Self-Directed IRA Disqualified Persons

A Self-Directed IRA allows you to make alternative asset investments with your retirement funds. In other words, it gives you more options than just traditional investments, such as stocks and bonds. However, there are IRS regulations surrounding self-directed IRAs. This includes disqualified persons. As a result, your IRA cannot perform transactions with these people (and sometimes, organizations).

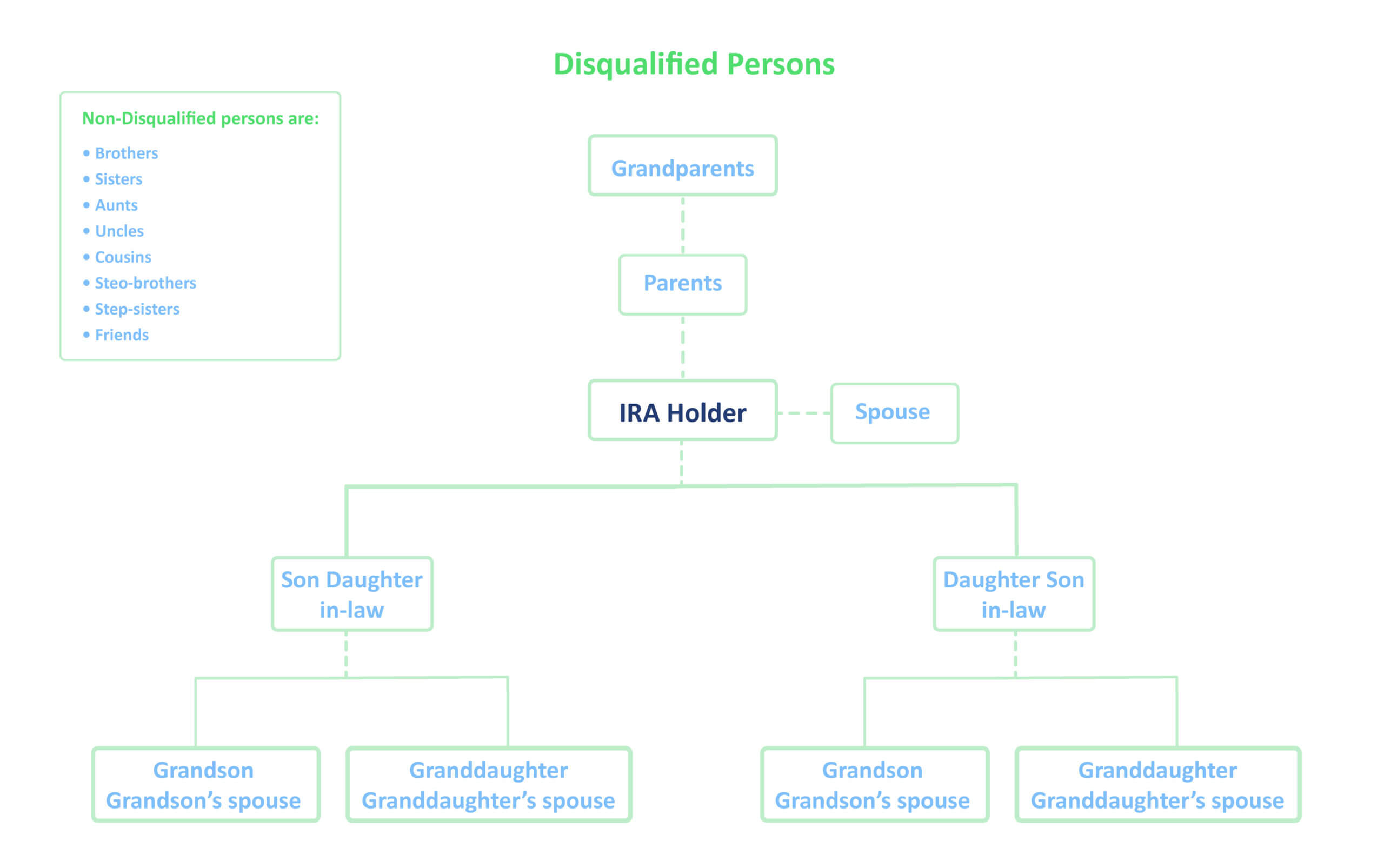

Who Are Disqualified Persons?

