Best Retirement Accounts for Realtors

Realtors have many options when planning for retirement. While some realtors have company-sponsored retirement plans, many realtors are self-employed. The majority of real estate agents are 1099 independent contractors. This article will explore the best retirement accounts for realtors to help decide what type of plan is best for your real estate career. Understanding these options will help you choose the best plan tailored to your personal circumstances and financial goals.

Key Takeaways

- A Solo 401(k) is the best all-around option for most self-employed realtors, offering high contribution limits, Roth features, and real estate investing flexibility.

- SEP IRAs are easy to set up and a good choice for realtors who want a simple, high-limit retirement plan without employee deferrals.

- Cash Balance Plans are ideal for high-earning realtors who want to contribute over $100,000 per year and maximize tax savings.

Introduction to Retirement Planning

As a real estate agent, planning for retirement is crucial to ensure a secure financial future. Retirement planning involves creating a strategy to save and invest for the future, taking into account income, expenses, and financial goals. A well-planned retirement strategy can help real estate agents achieve their desired lifestyle and provide financial security during their golden years.

It’s essential to consider factors such as taxable income, cash flow dynamics, and tax implications when choosing a retirement plan. Real estate agents can benefit from consulting a financial planner to create a personalized retirement plan, which may include a combination of retirement accounts, such as a SEP IRA, Solo 401(k), and regular IRAs.

Best Retirement Accounts for Realtors

There are several types of retirement accounts available to real estate agents, each with its own advantages and disadvantages. These include traditional and Roth IRAs, SEP IRAs, Solo 401(k)s, and Cash Balance Plans. Traditional IRAs offer tax-deductible contributions, while Roth IRAs provide tax-free growth and withdrawals.

SEP IRAs and Solo 401(k)s are designed for self-employed individuals and offer high contribution limits, making them suitable for real estate agents with higher incomes.

Cash Balance Plans, on the other hand, offer significant tax savings and are ideal for real estate agents who have achieved substantial success in their careers. Real estate agents can also consider alternative investments, such as real estate investments, to diversify their retirement portfolio.

Self-Employed Benefits for Realtors

A vast majority of realtors are self-employed. Accordingly, a self-employed real estate professional who operates his or her own business will receive a 1099 with the commissions earned from the real estate agency. Small business owners, including realtors, can benefit significantly from retirement plans tailored to their needs.

There are many ways a realtor can be self-employed. They can be a sole proprietor, or can establish an entity, such as an LLC, C, or S corporation. The great news is that it is now better than ever to be self-employed. Not only do you have the ability to control your work/life balance, and obtain health insurance, but you also have the opportunity to supercharge your retirement savings.

Any business can establish a SEP IRA. The key is that the individual or entity establishing the plan must have a business and not just a passive activity or hobby. For example, the individual would need to file a Schedule C on Form 1040 as a sole proprietor or single member LLC or a business tax return. In addition, only earned income from the business that adopted the plan is eligible to be contributed to a SEP IRA.

SEP IRA for Realtors

A Simplified Employee Pension IRA (SEP IRA) has traditionally been the most popular retirement plan for the self-employed and small business owner. A SEP IRA is a pure profit-sharing plan that allows the employer to make up to a 25% (20% in the case of a sole proprietorship or single member LLC) profit-sharing contribution to all eligible employees up to a maximum of $72,000 for 2026, which is a $2,000 increase from 2025. A SEP IRA does not include a catch-up contribution option when you reach age 50, which is a drawback compared to the Solo 401(k). A SEP IRA is a pure profit-sharing plan which means there are no employee deferrals. So, if you earn $100,000, the most you can put away in your SEP is $25,000.

One can set up a SEP IRA up until the business files its income tax return. Contributions must be made by the tax return deadline (including extensions). SEP IRA contributions can be made in pretax Roth.

A Roth SEP IRA allows employer contributions to be made on an after-tax basis, meaning the funds grow tax-free and qualified withdrawals in retirement are also without tax. While traditional SEP IRAs are funded with pretax dollars, the Roth SEP—made possible under the SECURE 2.0 Act—gives business owners and employees the option to pay taxes upfront for potential long-term tax-free growth.

Traditional IRA contributions are also an option for individuals who exceed the income limits for a Roth IRA, offering tax deductions for contributions made within the year. The SEP IRA is a great retirement and investment plan for a self-employed realtor.

Book a free call with a self-directed retirement specialist

- Review your self-directed retirement options

- Learn about investing in alternative assets

- Get all of your questions answered

Solo 401(k) for Realtors

The Solo 401(k) plan, also known as an Individual 401(k), has surpassed the SEP IRA as the most popular retirement plan for the self-employed. It is an IRS-approved retirement plan which is suited for business owners who do not have any employees, other than him or herself and their spouses. A Solo 401(k) plan is basically a regular 401(k) plan covering only one employee. The most popular feature of the Solo 401(k) plan is the ability to make high annual contributions. Required minimum distributions (RMDs) are mandated once the account holder reaches age 73.

To be eligible to establish a Solo 401(k) plan, an investor must meet just two eligibility requirements:

- The presence of self-employment activity.

- The absence of full-time employees.

The business owner and their spouse are technically considered “owner-employees” rather than “employees”.

In 2026, a Solo 401(k) plan participant under the age of 50 can make a maximum annual employee deferral contribution in the amount of $24,500. That amount can be made in pretax, after-tax, or Roth. On the profit-sharing side, the business can make a 25% (20% in the case of a sole proprietorship or single member LLC) annual profit-sharing contribution based on the amount of the net Schedule C amount or W-2, as applicable, up to a combined maximum, including the employee deferral, of $72,000 for 2026.

Plan participants at least age 50 can make an additional catch-up contribution of up to $7,500 as the employee increasingly the limits to $32,000 and $79,000 respectively. '

Plus, beginning in 2025, participants between the ages of 60 and 63 can take advantage of the "super" catch-up. Instead of $7,500, those individuals can increase their annual contribution by $11,250.

Solo 401(k) plans offer more control over investment choices, including the ability to invest in assets like real estate, cryptos, private placements, and more. Additionally, participants can begin taking distributions without penalties starting at age 59 1/2.

Note – if the investor reports real estate income, such as rental income, using a Schedule E on Form 1040, the real estate activity will likely not be eligible for a Solo 401(k) because it is being treated as passive versus business (Schedule C).

Related: Solo 401(k) or SEP IRA for Real Estate Investors?

SEP IRA vs. Solo 401(k): What’s Better for Realtors?

The SEP IRA is known for its ease of use. It’s ideal for realtors who want a straightforward way to save for retirement with minimal paperwork. You can contribute up to 25% of your net earnings from self-employment, up to a maximum. However, only the employer (you, as the business owner) can contribute—there are no catch-up contributions. It is best for realtors with fluctuating income who prefer a simple, low-maintenance retirement plan.

The Solo 401(k) is designed for self-employed individuals with no full-time employees other than a spouse. Unlike the SEP IRA, the Solo 401(k) lets you contribute both as the employee and employer. It also allows Roth contributions, and you can even borrow from your plan—something SEP IRAs don’t allow. This is a good option for realtors who want to contribute more, take advantage of Roth savings, or access their retirement funds via loans.

Investing in a Solo 401(k) plan also provides the flexibility to diversify your portfolio beyond traditional assets.

Bonus for Realtors: Real estate investors using retirement funds must use non-recourse loans when financing property purchases. While IRAs are subject to the Unrelated Business Taxable Income (UBTI) tax when using borrowed funds, 401(k) plans are generally exempt from this tax.

Under IRC 514, a 401(k) plan, but not an IRA, is exempt from the UBTI tax. In the case of a real estate investment, the UBTI would be triggered when an IRA uses leverage to make a purchase. Up to a 37% tax would be imposed on the income generated based off the percentage of the financed portion of the real estate property.

If you want maximum contributions and more control over your retirement savings, the Solo 401(k) is often the better choice. But if you’re looking for a low-effort, tax-deferred plan with high contribution limits, a SEP IRA may be a better fit.

