Socially Responsible Investing with an IRA

In recent years, socially responsible investing (SRI) has grown from a niche concept to a mainstream strategy embraced by individuals and institutions alike. It combines the pursuit of financial returns with the desire to make a positive impact on society and the environment. When integrated into a retirement plan, such as a Self-Directed IRA, socially responsible investing can align your financial future with your personal values. This article explores the concept of socially responsible investing, how it works with IRAs, and actionable steps to build a portfolio that reflects your ethical priorities. Why not start the new year on a positive note and learn about socially responsible investing.

- Socially Responsible Investing allows you to align your IRA investments with personal values, focusing on environmental, social, and governance (ESG) criteria.

- Many IRAs offer ESG-focused mutual funds, ETFs, and individual stocks, enabling socially conscious choices without sacrificing diversification.

- Go the extra mile by self-directing your retirement and invest in a broader range of assets.

What is Socially Responsible Investing?

Socially responsible investing, also known as sustainable or ethical investing, seeks to generate financial returns while promoting social and environmental good. This investment strategy considers both financial performance and a company’s adherence to environmental, social, and governance (ESG) criteria. Factors include:

- Environmental: Climate change mitigation, renewable energy, pollution control, and resource conservation.

- Social: Labor rights, diversity, community impact, and human rights.

- Governance: Ethical leadership, transparency, and shareholder rights.

The primary goal of socially responsible investing is to invest in companies or funds that align with your values, while avoiding those involved in practices you find objectionable, such as fossil fuels, tobacco, or firearms.

What is an IRA, and How Does It Work?

A Self-Directed IRA (SDIRA) is a tax-advantaged retirement account that is used to make traditional, as well as non-traditional (alternative) investments, including mutual funds, real estate, cryptos, and private placements. IRAs offer two different tax treatments:

- Traditional IRA: Contributions are tax-deductible, and earnings grow tax-deferred until withdrawal during retirement, at which point they are taxed as regular income.

- Roth IRA: Contributions are made with after-tax dollars, but qualified withdrawals during retirement are tax free, so long as you are at least age 59 1/2 and any IRA has been open for at least five years.

Furthermore, there are two types of SDIRAs which allows you to choose the type of control you need.

- Checkbook Control: With a “Checkbook IRA,” an LLC is utilized by the plan, giving you full control of your IRA funds. Consent from your custodian is not needed. You simply write a check to make an investments.

- Custodial Control: When you don’t need total control of your IRA funds, your custodian makes the investment on your behalf. Generally, investments take longer to be finalized.

Why Combine Socially Responsible Investing with an IRA?

- Align Investments with Personal Values

By incorporating socially responsible investing into your Self-Directed IRA, you can ensure your retirement savings contribute to causes you believe in, such as clean energy, equitable labor practices, or gender diversity in leadership. - Potential for Competitive Returns

Studies have shown that ESG-focused investments often perform as well as, if not better than, traditional investments over the long term. Companies with strong ESG practices tend to be better managed and face fewer regulatory and reputational risks. - Tax Advantages

Combining SRI with an IRA allows you to enjoy the tax benefits of the account while making a positive impact with your investments. - Long-Term Impact

Retirement accounts are designed for long-term growth, making them a powerful tool for driving systemic change through sustained investment in responsible companies.

Steps to Get Started with Socially Responsible Investing in an IRA

- Define Your Values and Goals – Start by identifying the issues that matter most to you. Do you want to combat climate change? Support gender equality? Promote fair labor practices? Clarifying your priorities will guide your investment decisions.

- Research ESG-Focused Funds – Many mutual funds and ETFs are designed with ESG criteria in mind. Look for funds that align with your values and have a track record of strong performance.

- Put Your (IRA) Money Where Your Mouth Is – Invest in companies that practice socially responsible investing either directly or through crowd-funding platforms.

- Monitor and Rebalance Your Portfolio – Socially responsible investing is not a set-it-and-forget-it strategy. Regularly review your portfolio to ensure it remains aligned with your values and financial goals.