The IRS restricts certain transactions between the IRA and a “disqualified person.” This comes from a congressional assumption that certain transactions between certain parties are inherently suspicious. As a result, they are not allowed.

The definition generally includes you (the IRA holder), your lineal descendants and entities in which the IRA holder holds a controlling equity or management interest.

Here’s a look at who the IRS considers to be disqualified:

An In-Depth Look at a Disqualified Person

You can do so much with a Self-Directed IRA, however it’s important not to do anything that triggers a prohibited transaction. This can lead to high penalties. In order to avoid triggering a prohibited transaction with your Self-Directed IRA, make sure you know who the IRS considers “disqualified persons.” Here, we provide a more in-depth look at who and what qualifies.

- A Fiduciary (the IRA holder, participant, or person having authority over making IRA investments)

- Someone who provides services to the plan (trustee or custodian)

- A family member of the IRA holder, trustee or custodian (parents, grandparents, children, grandchildren, spouse’s of the fiduciary’s children, etc.)

- Entities of which a disqualified person owns 50%

Note: brothers, sisters, aunts, uncles, cousins, step-brothers, step-sisters, and friends are NOT treated as “disqualified.”

Application of the Prohibited Transaction Rules

In order to determine whether a transaction you wish to make is a prohibited transaction, it’s important to examine all the parties within this transaction – not simply the IRA owner.

Pursuant to Internal Revenue Code Section 4975, a Self-Directed IRA cannot engage in certain types of transactions. You can understand the types of prohibited transactions by dividing them into three categories:

- Direct Prohibited Transactions

- Self-Dealing Prohibited Transactions

- Conflict of Interest Prohibited Transactions

The Best Way to Prevent a Prohibited Transaction

When making an investment with a Self-Directed IRA, it is advisable to not engage in any transaction with a disqualified person. There is an abundance of case law that clearly states that an IRA holder can not engage in a transaction that directly or indirectly benefits a disqualified person.

Below are a few examples of common prohibited transactions involving disqualified persons:

Direct or Indirect Lending of Money between an IRA and Disqualified Person

Example: Jen lends her husband $20,000 from her IRA.

Direct or Indirect Furnishing of Goods, Services or Facilities Between an IRA and a Disqualified Person

Example: Joel buys a home with his IRA funds and personally fixes it up.

The Direct or Indirect Transfer to a Disqualified Person to Pay Mortgage or Credit Card Bills

Example: Tim is in a financial jam and takes $3,000 from his IRA to pay his mortgage and credit card bill.

Receipt of any consideration by a “Disqualified Person” who is a fiduciary for his/her own account from any party dealing with the IRA in connection with a transaction involving income or assets of the IRA

Example: Derrick uses his IRA funds to loan money to a company in which he manages and controls but owns a small ownership interest in.

Get in Touch

Do you still have questions regarding disqualified persons and prohibited transactions? Contact IRA Financial directly at 800-472-0646.

Related Articles

How IRA Financial’s New Platform Works

IRA Financial's Unified Platform combines stock and ETF trading, alternative asset investing, and cryptocurrency access inside a single retirement…

Stop Choosing Between Stocks and Alternatives. Your IRA Can Hold Both.

I get this question more than almost any other. Someone calls me, they have been self-directing for a few years, maybe they own a rental property or…

Self-Directed Retirement Providers That Let You Invest in Both Crypto and Private Equity

Can you invest in cryptocurrency and private equity inside the same retirement account? Yes! With the right self-directed retirement plan, you can…

How a Self-Directed IRA LLC Acts as Your Private Family Office

For decades, the term "family office" was reserved for the ultra-wealthy. It represented a private firm dedicated entirely to managing the…