Tax Implications

The tax implications of retirement plans are a critical consideration for real estate agents. Contributions to a retirement account can reduce taxable income, which can lower tax liability. The tax system operates on Marginal Income Tax Brackets, which determine the tax benefit of retirement contributions. Real estate agents can determine the tax benefit by multiplying the dollar amount contributed to their retirement plan by the marginal rate of the bracket.

Defined Benefit Plan/Cash Balance Plan

For realtors who expect to have consistent annual earnings above $150,000 for the next several years and are looking to put away over $100,000+ a year in a retirement plan, the defined benefit/cash balance plan is your answer.

A cash balance plan, a type of defined benefit pension plan, promises an employee an employer contribution equal to a percent of each year’s earnings and a rate of return on that contribution. Defined benefit plans guarantee a specific benefit at retirement to each eligible employee. In general, defined benefit plan benefits are funded over the working life of the participating employee with annual tax-deductible contributions from the employer. The employee does not make any contributions to the plan. Instead, the employer makes all contributions based on predetermined retirement benefits as outlined in the pension plan document. Based on certain complex calculations by an actuary, a defined benefit/cash balance plan can provide enormous tax benefits and retirement savings to self-employed realtors.

Conclusion

So, what is the best retirement account for realtors? For most realtors, the Solo 401(k) plan offers the greatest retirement and tax saving benefits. In addition, a Solo 401(K) plan can also contain a self-directed option allowing one to use his or her plan funds to invest in real estate as well as other traditional and alternative assets. For any realtor who expects consistent earnings above $150,000 for several years and wishes to maximize their retirement and tax advantages, the defined benefit/cash balance plan is a great option.

Retirement funds can be utilized in various investment strategies, providing significant tax-deferred income generation through real estate investments.

Realtors: Choose the Retirement Account That Works as Hard as You Do

You work hard to close deals — your retirement plan should work just as hard. Whether you want max contributions, investment flexibility (including real estate), or simplicity in setup, there’s a plan suited to your income stream and business goals. Let’s make sure you’re choosing the most powerful option for your future.

Schedule a Free Consultation

Open an Account

Swanson v. Commissioner, 106 T.C. 76 (1996): What It Still Means for IRA Entity Investments

Swanson v. Commissioner remains a landmark Tax Court decision confirming that Individual Retirement Accounts (IRAs) may form and invest in entities under certain conditions. While the case continues to be widely cited in Self-Directed IRA planning, it is important to understand both its holdings and its limitations in light of current IRS regulations and enforcement trends.

Below is an overview of the case and its ongoing relevance.

Background

Mr. Swanson, the central figure in this case, structured an investment strategy involving his IRAs and newly formed corporations. He established two corporations, with his IRAs serving as the sole shareholders. Importantly, Mr. Swanson did not personally own any stock in the corporations, although he did serve as a director.

The corporations were formed at inception with IRA ownership, and no pre-existing ownership interests were transferred to the IRAs.

Key Legal Points

Initial Formation and Stock Purchase

The Tax Court ruled that the initial formation and capitalization of the corporations by the IRAs did not constitute a prohibited transaction under Internal Revenue Code Section 4975.

Why?

The court found that the purchase of newly issued stock by the IRAs did not qualify as a sale or exchange of property between a plan and a disqualified person under Section 4975(c)(1)(A). At the time of formation, the corporations were not yet disqualified persons, making the initial transaction permissible.

This distinction applies specifically to the initial capitalization of a newly formed entity.

Dividends and IRA Assets

The court also clarified that the receipt of dividends by the IRA from the corporation was not a prohibited transaction.

Why?

Dividends did not become IRA assets until they were actually declared and paid to the IRA. As such, the payment of dividends alone did not trigger a prohibited transaction, provided the distributions were made on standard, non-preferential terms.

Management Functions

Mr. Swanson’s service as a director of the corporations did not constitute a prohibited transaction.

In other words, the Tax Court held that the performance of typical management or oversight functions, by itself, did not violate the prohibited transaction rules governing IRAs. However, the ruling did not address extensive operational involvement or the provision of personal services beyond normal corporate governance roles.

Entity Status After Formation

The Tax Court did acknowledge that after formation, the corporations became disqualified persons with respect to the IRAs.

This distinction is critical. Once the entity exists and is owned by the IRA, most transactions between the IRA, the entity, and the IRA owner are subject to strict prohibited transaction limitations. Ongoing compliance is essential to preserve the IRA’s tax-advantaged status.

Takeaway

The Swanson case affirmed that IRAs have the legal capacity to form and invest in entities without automatically triggering a prohibited transaction, provided the structure is implemented correctly at inception.

At the same time, the ruling underscores the importance of continued adherence to IRS rules after formation. While Swanson provides valuable guidance, it does not grant unlimited authority for IRA owners to control or transact with IRA-owned entities. Operational conduct, ongoing transactions, and indirect benefits remain key areas of IRS scrutiny.

Careful structuring and ongoing compliance are essential to maintaining the tax-advantaged status of IRA investments.

What is a Self-Directed Account?

A Self-Directed account in the retirement account world can mean a Self-Directed IRA or a Self-Directed Solo 401(k) plan. This article will examine the key details surrounding both the Self-Directed IRA and the Self-Directed Solo 401(k).

What is a Self-Directed Account?

A Self-Directed IRA is not a legal term that you will find in the Internal Revenue Code. A Self-Directed IRA is essentially an IRA that allows for alternative asset investments, such as real estate or even cryptocurrency. Traditional financial institutions do not allow IRAs to invest in IRS-approved alternative assets, such as real estate, because their focus is on earning fees through traditional investments. Hence, the birth of the Self-Directed IRA industry. Today, the Retirement Industry Trust Association (RITA) estimates anywhere between 4-7% of all IRAs are invested in alternative assets. Accordingly, the Self-Directed IRA is the only way one can purchase alternative assets in an IRA.

How Does the Self-Directed IRA Work?

With a Self-Directed IRA, a special IRA custodian, IRA Financial, will serve as the custodian of the IRA. All types of IRAs can be used in a Self-Directed IRA structure, such as a Traditional IRA, Roth IRA, SEP IRA, SIMPLE IRA, 401(k) rollover, and even a Coverdell and HSA.

Unlike a typical financial institution which generates fees by selling products and providing investment services, a Self-Directed IRA custodian earns fees by simply opening and maintaining IRA accounts and does not offer any financial investment products or platforms. With a Self-Directed IRA, the IRA funds are generally held with the IRA custodian. The IRA owner will then direct the IRA custodian to invest the IRA funds in IRS-approved alternative asset investments, such as real estate. Title to the Self-Directed IRA asset will be in the name of the Self-Directed IRA custodian care of the IRA owner.

A Self-Directed IRA is popular with retirement investors looking to invest in alternative assets that do not involve a high frequency of transactions, such as the purchase of raw land or private fund investments.

Types of Self-Directed Accounts

The two primary options for using a Self-Directed IRA to make alternative asset investments are the (i) full-service Self-Directed IRA and (ii) the Self-Directed IRA with “checkbook control.”

Self-Directed IRA Account Full Service

With a full-service Self-Directed IRA, a special IRA custodian, IRA Financial, will serve as the custodian of the IRA. Unlike a typical financial institution which generates fees by selling products and providing investment services, a Self-Directed IRA custodian earns fees by simply opening and maintaining IRA accounts and does not offer any financial investment products or platforms.

With a full-service Self-Directed IRA, the IRA funds are generally held with the IRA custodian. The IRA owner will then direct the IRA custodian to invest the IRA funds in IRS-approved alternative asset investments, such as real estate. Title to the Self-Directed IRA asset will be in the name of the Self-Directed IRA custodian care of the IRA owner. For example: IRA Financial Trust Company CFBO John Doe IRA.

A Self-Directed IRA that is full-service is popular with retirement investors looking to invest in alternative assets that do not involve a high frequency of transactions, such as the purchase of raw land or private fund investments.