Challenges and Considerations

While socially responsible investing offers many benefits, there are some challenges to be aware of:

Defining “Responsibility”

What qualifies as socially responsible can vary widely depending on personal values. For example, a company might score high on environmental issues but fall short on labor practices. It’s essential to weigh the trade-offs.

Higher Fees

Some ESG funds come with higher expense ratios compared to traditional funds. Carefully review costs to ensure they don’t erode your returns.

Greenwashing

Some companies claim to be sustainable without truly adhering to ESG principles—a practice known as greenwashing. Perform due diligence to ensure investments meet genuine ESG criteria.

Limited Options

Self-directing you retirement funds put you in control in the types of investments you can make. Just make sure to work with IRA provider who offers the one you wish to make.

The Future of Socially Responsible Investing in IRAs

The demand for socially responsible investing is expected to grow as younger generations prioritize ethical considerations in their financial decisions. Technological advancements and improved transparency in ESG reporting will make it easier for investors to assess the social and environmental impact of their portfolios. Furthermore, regulatory changes may incentivize companies to adopt sustainable practices, broadening the range of responsible investment opportunities.

Socially responsible investing with a Self-Directed IRA allows you to align your retirement savings with your values without sacrificing financial performance. By defining your priorities, researching options, and building a well-diversified portfolio, you can make a positive impact while securing your financial future. While challenges like greenwashing and limited options exist, they can be navigated with due diligence and careful planning.

Whether you’re new to investing or a seasoned pro, integrating socially responsible investing into your retirement is a meaningful way to support causes you care about while working toward your long-term financial goals. As the landscape of socially responsible investing continues to evolve, the opportunities to invest with purpose are greater than ever.

Align Your Retirement with Your Values

With a Self-Directed IRA, you can invest in assets that reflect your commitment to environmental sustainability, social equity, and ethical governance. Whether you're interested in green energy, impact funds, or community-focused ventures, our experts can help you build a portfolio that supports your principles.

Schedule a Free Consultation

Open an Account

Solo 401(k) and the UBIT Rules: What Investors Need to Know

One of the biggest advantages of using retirement funds—such as a Solo 401(k), 401(k), or IRA—to make investments is that, in most cases, all income and gains flow back to the account tax-free. This is because a 401(k) is tax-exempt under Internal Revenue Code Section 401, and Section 512 exempts most forms of investment income from taxation.

Examples of exempt income include:

- Interest from loans

- Dividends and annuities

- Royalties

- Most rental income from real estate

- Gains or losses from the sale of real estate

However, it’s not all tax-free. The IRS has rules designed to prevent retirement accounts from engaging in active business operations in ways that give them a competitive advantage over taxable entities. These rules are known as Unrelated Business Taxable Income (UBTI) or Unrelated Business Income Tax (UBIT).

Understanding UBIT is crucial for anyone investing through a Solo 401(k). Here’s what you need to know.

What Is UBIT?

UBIT is a tax on income generated by a tax-exempt entity—like a retirement account—from activities that are unrelated to its exempt purpose. For Solo 401(k)s, “unrelated” usually means income from operating an active trade or business.

Key points:

- UBIT was enacted in the 1950s to prevent charities and retirement accounts from gaining an unfair competitive advantage.

- If your Solo 401(k) triggers UBIT, income from those activities can be taxed at nearly 40% (as of 2022).

- Investing in an active business through a C Corporation generally avoids UBIT.

How UBIT Applies to Solo 401(k) Investments

The IRS looks at three key elements when determining whether UBIT applies:

1. Trade or Business

The IRS defines a “trade or business” under Internal Revenue Code Section 162, which allows deductions for expenses “paid or incurred in carrying on any trade or business.”

Examples of potentially taxable business activities through a Solo 401(k):

- Operating a restaurant or retail store via an LLC or partnership

- Manufacturing or development businesses

- Short-term real estate flipping through a passthrough entity

2. Regularly Carried On

UBIT only applies if the trade or business is regularly carried on, meaning the activity resembles how a taxable commercial enterprise operates.

- Seasonal or occasional activities are generally exempt.

- The IRS evaluates whether comparable businesses operate year-round in similar circumstances.

