing.

The IRS requires that UDFI be calculated based on the ratio of debt to the property’s value and applies UBTI tax to that percentage of income. For example, if a property’s value is $1 million and has a mortgage of $600,000, 60% of the income derived from the property would be subject to UBTI.

Calculating UBTI and UDFI: A Step-by-Step Example

To understand the mechanics of UBTI within a Self-Directed IRA investing in a real estate syndicate, consider the following example:

- Investment Scenario: An SDIRA invests in a real estate syndicate that purchases a commercial building for $2 million. The syndicate funds 50% of the purchase with investor equity and 50% with debt financing.

- Income Generation: The building generates $200,000 in net operating income (NOI) for the year.

- UBTI Calculation for Debt-Financed Portion:

- Debt Ratio: 50% of the property was financed by debt.

- Income Subject to UBTI: 50% of $200,000 = $100,000 is considered UBTI for the IRA since it’s the portion derived from debt financing.

- Applying UBTI Tax: The UBTI rate is calculated at the trust tax rate, which ranges from 10% to 37% depending on the income amount. Assuming a 20% tax rate on $100,000, the SDIRA would owe $20,000 in UBTI.

Filing Requirements and Tax Implications for IRAs

When an IRA is liable for UBTI, it’s the responsibility of the account custodian to file a separate tax return for the IRA—Form 990-T, which is used to report UBTI.

- Filing Form 990-T: The IRA custodian must file Form 990-T for each tax year that the IRA generates $1,000 or more in UBTI.

- Paying UBTI Taxes: Taxes are paid from the IRA’s funds, not from the account holder’s personal funds. This requirement is important because taking personal funds to cover the tax would constitute an early distribution, which could trigger penalties.

For this reason, IRA holders often weigh whether the potential for high returns offsets the tax implications of UBTI. Real estate syndicates with high leverage or operational income can significantly impact the IRA’s net returns due to UBTI liability.

Strategies for Minimizing UBTI in IRA Real Estate Investments

While UBTI can reduce the attractiveness of certain real estate syndicate investments in Self Directed IRAs, there are strategies to help minimize or manage UBTI exposure:

- Focus on Low or Non-Leveraged Syndicates: By investing in syndicates that do not use debt financing, investors can avoid UBTI on income derived from the property, as income from fully-owned real estate is generally not subject to UBTI.

- Consider Different Investment Structures: Certain real estate investments, such as Real Estate Investment Trusts (REITs), may provide real estate exposure without UBTI. REIT dividends are typically treated as passive income, which is exempt from UBTI.

- Leverage Roth IRAs: UBTI affects both Traditional and Roth IRAs. However, because Self-Directed Roth IRAs grow tax-free, paying UBTI in a Roth IRA might be more advantageous since future growth remains untaxed.

- Regular Monitoring and Reporting: Work closely with a tax advisor or CPA familiar with UBTI and real estate syndicates. They can help monitor the debt ratio, calculate UBTI accurately, and ensure timely filing and payment of UBTI to avoid penalties.

Conclusion

UBTI presents a unique challenge for Self-Directed IRA investors in real estate syndicates, particularly when debt financing is involved. While IRAs offer tax advantages for traditional investment income, these benefits do not fully extend to income generated from debt-financed real estate or business activities within a syndicate. Understanding the mechanics of UBTI, especially UDFI, and implementing strategies to minimize exposure can help investors make more informed decisions about using IRAs for real estate syndicate investments.

With careful planning and expert tax guidance, it’s possible to navigate UBTI considerations effectively, balancing the potential for higher returns with the tax implications of these investments within a Self-Directed IRA.

Make Smart, Tax-Aware Decisions with Real-Estate Syndicate Investments

When you invest your self-directed IRA into a real estate syndicate, UBTI and UDFI rules matter—and getting them wrong can erode your returns or trigger unexpected taxes. Our team is ready to help you understand how to structure these investments, calculate leveraging impacts, and stay compliant while maximizing growth.

Schedule a Free Consultation

Open an Account

Can You Gift an IRA?

Sometimes, situations arise where a family member, friend or charity needs cash and the question arises can I use my IRA to gift someone money? This article will go over the IRS rules for gifting from retirement accounts.

Key Takeaways

- Can I gift my IRA to someone else?

- No, you cannot directly gift an IRA to another person. If you withdraw funds to give as a gift, the amount will be taxable and may be subject to early withdrawal penalties if you are under 59½

- Can I use my IRA to gift money to a charity?

- Yes, if you are 70½ or older, you can make a Qualified Charitable Distribution (QCD) of up to $100,000 per year directly from your IRA to a charity. This allows you to donate tax free and satisfy your RMD if you are 73 or older.

- What are the tax benefits of gifting an IRA to a charity?

- QCDs do not count as taxable income but are also not tax-deductible.

- You can donate up to $100,000 annually, indexed for inflation.

- Married couples can each donate $100,000, for a combined $200,000 per year.

IRA Accounts

An Individual Retirement Account (IRA) is a powerful tool to help you save for retirement, while enjoying tax benefits. There are several types of IRAs, each with its own rules and advantages. Traditional IRAs allow for tax-deductible contributions; you can reduce your taxable income in the year you contribute. However, withdrawals in retirement are taxed as ordinary income. On the other hand, Roth IRAs offer tax-free withdrawals in retirement if certain conditions are met, but contributions are made with after-tax dollars, meaning there is no immediate tax break.

Other types of IRAs are SIMPLE IRAs and SEP IRAs, used by small business owners and self-employed individuals. These accounts have higher contribution limits and can be a great way to boost retirement savings. Understanding the specific rules, such as contribution limits and withdrawal rules, is key to maximizing the tax benefits of your retirement account(s).

What Can I Do with an IRA?

Other than the regular investments you can’t make with an IRA, like life insurance and collectibles, the Internal Revenue Code (IRC) prohibits any transactions with a disqualified person.