Self-Directed IRA Account "Checkbook Control"

With a Self-Directed IRA with checkbook control, an IRA is set-up with a Self-Directed IRA custodian, such as IRA Financial. The IRA is then invested into a special purpose limited liability company (“LLC”), which IRA Financial can help you establish. The Self-Directed IRA LLC is then managed by the IRA owner providing the IRA owner with “checkbook control” over the IRA funds. With a “checkbook control” Self-Directed IRA LLC, the manager of the Self-Directed IRA LLC will have the authority to make investment decisions without the involvement of the custodian. Plus, a Self-Directed IRA LLC will offer the IRA owner limited liability protection over IRA investments. Moreover, all Self-Directed IRA investments will be titled in the name of the LLC offering the IRA owner more privacy. With a Self-Directed IRA LLC with “Checkbook Control’ you will be able to buy real estate by simply writing a check.

All types of IRAs can be transferred tax-free to a Self-Directed IRA LLC. A Self-Directed Roth IRA with “checkbook control” is popular with IRA investors seeking to invest in alternative assets, such as rental properties, fixes, and flips, tax liens, or cryptocurrencies that require a high frequency of transactions.

Why Set Up a Self-Directed IRA

The Self-Directed IRA is the most popular Self-Directed retirement solution. A Self-Directed IRA is the perfect retirement or investment vehicle for anyone looking to use their IRA funds to invest in non-publicly traded securities. The primary advantages of using a Self-Directed IRA are you gain the ability to invest in almost anything you want, diversify your retirement assets, hedge against inflation, plus generate income and gains tax-free.

The Self-Directed Solo 401(k)

A Solo 401(k) plan is not a new type of retirement plan. It is a traditional 401(k) plan covering only one employee. In general, to be eligible to establish a Solo 401(k) plan, one must be self-employed or have a small business with no full-time employees (over 1000 hours during the year) other than a spouse or other owner(s).

As the name implies, the Solo 401(k) plan is an IRS-approved qualified 401(k) plan designed for a self-employed individual or the sole owner-employee of a corporation. It works best when there are no other employees or a very small number of employees.

Unlike a Solo 401(k) plan that can be opened at a traditional financial institution, a Self-Directed Solo 401(K) plan allows one to invest in alternative assets and not just stocks, just like a Self-Directed IRA.

How Does the Solo 401(k) Plan Work

The Solo 401(k) plan documents essentially control what a Solo 401(k) plan can invest in. Not all Solo 401(k) plans are the same. For example, only a Self-Directed Solo 401(k) plan will allow you to buy alternative assets, such as real estate with your plan funds. Whereas, a Solo 401(k) plan provided by a traditional financial institution, such as Vanguard, would not permit the plan to invest in alternative assets, such as real estate.

When it comes to making investments with a Self-Directed Solo 401(k) account, the IRS generally does not tell you what you can invest in, only what you cannot invest in. The types of investments that are not permitted to be made using retirement funds is outlined in Internal Revenue Code Sections 408 and 4975. These rules are generally known as the “Prohibited Transaction” rules. Other than collectibles, and transactions that involve or directly or indirectly benefit the plan participant or a “disqualified person,” one can use their 401(k) to make the investments. A “disqualified person” is generally defined as the plan participant and any of his or her lineal descendants and/or any entities controlled by such persons.

Hence, so long as the Self-Directed Solo 401(k) account plan documents allow for real estate investments and the real estate investment does not directly or indirectly benefit a “disqualified person,” real estate is a permissible Solo 401(k) investment.

Why Should I Set Up a Solo 401(k) Account?

To be eligible to benefit from the Solo 401(k) plan, investors must meet just two eligibility requirements:

- The presence of self-employment activity.

- The absence of full-time employees.

Hence, anyone with a part-time or full-time business, whether operated as a sole proprietorship, LLC, or corporation, would generally be eligible to establish a Self-Directed Solo 401(k) account, provided the business has no non-spouse common-law employees who meet the plan’s eligibility requirements.

For more information, see the IRS guidance on One-Participant 401(k) Plans.

The following are the key reasons why the Self-Directed Solo 401(k) account is the most popular retirement plan for the self-employed or small business owner.

High Contribution Limits

With a Self-Directed Solo 401(k) Plan account, in 2026, a plan participant can make contributions up to $72,000 (70,000 in 2025) annually with an additional $7,500 catch-up contribution for those age 50 and older. Plus, if you are between the ages of 60 and 63, the catch-up contribution increases to $11,250.

Under the 2026 Solo 401(k) contribution rules, a plan participant under the age of 50 can make a maximum annual employee deferral contribution of $24,500 ($23,500 for 2025). That amount can be made in pretax, after-tax, or Roth. On the profit-sharing side, the business can make a 25% (20% in the case of a sole proprietorship or single member LLC) annual profit-sharing contribution based on the amount of the net Schedule C amount or W-2, as applicable, up to a combined maximum, including the employee deferral, of $72,000 in 2026.

For plan participants aged 50 and older, an individual can contribute an additional $7,500 in 2025, and $8,000 in 2026. That amount can be made in pretax, after-tax, or Roth. On the profit-sharing side, the business can make a 25% (20% in the case of a sole proprietorship or single member LLC) annual profit-sharing contribution based on the amount of the net Schedule C amount or W-2, as applicable, up to the maximum.

The Self-Directed Solo 401(k) account can help business owners generate tax deductions as well as sock away a significant amount of money each year.

Loan Feature

If your plan permits loans, you may borrow from the vested balance of your 401(k) account. Internal Revenue Code Section 72(p) and the 2001 EGGTRA rules allow a plan participant to borrow money from the plan tax free and without penalty. As long as the plan documents allow for it and the proper loan documents are prepared and executed, a participant loan can be made for any reason.

A Self-Directed Solo 401(k) participant can borrow up to $50,000 or 50% of their vested account balance, whichever is less. The loan must be repaid over a period of five years or less with a payment frequency no greater than quarterly. The interest rate must be set at a reasonable rate of interest, generally based on the prime rate as per the Wall Street Journal. The Interest rate is fixed based on the prime rate at the time of the loan application.

Read More: Solo 401(k) Loan

“Checkbook Control”

One of the most popular features of the Self-Directed Solo 401k Plan is that it does not require the participant to hire a bank or trust company to serve as trustee. Instead, all assets of the Self-Directed 401(k) account are under the sole authority of the Solo 401k participant.

With a “checkbook control” Self-Directed Solo 401(k) account, you have the ability to invest in traditional as well as alternative assets, such as real estate. This structure eliminates the expense and delays associated with an IRA custodian, enabling you to act quickly when the right investment opportunity presents itself. In many cases, making a Self-Directed Solo 401(k) account investment is as simple as writing a check.

Related: What is a Checkbook Control IRA?

Flexible Contribution Options

With a Self-Directed Solo 401(k) account, contributions are completely discretionary. You always have the option to try to contribute as much as legally possible, but you always have the option of reducing or even suspending plan contributions if necessary.

Roth-Type Contributions

The IRA Financial Self-Directed Solo 401(k) account contains a built-in Roth sub-account which can be contributed to without any income restrictions. In addition, our Self-Directed Solo 401(k) account allows you to take advantage of the “mega backdoor Roth” option allowing you to reach your maximum contribution limit quicker all in Roth. The Solo 401(k) “mega backdoor Roth” option is the ultimate Roth solution.

The “Backdoor Roth Solo 401(k)” strategy allows participants to use after-tax contributions to move additional retirement savings into Roth accounts. For 2026, total contributions to a Solo 401(k) plan—including employee deferrals, employer profit-sharing, and after-tax contributions—are capped at $72,000, not including applicable catch-up contributions.

After-tax 401(k) contributions are not treated as employee deferrals or employer profit-sharing contributions and may be made only to the extent permitted by the annual contribution limit and the participant’s compensation. If the plan allows, these after-tax contributions may then be converted to a Roth 401(k) or rolled over to a Roth IRA, generally without additional tax on the converted amount.

For example, a self-employed individual over age 50 earning $70,000 could contribute $31,500 as an employee deferral (including catch-up) and approximately $14,000 as an employer profit-sharing contribution, for a total of $45,500. Depending on plan design and available contribution room, the remaining amount up to the annual limit may be contributed on an after-tax basis and subsequently converted to Roth.

Cost Effective Administration

The Self-Directed Solo 401(k) account is easy to operate and administer. There is generally no annual filing requirement unless your Solo 401(k) Plan exceeds $250,000 in assets, in which case you will need to file a short information return with the IRS (Form 5500-EZ). A Form 5500-EZ is also required in the final year of the plan, regardless of the account balance.