3. Unrelated to Retirement Purpose

The income must be unrelated to the account’s exempt purpose, which in the case of retirement accounts is retirement investing.

- Passive income like dividends, interest, and most rental income is generally not subject to UBIT.

- Active business operations, including income from an operating business through an LLC or partnership, can trigger UBIT.

UBIT Exceptions for Solo 401(k)s

While IRAs and Solo 401(k)s share similar rules, there are some important differences:

- Non-recourse real estate financing: Using non-recourse loans to buy property in a Solo 401(k) generally does not trigger UBIT, whereas IRAs might be subject to Unrelated Debt-Financed Income (UDFI).

- C Corporation investments: Solo 401(k) investments in C Corporations are usually exempt from UBIT.

Examples of Investments That Can Trigger UBIT

- Operating a business through an LLC or partnership

- Example: Your Solo 401(k) invests in a restaurant LLC. Because it is actively managed, income from operations may be subject to UBIT.

- Using margin on stock purchases

- Borrowing to buy stocks through your Solo 401(k) can generate UBIT.

- Short-term or speculative activities

- Income from flipping properties quickly through a passthrough entity may also trigger UBIT if conducted like a business.

Key Takeaways

- Most passive income (dividends, interest, royalties, rental income) does not trigger UBIT.

- Active business operations through passthrough entities can trigger UBIT, so proper planning is essential.

- Non-recourse financing in a Solo 401(k) avoids UBIT, unlike IRAs.

- Investing via a C Corporation is a common way to legally avoid UBIT.

FAQs

Q: Can my Solo 401(k) own a rental property without triggering UBIT?

A: Yes, generally. Rental income is considered passive, unless the property is financed with debt (for IRAs) or you provide substantial services, such as running a hotel or storage facility.

Q: What happens if my Solo 401(k) triggers UBIT?

A: The income subject to UBIT will be taxed at the corporate tax rate (around 40% as of 2022). Careful planning can often avoid this tax.

Q: Are all passthrough entities subject to UBIT?

A: Only if the entity generates income from an active trade or business. Passive investments like rental real estate or dividends generally do not trigger UBIT.

Q: How do I avoid UBIT in my Solo 401(k)?

A: Structure investments carefully, avoid active businesses through passthrough entities when possible, or use a C Corporation as the investment vehicle. Consult a qualified IRA or Solo 401(k) specialist to ensure compliance.

Conclusion

A Solo 401(k) is a powerful tool for retirement investing, offering tax-deferred or tax-free growth. However, understanding UBIT is critical to protecting your gains. By carefully structuring investments—especially when using LLCs, partnerships, or margin—you can maximize tax advantages while avoiding unnecessary UBIT exposure. Consulting with a knowledgeable IRA or Solo 401(k) specialist ensures your investments remain compliant and optimized for long-term growth.

Maximize Your Solo 401(k) While Staying UBIT-Compliant

Whether investing in real estate, operating a business, or exploring other opportunities, understanding the UBIT rules is essential. IRA Financial specialists help structure your Solo 401(k) investments properly, so you can enjoy the full tax advantages while avoiding unnecessary taxes.

Schedule a Free Consultation

Open an Account

Can a Solo 401(k) Reduce Self-Employment Tax?

One of the more common questions we receive from self-employed business owners seeking to establish a Solo 401(k) plan is whether it can reduce self-employment tax. The short answer is no.

In general, when one make a contribution to a Solo 401(k) plan, it’s typically after self-employment tax.

- Solo 401(k) contributions are made after self-employment tax

- Contributions will not lessen the tax you owe

- The best way to shrink your tax burden is maxing out your pretax contributions

What is Self-Employment Tax?

According to the IRS, you are self-employed if you are a sole proprietor (including an independent contractor); a partner in a partnership (including a member of a multi-member LLC), or you're in business by yourself. A sole proprietor also includes the member of a single-member LLC that is disregarded for federal income tax purposes and members of a qualified joint venture.

Usually, you must pay self-employment tax if you have net earnings from self-employment of $400 or more. Net earnings are calculated by subtracting ordinary and necessary trade or business expenses from the gross income you generate from your trade or business. You can be liable for paying self-employment tax even if you currently receive social security benefits.