Secret Weapon for Real Estate Investors

Pursuant to Internal Revenue Code Section 514, a 401(k) account is not subject to the unrelated business taxable income tax (UBTI) on the use of a non-recourse loan (leverage) in connection with the purchase of real estate. An IRA that uses leverage to purchase real estate would be subject to the UBTI on the debt-financed portion of the property. The current maximum UBTI tax rate is 37%.

Tax-Deferred or Tax-Free Gains

In general, all income and gains generated from a 401(k) account will flow back to the plan without tax. That means you will pay no tax on any income or gains earned by your plan investments while they are held inside the account. Traditional plan withdrawals are subject to tax, while qualified Roth withdrawals are not.

Conclusion

Over the last several years, the self-directed account has become an increasingly popular vehicle for retirement account investors looking to gain more investment freedom and greater retirement tax savings. In addition, a self-directed account is the perfect retirement or investment vehicle for anyone looking to use their retirement funds to invest in non-publicly traded securities. The primary advantage of using a Self-Directed Solo 401(k) is that the account owner gains the ability to invest in almost anything they want, better diversify their retirement assets, hedge against inflation, plus generate income and gains without tax.

What is a SIMPLE IRA? A Guide to Your Retirement Plan Options

A SIMPLE IRA, or Savings Incentive Match Plan for Employees IRA, is a retirement plan designed for small businesses. It allows both employers and employees to contribute to retirement savings, offering tax advantages and easy setup. In this article, we’ll explore how SIMPLE IRAs work, their benefits, and how to set one up.

Key Takeaways

- SIMPLE IRAs are employer-sponsored retirement plans designed for small businesses, allowing both employers and employees to contribute.

- Key features of SIMPLE IRAs include mandatory employer contributions, higher contribution limits, and substantial tax benefits for both employers and employees.

- Participation in a SIMPLE IRA requires meeting specific eligibility criteria, and the setup process is relatively simple.

Understanding SIMPLE IRAs

SIMPLE IRAs are tailored as employer-sponsored retirement plans targeting small business entities. These accounts allow both employees and employers to make contributions towards building a substantial nest egg for future financial security. The main intent behind establishing a SIMPLE IRA plans is to deliver an easy-to-manage and financially feasible method through which small business owners can offer their workforce access to a retirement savings plan.

Designed with small employers in mind who may not yet provide a retirement plan, SIMPLE IRAs stand out due to their tax benefits and the potential growth from compound interest that can considerably enhance one’s savings over time. What makes them even more appealing is the relatively low operational costs they incur when compared with other traditional forms of employee-funded retirement plans, positioning them as particularly beneficial options within smaller corporate settings.

How SIMPLE IRAs Work

SIMPLE IRAs stand out because they allow contributions to the retirement account from both employers and employees. This feature distinguishes SIMPLE IRAs from other types of retirement plans by promoting a joint effort in amassing funds for retirement. Employees have the option to allocate a portion of their earnings into their SIMPLE IRAs, while employers are mandated to contribute either by matching or through non-elective payments into the plan.

The investment choices within a SIMPLE IRA mirror those accessible in a traditional IRA, encompassing an array of options such as stocks, bonds, and mutual funds. Similarly, if you self-direct your SIMPLE, you can access an almost-unlimited array of alternative investments, including real estate, cryptos, and private placements. This is akin to the Self-Directed IRA. The versatility provided enables individuals participating in SIMPLE IRAs to shape their investment strategies around personal financial goals and risk tolerance since all investing carries inherent risks.

To maximize their potential for accumulating wealth for later years, it is crucial for both employers and staff members alike to gain insight into how SIMPLE IRAs operate effectively toward securing robust retirement savings.

Key Features of SIMPLE IRAs

SIMPLE IRAs present several compelling characteristics that render them an excellent choice for small business retirement plans. They boast contribution limits that surpass those of traditional IRAs, require contributions from employers, and provide substantial tax advantages. The combination of these attributes yields considerable advantages for both employees and their employers.

Contribution Limits

SIMPLE IRAs stand out for offering more generous annual contribution limits than traditional IRAs. Employees are permitted to allocate a portion of their earnings directly into their SIMPLE IRA each year, with a set limit determined by the IRS. In 2026, for instance, individuals below 50 years old can defer up to $17,000 of their salary into these accounts while those aged 50 and over have the advantage of making catch-up contributions that amount to an extra $4,000.

Thanks to SECURE Act 2.0, savers can contribute more to a SIMPLE IRA if he or she is between the ages of 60 and 63. This “enhanced” catch-up contribution is $5,250 making the total maximum contribution of $22,250 for this year.

Contributions made via employee salary deferrals become fully vested immediately upon depositing them into a SIMPLE IRA account. This feature is key in bolstering long-term retirement savings for employees because it includes not only personal deferred wages but also integrates additional employer matching funds as well as both employee salary deferral contributions and straightforward employee pay deductions.

Employer Contributions

Contributions from employers are an essential element of SIMPLE IRAs, and they must select one of two contribution options. They can either provide a matching contribution that equals up to 3% of the employee’s pay or opt for a non-elective deposit equaling 2% for each qualifying staff member’s compensation—regardless if the individual makes personal contributions. This design is aimed at bolstering retirement savings and promoting more widespread involvement in these plans.

Tax Benefits

SIMPLE IRAs provide significant tax advantages for employees and employers alike. For employees, contributions to a SIMPLE IRA are made with pretax dollars, which decreases their taxable income and enables their retirement savings to grow tax-deferred. This defers taxes on both the contributions and the earnings until withdrawals begin, typically at retirement.

Similarly, employers benefit from these plans because their contributions are usually deductible. The tax-advantaged nature of SIMPLE IRAs makes them an attractive option for small businesses wanting to establish a retirement plan while minimizing tax burdens.

Eligibility Requirements

Eligibility for participation in a SIMPLE IRA retirement plan is determined by specific criteria. It’s tailored to eligible employers operating small businesses with no more than 100 employees and prohibits the simultaneous operation of another retirement plan within the same tax year. This exclusivity helps maintain simpler and less restrictive eligibility standards, streamlining their approach to employee retirement benefits.

To participate, employees must have received compensation of at least $5,000 during any two previous years and anticipate an equivalent amount in the upcoming year. Eligible employers are not permitted to impose additional eligibility stipulations that are less stringent than those outlined here, thus ensuring all qualifying employees can straightforwardly join the SIMPLE IRA plan without encountering overly restrictive barriers based on their compensation or employment history.

Book a free call with a self-directed retirement specialist

- Review your self-directed retirement options

- Learn about investing in alternative assets

- Get all of your questions answered

Setting Up a SIMPLE IRA

Establishing a SIMPLE IRA for small businesses is straightforward, entailing the selection of a financial institution, such as IRA Financial, filling out necessary paperwork for the plan, and communicating to employees their entitlements. The uncomplicated nature of this procedure renders SIMPLE IRAs appealing as a fuss-free retirement planning option.

Choose a Financial Institution

To initiate a SIMPLE IRA, the initial course of action is to select a financial institution that will act as the trustee for your plan. This could be any IRS-sanctioned establishment such as banks, mutual funds companies, or insurance providers—all varying in investment choices and pricing models.

Choosing an appropriate financial institution is vital because it oversees investment management and maintains adherence to IRS regulations. Both setup costs and yearly fees associated with a SIMPLE IRA account tend to be more economical compared to those tied to 401(k) plans, presenting them as cost-effective solutions particularly suited for small businesses.

Notify Eligible Employees

Employers are required to notify eligible employees about the SIMPLE IRA plan and their rights no less than 60 days before the start of the annual election period. The notification must encompass information regarding contribution limits, how employer contributions work, and instructions for electing salary deferral contributions.

By providing this knowledge, employers guarantee that their employees have a clear understanding enabling them to make informed choices concerning their plans for retirement savings.

Establish Accounts

After selecting a financial institution and informing the employees, the next step involves creating individual SIMPLE IRA accounts for every qualified employee. The establishment of these accounts enables employees to begin their contributions towards retirement savings without delay.

Managing a SIMPLE IRA

Overseeing a SIMPLE IRA account entails handling contributions, selecting investment choices, and managing withdrawals. The straightforward nature of the plan eases the administrative burden, thus simplifying upkeep for small businesses. Specific procedures and factors must be taken into account when administering both employee contributions and employer contributions within this framework.

Employee Contributions

Workers make contributions to their SIMPLE IRA by setting aside a portion of their salary, which may be allocated among various investment vehicles like stocks and mutual funds (or alternative investments if you utilize the Self-Directed HSA structure). It is mandatory for employers to deposit these funds within a span of seven business days after deducting them from the workers’ wages, ensuring that the investments begin accruing potential earnings without delay.

Employees are granted the liberty to halt their SIMPLE IRA contributions whenever they choose. Should they opt to do so, they are only permitted to restart contributing at the onset of the subsequent calendar year. Employers bear the responsibility of providing transparent information regarding any charges or commissions associated with SIMPLE IRA investments and must communicate this during the period when employees select their contribution options.

Employer Responsibilities

When administering a SIMPLE IRA plan, employers are tasked with several obligations. It is essential for them to furnish participating employees each year with an itemized statement that outlines the aggregate contributions deposited into their SIMPLE IRA accounts. This clarity supports employees in monitoring their retirement savings and appreciating the advantages of being enrolled in such a plan.

Should there be instances where eligible employees have been erroneously omitted from participation, it becomes necessary for employers to make additional financial inputs as rectification for any overlooked deferrals. Conversely, if ineligible individuals were inadvertently included in the plan, it falls upon employers to rectify by ensuring over-contributions are duly retracted and accurately documented.

Fulfilling these duties upholds both the credibility of the SIMPLE IRA plan and adherence to regulations set forth by IRS rules.

Comparison with Other Retirement Plans

SIMPLE IRAs are just one of many retirement plan options available. A comparison with other plans like SEP IRAs and traditional IRAs can help identify the best option for your business and employees.

Here’s how SIMPLE IRAs compare to these plans:

SIMPLE IRA vs. SEP IRA

- SIMPLE IRAs and SEP IRAs are both designed for small businesses, yet they have several key distinctions.

- SIMPLE IRAs permit contributions from both the employer and the employee; only employers contribute to SEP IRAs.

- In a SIMPLE IRA arrangement, it is mandatory for employers to match their employees’ contributions, often up to 3% of the employee’s pay; SEP IRAs may provide more versatility in contribution choices.

- Both plans can be self-directed to include “alts”

The criteria for eligibility also vary between the two. SIMPLE IRAs enable employees to make contributions, whereas SEP IRAs depend entirely on employer funding. Understanding these variations is crucial when determining which plan best aligns with your company’s unique requirements.

SIMPLE IRA vs. Traditional IRA

SIMPLE IRAs are tailored for small businesses and mandate contributions from employers, contrasting traditional IRAs that any individual with earned income can establish independently of employer involvement. The contribution ceiling for SIMPLE IRAs is higher than that of traditional IRAs, especially for those of catch-up age. The compulsory nature of employer contributions within SIMPLE IRAs serves as an advantage to enhance retirement savings.

In terms of investment opportunities, both SIMPLE and Traditional IRAs provide access to a variety of options such as stocks, bonds, and mutual funds. As stated before, both individual plans, and small business IRAs can choose to self-direct opening the door to endless investment opportunities. Yet it’s the obligatory aspect of employer contributions in SIMPLE IRAs that often renders them a more beneficial choice for employees working at small companies seeking to augment their retirement reserves.

Common Mistakes and How to Avoid Them

Administering a SIMPLE IRA plan may pose certain difficulties. Mistakes often arise when employees in associated companies are not accounted for or when eligibility criteria are misapplied, potentially causing substantial problems. Implementing proper checks within payroll structures is vital to avoid such errors.

Participants must recognize that they have the ability to take out funds from their SIMPLE IRA whenever necessary. Penalties can apply for early withdrawals made before reaching 59½ years of age. To address any discrepancies that occur, employers have the option of utilizing the IRS’s Voluntary Correction Program, which offers a framework for correcting these mishaps.

Terminating a SIMPLE IRA Plan

Ending a SIMPLE IRA plan necessitates communicating with the financial institution to cease contributions in the upcoming year and conveying the decision to end the agreement. Employers are also obligated to inform their employees about the discontinuation of the plan.

While there is no mandate to report the cessation of a SIMPLE IRA plan to the IRS, withdrawals from such an account are taxable as income. Early withdrawals may result in extra penalties, especially if they occur within two years after starting participation in the plan.

Summary

SIMPLE IRAs present an uncomplicated (they are “simple” after all) and affordable avenue for retirement savings specifically tailored to the needs of small businesses. They stand out due to their generous contribution limits, obligatory contributions from employers, and substantial tax advantages, making them appealing to both business owners and their staff. Grasping who qualifies for a SIMPLE IRA, the processes involved in establishing and maintaining one, as well as its position relative to other types of retirement plans, is crucial for judicious retirement strategy decisions.

Small businesses can capitalize on the perks that SIMPLE IRAs bring forth by providing employees with robust options for accumulating funds toward their later years, thereby promoting greater financial stability upon reaching retirement age. Lastly, self-directing your SIMPLE IRA is a popular option for those who wish to offer their employees alternative investments, including real estate, precious metals, and private equity.

Ready to Set Up a SIMPLE IRA for Your Business?

If you’re a small-business owner or solopreneur with no more than 100 employees, a SIMPLE IRA offers a straightforward, tax-advantaged retirement plan with minimal administration. But the right setup matters to ensure you maximize the benefits and stay compliant. Let our experts walk you through your options and get started the right way.

Schedule a Free Consultation

Open an Account

Frequently Asked Questions

What are the contribution limits for SIMPLE IRAs?

The contribution limits for SIMPLE IRAs in 2026 are $17,000 for employees under 50 and $21,000 for those aged 50 and above. If you are between the ages of 60 and 63, you may contribute an additional $5,250.

Can employers choose not to make contributions to SIMPLE IRAs?

Employers must make contributions to SIMPLE IRAs, either through matching or non-elective contributions; they cannot opt out of this requirement.

How do SIMPLE IRAs differ from SEP IRAs?

SIMPLE IRAs permit both employer and employee contributions with mandatory employer contributions, whereas SEP IRAs are exclusively funded by the employer and allow more flexible contribution options.

Are there tax benefits associated with SIMPLE IRAs?

Yes, contributions to SIMPLE IRAs are tax-deductible, allowing for tax-deferred growth until withdrawal. This makes them a beneficial option for retirement savings.

What happens if I make an early withdrawal from my SIMPLE IRA?

An early withdrawal from your SIMPLE IRA before age 59½ may result in a 10% penalty, which increases to 25% if the withdrawal is made within the first two years of the account. It is advisable to carefully consider the implications before proceeding with an early withdrawal.

What Are the Requirements to Open a Self-Directed IRA?

A Self-Directed IRA (SDIRA) offers investors the ability to diversify retirement savings beyond traditional stocks, bonds, and mutual funds by allowing alternative investments such as real estate, private equity, private lending, cryptocurrencies, and precious metals. While the investment flexibility is broader, the requirements to open a Self-Directed IRA are straightforward and governed by the same rules that apply to standard IRAs.

This article outlines the key requirements you must meet to open and fund a Self-Directed IRA, along with important compliance considerations.

What Is a Self-Directed IRA?

A Self-Directed IRA is an individual retirement account that follows the same tax rules as a Traditional or Roth IRA but allows for a much wider range of investment options. The account must be administered by a specialized custodian who supports alternative assets and ensures the account remains compliant with IRS regulations.

Basic Eligibility Requirements

To open a Self-Directed IRA, you must meet the same eligibility standards that apply to any IRA under rules established by the Internal Revenue Service.

1. Earned Income (for Contributions)

To make new annual contributions, you must have earned income (such as wages or self-employment income). Investment income alone does not qualify.

- Annual contribution limits are set by the IRS and may be adjusted each year

- Individuals age 50 or older may qualify for catch-up contributions

- You may still open and fund a Self-Directed IRA through a transfer or rollover even if you do not currently have earned income.