If you are self-employed, your FICA tax rate for 2025 is 15.3%. The self-employment rate is the sum of a 12.4% Social Security tax and a 2.9% Medicare tax on net earnings. For 2025, the first $176,100 of your combined wages, tips, and net earnings is subject to any combination of the Social Security part of self-employment tax, Social Security tax, or railroad retirement (tier 1) tax.

According to the Social Security Administration, if you have wages, as well as self-employment earnings, the tax on your wages is paid first. But this rule only applies if your total earnings are more than the $176,100.

For example, if you will have $30,000 in wages and $45,000 in self-employment income in 2025, you will pay the appropriate Social Security taxes on both your wages and business earnings.

However, if your wages are $100,000, and you have $78,000 in net earnings from a business, you don’t pay dual Social Security taxes on earnings more than $176,100. Your employer will withhold 7.65% in Social Security and Medicare taxes on your $100,000 in earnings. You must pay 15.3% in Social Security and Medicare taxes on your first $50,000 in self-employment earnings, and 2.9% in Medicare tax on the remaining $26,100 in net earnings.

[elementor-template id="70660"]

Self-Employment Can Lower Federal Income Tax

Net earnings from income tax are considered earned income. Income that you earn includes all the taxable income and wages from working. This can be as an employee, or from running or owning a business. It also includes other types of taxable income. Earned income includes:

- Wages, salaries, tips, and other taxable employee pay

- Net earnings from self-employment

- Union strike benefits

- Long-term disability benefits received prior to minimum retirement age

Therefore, establishing a Solo 401(k) plan will help you reduce federal income tax by making pretax deductions. However, it will not reduce self-employment tax.

The Solo 401(k) for the Self-Employed

Who is eligible to set up a Solo 401(k) plan?

A Solo 401(k) plan is well suited for businesses that either do not employ any employees or employee certain employees that may be excluded from coverage. It is perfect for any sole proprietor, consultant, or independent contractor. To be eligible to benefit from the Solo 401(k) plan, investor must meet just two eligibility requirements:

- The presence of self employment activity.

- The absence of full-time employees.

The business owner and their spouse are technically considered “owner-employees” rather than “employees."

What type of business can set-up a Solo 401(k)?

Any U.S. based legal business. A business is an activity in which a profit motive is present and economic activity is involved. If you are self-employed, then using a Schedule C to report income or expenses will work. Note – if you report rental income on a Schedule E you will not be deemed to be in business since a Schedule E is for passive real estate or interest income.

Solo 401(k) Plan Advantages

The Solo 401(k) plan has become the most popular retirement plan for the self-employed for several reasons.

- High Maximum Annual Contributions: In 2025, one can contribute up to $70,000, or $77,500 if you are at least age 50.

- Loan Feature: The ability to borrow up to $50,000 or 50% of the account balance, whichever is less, to use for whatever purpose. The loan amount plus interest is paid back to the plan.

- Investment Opportunities: The ability to make traditional, as well as alternative asset investments, including stocks, mutual funds, real estate, metals and cryptos.

- UBTI Exemption: If you plan on making real estate investments, the Solo 401(k) is not subject to the UBTI tax, when using leverage to buy the property.

If you still have questions regarding the Solo 401(k) self-employment tax, or how the Solo 401(k) plan can help you to save on taxes, get in touch with IRA Financial directly by calling 800-472-0646.

The Rollins Case & The Self-Directed IRA Prohibited Transaction Lesson

Rollins v. Commissioner is an important case in the Self Directed IRA LLC context because it illustrates how one can engage in a prohibited transaction with an entity even if the entity is not a disqualified entity per se. The Rollins case also is important for examining whether a potential transaction could be considered an indirect prohibited transaction under Internal Revenue Code (IRC) 4975.