Choosing the Right Type of Self-Directed IRA

When opening a Self-Directed IRA, you must choose the account type that best aligns with your tax strategy.

Traditional Self-Directed IRA

Contributions may be tax-deductible, and taxes are paid when distributions are taken in retirement.

Roth Self-Directed IRA

Contributions are made with after-tax dollars, but qualified distributions are tax-free.

Income limits apply to Roth IRA contributions, though rollovers and Roth conversions may still be permitted.

Selecting a Self-Directed IRA Custodian

A key requirement for opening a Self-Directed IRA is choosing a custodian that allows alternative investments. Not all IRA custodians offer self-direction.

The custodian is responsible for:

- Establishing and maintaining the IRA

- Executing investments at your direction

- Holding IRA assets

- Completing required IRS reporting, including Forms 5498 and 1099-R

Custodians do not provide investment advice but play a critical role in account administration and compliance.

Funding Your Self-Directed IRA

You can fund a Self-Directed IRA using several IRS-approved methods:

Annual Contributions

Contributions are subject to IRS limits and eligibility rules.

IRA Transfers

A tax-free transfer of funds from an existing IRA into a Self-Directed IRA.

Retirement Account Rollovers

You may roll over funds from:

- Traditional IRAs

- SEP IRAs

- SIMPLE IRAs (after the required holding period)

- Employer-sponsored plans such as 401(k)s, 403(b)s, and Thrift Savings Plans

Rollovers must be handled properly to avoid unnecessary taxes or penalties.

Using Your Self-Directed IRA to Invest in Alternative Assets

Once your Self-Directed IRA is properly funded through contributions, transfers, or rollovers, the account can be used to invest in a broad range of alternative assets not typically available in standard IRAs. These may include real estate, private equity, private lending, cryptocurrencies, precious metals, and other non-traditional investments, provided they are permitted under IRS rules.

Working with an experienced Self-Directed IRA provider like IRA Financial can help ensure these investments are structured correctly, processed efficiently, and remain compliant with prohibited transaction regulations.

Investment Requirements and Restrictions

While Self-Directed IRAs allow a broader range of assets, certain investments and transactions are prohibited.

Prohibited Investments

The IRS does not allow IRAs to invest in:

- Life insurance contracts

- Collectibles, including artwork, antiques, rugs, alcoholic beverages, and most coins

Prohibited Transactions

You may not:

- Personally use or benefit from IRA-owned assets

- Transact with disqualified persons, such as yourself, your spouse, parents, children, or entities you control

- Provide services to the IRA or its investments

Engaging in a prohibited transaction can result in the loss of the IRAâs tax-advantaged status.

Recordkeeping and Compliance Responsibilities

Although custodians handle administrative reporting, the account holder is responsible for:

- Performing due diligence on investments

- Ensuring all income and expenses flow through the IRA

- Maintaining proper documentation

- Understanding valuation and reporting requirements

Self-direction provides control, but it also requires careful attention to IRS rules.

Minimum and Ongoing Requirements

There is no minimum income requirement to open a Self-Directed IRA, and many custodians do not require a minimum account balance. However, investors should be prepared for:

- Account setup and annual maintenance fees

- Transaction-related fees for alternative assets

- Ongoing administrative and compliance obligations

Final Thoughts

Opening a Self-Directed IRA does not require special credentials or advanced investing experience, but it does require a solid understanding of IRS rules and a commitment to compliance. For investors seeking diversification and greater control over retirement assets, a Self-Directed IRA can be a powerful planning tool when structured correctly.

Choosing the right Self-Directed IRA custodian is critical to long-term success and compliance. IRA Financial is a leading provider of Self-Directed IRAs and Solo 401(k)s, offering deep expertise in alternative investments, strong compliance support, flexible account structures such as checkbook control, and transparent pricing with no asset-based fees. For investors seeking greater control while staying aligned with IRS rules, IRA Financial may be the right long-term partner for a diversified retirement strategy.

The Roth IRA Five-Year Rule Explained

The Roth IRA is one of the most accessible tax‑advantaged retirement accounts available to Americans. However, to fully benefit from the tax-free advantages of the plan, it is critical to understand the Roth IRA rules. For Roth IRA distributions to be tax-free, the account owner must generally be over the age of 59½ and at least one Roth IRA must have been opened and funded for a minimum of five years.

This article explores the nuts and bolts of the Roth IRA five-year rule and how it applies to contributions, earnings, and conversions.

Key Points

- Roth IRA contributions can be withdrawn at any time without tax or penalty

- Roth IRA earnings and converted amounts may be subject to the Roth IRA five-year rule to avoid taxes or penalties

- Once a distribution is qualified, Roth IRA withdrawals are tax-free

Roth IRA Basics

The Roth IRA was created in 1997 and is an after-tax retirement account. Unlike a Traditional IRA, Roth IRA contributions are not tax deductible when made. Instead, contributions are funded with after-tax dollars, and all qualified distributions are tax-free, including investment earnings.

Roth IRA contributions can be withdrawn at any time without tax or penalty. Contribution limits for Roth IRAs are the same as Traditional IRAs. For 2026, the contribution limit is $7,500, with an additional $1,100 catch-up contribution for individuals age 50 or older, subject to IRS cost-of-living adjustments.

Lastly, Roth IRAs are not subject to required minimum distributions (RMDs) during the lifetime of the account owner, allowing funds to grow tax-free for as long as desired.

Who Is Eligible for a Roth IRA?

Roth IRA rules impose income limitations on who can make direct Roth contributions. For 2026, Roth IRA eligibility is subject to modified adjusted gross income (MAGI) phase-out ranges:

- Single filers: $153,000 – $168,000

- Married filing jointly: $242,000 – $252,000

These income thresholds are adjusted periodically by the Internal Revenue Service.

Individuals who exceed these limits may still be able to fund a Roth IRA using a strategy commonly referred to as a “Backdoor Roth IRA.” This strategy generally involves making a nondeductible traditional IRA contribution and subsequently converting it to a Roth IRA, subject to the IRS pro-rata rule and other applicable tax considerations.

To fully understand how the Roth IRA five-year rule works, it is helpful to distinguish between Roth IRA contributions and Roth IRA conversions.

Roth IRA Contributions

For Roth IRA contributions, a distribution is considered “qualified” if the account owner is age 59½ or older and at least five years have passed since the first Roth IRA was opened and funded. Qualified distributions are entirely tax-free.

The method for counting the five-year period is unique. For example, a Roth IRA contribution made in April for the previous tax year is treated as though it were made on January 1 of that tax year. As a result, the earliest year a qualified distribution could occur is five tax years after that year.

Once the five-year rule has been satisfied for any Roth IRA, it is considered satisfied for all Roth IRAs owned by the individual. However, this aggregation rule does not apply to employer-sponsored Roth accounts such as Roth 401(k)s, which maintain their own separate five-year clocks.

Non-Qualified Roth IRA Distributions

If a Roth IRA distribution does not meet the requirements for a qualified distribution, either because the five-year rule has not been satisfied or the account owner is under age 59½, then the Roth IRA ordering rules must be applied to determine the tax treatment.

These ordering rules dictate which portion of the distribution is treated as contributions, conversions, or earnings, and whether taxes or penalties may apply.

Contributions

Roth IRA contributions may always be withdrawn tax-free and penalty-free at any time. For example, if a Roth IRA contribution is made on June 1, 2026, the full amount may be withdrawn as early as June 2, 2026, without tax or penalty.

Because Roth IRA contributions are made with after-tax funds, allowing these amounts to be withdrawn does not result in a tax loss to the IRS. The five-year rule does not apply to Roth IRA contributions. However, different rules apply to Roth IRA conversions.

Earnings

Roth IRA earnings represent the investment growth generated inside the account. Contributions reflect the amount deposited, while earnings consist of interest, dividends, and capital appreciation.

For example, if Mike contributes $7,000 to a Roth IRA at age 28, he may withdraw the full $7,000 at any time without tax or penalty. If the account later grows to $8,000, the $1,000 of earnings would generally be subject to income tax and a 10% early distribution penalty if withdrawn before age 59½ and before satisfying the five-year rule.

Once Mike reaches age 59½ and the five-year rule has been met, the entire Roth IRA balance, including earnings, may be withdrawn tax-free.

Roth IRA Conversions

A Roth IRA conversion occurs when pretax IRA assets are converted to a Roth IRA. The primary benefit of a conversion is the ability to move funds from a tax-deferred account, potentially subject to future taxation and RMDs, into a Roth IRA, where future qualified distributions are tax-free and no RMDs apply.

Converted amounts are included in taxable income in the year of conversion. While converted principal is not taxed again upon distribution, early withdrawals may be subject to penalties if certain requirements are not met.

Converted Amounts and the Five-Year Rule

Each Roth IRA conversion has its own separate five-year holding period. The five-year clock begins on January 1 of the year in which the conversion occurs, regardless of the actual conversion date.

If an individual is under the age of 59½, converted amounts withdrawn within five years of the conversion may be subject to the 10% early distribution penalty, even though income taxes were already paid at conversion. This penalty generally does not apply once the individual reaches age 59½.

If the account owner is age 59½ or older, converted principal may be withdrawn at any time without penalty. However, earnings associated with converted funds must still meet the requirements for a qualified distribution to be tax-free.

Ordering Rules Summary

Roth IRA distributions are deemed to occur in the following order:

- Contributions

- Conversions (on a first-in, first-out basis)

- Earnings

Careful recordkeeping is essential to determine the tax treatment of Roth IRA distributions.

Example

Jen is 45 years old and completes a Roth IRA conversion of $60,000 in 2026. Because she is under the age of 59½, she must wait five years before withdrawing the converted amount without penalty. Upon reaching age 59½ and satisfying the applicable five-year requirements, Jen may withdraw the entire Roth IRA balance tax-free.

Conclusion

Key considerations regarding the Roth IRA five-year rule include:

- Roth IRA contributions can be withdrawn at any time without tax or penalty

- Earnings require both age 59½ and satisfaction of the five-year rule to be tax-free

- Once the Roth IRA five-year rule has been satisfied, it applies to all Roth IRAs owned by the individual

- Starting a Roth IRA early helps begin the five-year clock

- Each Roth IRA conversion has its own five-year holding period

- Converted amounts withdrawn before age 59½ may be subject to penalties

- Earnings on converted amounts must meet both age and five-year requirements

The Roth IRA five-year rule can be complex, but understanding these distinctions is essential to maximizing the tax-free benefits of the Roth IRA while remaining compliant with IRS rules.

Is a Solo 401(k) Roth Employer Contribution Tax Deductible?

Thanks to the SECURE Act 2.0, which became law in December 2022, Solo 401(k) employer profit-sharing contributions can now be made in pretax or Roth. This article will explore the tax ramifications for the employee and employee in the case of employer profit-sharing contributions made in Roth. However, before we get into the Solo 401(k) employer profit-sharing contribution Roth rules, it is important to understand what a Solo 401(k) plan is and how the 2026 Solo 401(k) contribution rules work.

What is a Solo 401(k)?

A Solo 401(k) plan” is an IRS-approved retirement plan, which is designed for business owners who do not have any employees, other than themselves and perhaps their spouse. The Solo 401(k) plan is not a new type of plan. It is essentially a regular 401(k) plan covering only one employee. The Economic Growth Tax Relief and Reconciliation Act of 2001 (EGTRRA) created a strong interest in the Solo 401(k) Plan. EGTRRA added employee deferrals, the loan feature, and Roth contributions to the Solo 401(k) plan making it a far better option for the self-employed or small business owner than a SEP IRA.

Who Can Establish a Solo 401(k) Plan?

The Solo 401(k) plan may be adopted by an individual sole proprietor, or any other business entity, such as an LLC, corporation, or partnership. In general, to be eligible to benefit from the Solo 401(k) Plan, one must meet just two eligibility requirements:

(i) The presence of self-employment activity.

(ii) The absence of full-time employees.

The following types of employees may be generally excluded from coverage:

- Employees under 21 years of age

- Employees who work less than 1000 hours annually or two years of 500 hours or more

- Union employees

- Nonresident alien employees

2026 Solo 401(k) Plan Contribution Rules

Under the 2026 Solo 401(k) contribution rules, a plan participant under the age of 50 can make a maximum annual employee deferral contribution in the amount of $24,500. That amount can be made in pretax, after-tax, or Roth. On the profit-sharing side, the business can make a 25% (20% in the case of a sole proprietorship or single member LLC) annual profit-sharing contribution. in pretax or Roth, based on the amount of the net Schedule C amount or W-2, as applicable, up to a combined maximum, including the employee deferral, of $72,000.

For plan participants over the age of 50, an individual can make a maximum annual employee deferral contribution of $32,500. That amount can be made in pretax, after-tax, or Roth. On the profit-sharing side, the business can make a 25% (20% in the case of a sole proprietorship or single member LLC) annual profit-sharing contribution, in pretax or Roth, based on the amount of the net Schedule C amount or W-2, as applicable, up to a combined maximum, including the employee deferral, of $80,000 ($77,500 in 2023).

Roth Employer Profit Sharing Contribution & SECURE Act 2.0

In the case of a Solo 401(k), employer profit-sharing contributions are generally based on a percentage of compensation. For a sole proprietor or single-member LLC taxed as a disregarded entity, the contribution is calculated using a special formula that effectively allows up to 20 percent of net Schedule C income. For an S corporation or C corporation owner paid via W-2 wages, the employer contribution can be up to 25 percent of W-2 compensation.

Prior to 2023, all Solo 401(k) employer profit-sharing contributions were required to be made on a pre-tax basis. The business received a tax deduction for the contribution, and the participant did not recognize any current income. Instead, the contribution (and its earnings) would be taxed when distributed in retirement, potentially along with a 10 percent early distribution penalty if taken too soon. Because the IRS would eventually tax these funds at distribution, there was no need to impose taxation when the contribution was made.

That framework changed with the passage of SECURE 2.0 in late 2022. Among its many retirement-related provisions, SECURE 2.0 introduced the ability for 401(k), 403(b), and governmental 457(b) plans to permit vested employer matching and non-elective contributions to be treated as Roth contributions. This provision became effective after enactment, allowing plan sponsors, including Solo 401(k) plans, to offer Roth employer contributions if properly drafted.

As a result, beginning in 2023, a Solo 401(k) participant may elect to have employer profit-sharing contributions made on a Roth basis instead of pre-tax. The business remains eligible to deduct the employer contribution, but the participant must include the Roth employer contribution in taxable income in the year it is made. This immediate taxation is required because qualified Roth 401(k) distributions are generally tax-free, and the IRS must collect the tax upfront rather than at retirement.

New for 2026: Mandatory Roth Catch-Up Contributions for Higher-Income Solo 401(k) Owners

Beginning January 1, 2026, SECURE 2.0 imposes an additional Roth requirement that specifically affects catch-up contributions. If a Solo 401(k) participant is age 50 or older and had prior-year wages exceeding $150,000 from the employer sponsoring the plan, any catch-up contributions must be made on a Roth (after-tax) basis. The $150,000 threshold is indexed for inflation and is measured using prior-year Social Security wages (typically Box 3 of the W-2).

Under this rule, only the catch-up portion of employee deferrals is affected. Standard employee deferrals up to the regular annual limit may still be made on either a pre-tax or Roth basis. However, once the income threshold is exceeded, every dollar of the catch-up contribution must be Roth.

This rule applies to Solo 401(k) plans because they are still 401(k) plans under the tax code. For owners of S corporations or C corporations who pay themselves W-2 wages, the Roth catch-up requirement will clearly apply if the wage threshold is met. While the rule is more nuanced for sole proprietors without W-2 wages, most high-income Solo 401(k) owners should assume Roth catch-up contributions will be required and ensure their plan document supports Roth deferrals.

Importantly, if a Solo 401(k) plan does not offer Roth contributions at all, high-income participants will not be permitted to make catch-up contributions beginning in 2026. This makes Roth-ready plan design a critical consideration for older, higher-income business owners.

Learn More: The New 2026 Solo 401(k) Roth Catch-Up Rule: What High-Income Owners Need to Know

Items to Consider When Making Solo 401(k) Roth Employer Contributions

- Participants must election to designate as Roth.

- Roth employer contributions likely starts five-year clock, if not already started for the year income included.

- Tax reporting. Probably appear on Form W-2, box 1 in year contribution made; maybe Form 1099-R. Not clear whether these amounts count for FICA/Medicare taxes.

- The employee is responsible for taxes; the employer gets a deduction.

- Roth employer contribution shouldn’t be counted as compensation for plan purposes.

- Alternatively, Roth employer plan contribution could be done as in-plan Roth conversation and Form 1099R.

Conclusion

The SECURE Act 2.0 introduced a groundbreaking change by allowing Solo 401(k) employer profit-sharing contributions to be made as Roth contributions. While this new option gives self-employed individuals more flexibility in managing their tax strategy, it also introduces important considerations around timing, taxation, and reporting.

A Roth employer contribution is not tax-deductible, since it is made with after-tax dollars. However, it allows for tax-free growth and tax-free qualified withdrawals in retirement—an advantage for those who expect to be in a higher tax bracket later on. Business owners should weigh the immediate tax cost against the long-term benefit of tax-free income.

As the IRS continues to clarify certain reporting and administrative details, Solo 401(k) owners should work closely with a tax professional to ensure proper compliance and optimize their contributions. The ability to choose between pretax and Roth employer contributions gives self-employed investors greater control and flexibility over their retirement planning—empowering them to invest freely and retire confidently.

Ready to Take Advantage of the New Roth Employer Contribution Rules?

Thanks to the SECURE Act 2.0, Solo 401(k) owners now have more flexibility than ever—allowing employer profit-sharing contributions in Roth. Whether you’re self-employed or running your own small business, understanding how these rules impact your taxes and retirement strategy is crucial.

Schedule a Free Consultation to learn how IRA Financial can help you structure your Solo 401(k) for maximum tax efficiency and long-term growth.

Open a Solo 401(k) Account today and take control of your retirement with flexible contribution options, Roth advantages, and full IRS compliance.

The Benefits of Diversification with Real Estate IRA Investments

For decades, most retirement portfolios have been built around traditional investments like stocks, bonds, and mutual funds. While these products provide exposure to public markets, they can leave investors vulnerable to market volatility, inflation risk, and sector-wide downturns. As a result, many retirement investors are now looking beyond Wall Street to real estate and alternative assets for greater stability and diversification.

A Self-Directed IRA (SDIRA) provides one of the most effective ways to diversify a retirement portfolio with real estate while still preserving the powerful tax advantages of retirement investing. Below is a breakdown of how SDIRAs work, why diversification matters, and why real estate has become one of the most popular asset classes for retirement investors seeking long-term growth and risk management.

What Is a Self-Directed IRA (SDIRA)?

A Self-Directed IRA is a retirement account that allows investors to use their funds for IRS-approved alternative investments, including:

- Residential and commercial real estate

- Private equity

- Cryptocurrencies

- Private lending

- Tax liens

- Precious metals

- Startups and venture funds

- LLCs and partnerships

Traditional IRAs at banks and brokerages like Fidelity, Schwab, and Vanguard are limited to stocks, mutual funds, and bond products. These firms do not permit alternative assets, not because the IRS prohibits them, but because their platforms and business models are not built to support private investments.

A SDIRA gives investors the freedom to invest in what they know and trust without sacrificing IRA tax benefits.

Book a free call with a self-directed retirement specialist

- Review your self-directed retirement options

- Learn about investing in alternative assets

- Get all of your questions answered

Tax Advantages of Using a SDIRA to Buy Real Estate

One of the biggest advantages of buying real estate with a SDIRA is the powerful tax treatment:

Traditional Self-Directed IRA

Rental income and capital gains are tax-deferred. Taxes are paid later when distributions are taken.

Roth Self-Directed IRA

All gains and rental income may be completely tax-free if Roth requirements are met.

Additional benefits include:

- Profits remain inside the IRA to compound faster

- No annual income tax on rental income unless UBIT applies

- No capital gains tax at sale; Traditional or Roth tax treatment applies

Compared to taxable real estate ownership, where income and gains are taxed each year, real estate inside a SDIRA compounds more efficiently.

Why Diversification Is Essential to Retirement Planning

Diversification spreads investments across different asset classes to reduce overall risk. A portfolio invested entirely in stocks and bonds may perform well in strong markets but can suffer dramatically during downturns.

Real estate provides diversification benefits because:

- It does not move in lockstep with equity markets

- It generates income independent of stock performance

- It protects against inflation through rent increases and appreciation

- It provides tangible, income-producing value

A well-diversified IRA is more resilient during:

- Stock market corrections

- Inflationary periods

- Rising interest rate environments

- Economic slowdowns

Examples of Why Diversification Matters

Market Crash Risk

During major downturns like 2008 or 2020, stock-heavy portfolios experienced massive losses in short time frames. Meanwhile, real estate in many markets held value and in some cases continued producing rental income.

Inflation Hedge

When inflation rises, the purchasing power of cash and bond income declines. Real estate historically offsets inflation because rents and property values tend to rise alongside it.

Income Stability

Stocks may cut dividends, but real estate can continue generating monthly rental income even when public companies struggle.

Private Market Advantage

While public markets react to headlines and panic, real estate values are based on economic fundamentals like location, demand, and supply.

Two Ways to Buy Real Estate with a SDIRA

There are two primary methods for purchasing real estate inside a SDIRA:

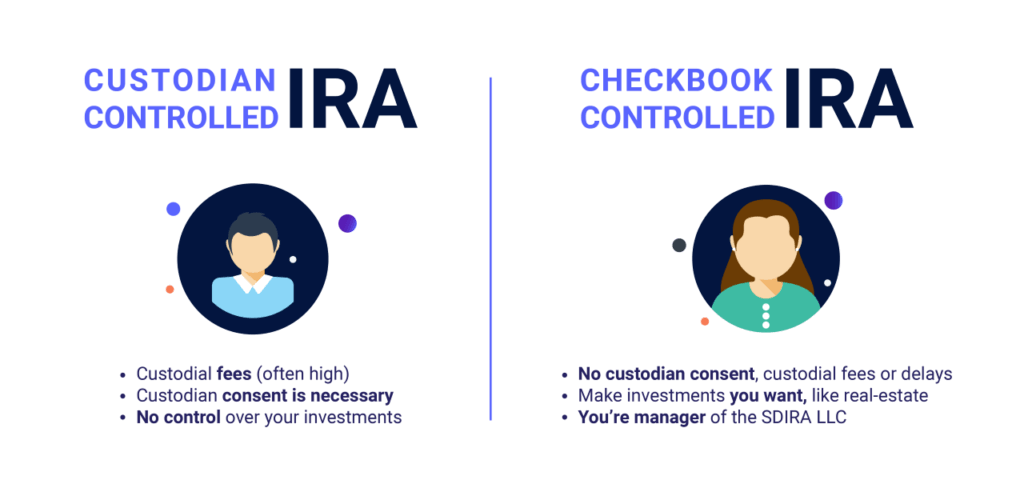

1. Custodian-Controlled SDIRA

With direct custody:

- The IRA owns the real estate

- The custodian processes all paperwork

- The investor submits instructions for every transaction

- Rent and expenses flow through the custodian

Advantages

- Simple structure

- Custodian handles administration

- Good for passive holdings

Disadvantages

- Slower transactions

- More paperwork

- Often higher transaction fees

- Less investor control

2. Checkbook Control IRA (IRA LLC)

With checkbook control:

- The IRA owns an LLC

- The LLC owns the property

- The account holder acts as manager

- The LLC has its own bank account

- Transactions occur without custodian approval

Advantages

- Immediate access to funds

- Faster closings

- Greater privacy

- Fewer custodian fees

- Simplified bookkeeping

This structure is ideal for investors buying multiple properties, engaging in private lending, participating in syndications or joint ventures, and active investors seeking efficiency and flexibility.

Why IRA Financial for Real Estate IRA Investing

IRA Financial is the national leader in Self-Directed IRAs and Solo 401(k) plans for real estate investors, serving over 27,000 clients and custodies over $5 billion in retirement assets.

What Sets IRA Financial Apart

1. Industry-Leading Legal Expertise