The Facts of the Rollins Case

The facts in Rollins are as follows: Mr. Rollins owned his own CPA firm. He was sole trustee of its 401(k) plan. Mr. Rollins caused his plan to lend funds to three companies in which he was the largest stockholder (9% to 33%), but not controlling, stockholder. The companies had 28, 70, and 80 other stockholders respectively. Mr. Rollins made the decision for the companies to borrow from his 401(k) plan. The loans were demand loans, secured by each company’s assets. The interest rate was market rate or higher. Mr. Rollins signed loan checks for his plan and signed notes for borrowers. All loans were repaid in full.

Mr. Rollins acknowledged that he is a disqualified person with regard to the plan because he owns Rollins, the CPA Firm, but he contends that (1) none of the corporations that were the borrowers was a disqualified person, (2) none of the loans was a transaction between him and the plan, and (3) he “did not benefit from these loans, either in income or in his own account."

Download the PDF for the Rollins Case: T.C. Memo. 2004-260

Mr. Rollins further claimed that no prohibited transaction occurred because: (1) the interest rate was above market interest and was paid, (2) the collateral was safe and secure and the principle was repaid, and (3) the plan’s assets were thereby diversified and thus the plan’s portfolio’s risk level was “significantly lowered."

The IRS Position

On the other hand, the IRS took the position that Mr. Rollins's ownership interest in these companies created a conflict of interest between the plan and the companies, resulting in dividing his loyalties to these entities. This conflicting interest as a disqualified person who is a fiduciary brought petitioner within the prohibition against dealing “with the income or assets of a plan in his own interest or for his own account” - I.R.C. § 4975(c)(1)(E).

The Tax Court held that a IRC Section 4975(c)(1)(D) indirect prohibition did not require an actual transfer of money or property between the plan and the disqualified person. The fact that a disqualified person could have benefited because of the use of plan assets was sufficient. The Tax Court held that the transactions were uses by Rollins or for his benefit, and were assets of the plan. These assets of the plan were not transferred to Rollins. For each of those transactions, however, Rollins sat on both sides of the table. Rollins made the decisions to lend the plan’s funds, and Rollins signed the promissory notes on behalf of the borrowers.

Understanding the Prohibited Transaction Rules

One of the more interesting parts of the Rollins case was the Tax Court’s emphasis that as the taxpayer, the burden of proof as to whether an indirect prohibited transaction had occurred is the responsibility of the taxpayer. In other words, at its core, the Rollins case is a "burden of proof" case that illustrates the breadth of the application of 4975(c)(1)(D) as well as the difficulty of meeting that burden of proof. Mr. Rollins was not a majority owner of any of the borrowers, but he was the largest shareholder for each company. Further, he also signed the notes for each borrower.

Would the same decision have been made if Mr. Rollins was not the largest shareholder or had not, as the Court put it, “sat on both sides of the table” (e.g., by not signing the notes on behalf of the borrowers)? It’s not entirely clear if that would have influenced the Court since it was still Mr. Rollins’ burden (as the disqualified person) to prove that the transaction did not enhance or was not intended to enhance the value of his investments in the borrowers. That seems to be a very tough burden to meet. Moreover, as the Court noted, the fact that a transaction is a good investment for the plan has nothing to do with the problem.

The lesson is that caution should be exercised whenever a disqualified person is sitting on both sides of the table!

Conclusion

In general, one can use a Self-Directed IRA to transact with a business that they own a majority share of. However, the Rollins case is a good example of the type of argument the IRS could make if they believe the Self-Directed IRA made the investment and the investment did not exclusively benefit the retirement account. In other words, an IRA investor should not make any investment that in anyway directly or indirectly benefits themselves or any disqualified person personally.

In the Rollins case, if Rollins had better facts and was able to show that the companies had other loan options or did not need the loan to survive, the IRS would have had a far tougher time in proving their case that Mr. Rollins engaged in a self-dealing IRS prohibited transaction. It is all important to note that Mr. Rollins has the burden of proving by a preponderance of the evidence that the loans did not constitute uses of the plan’s income or assets for his own benefit.

The Rollins case is a great example of the importance of working with a company that has the expertise to structure a Self-Directed IRA investment without triggering the IRS prohibited transaction rules.

Using a Self-Directed IRA for Promissory Notes

IRA Financial's Self-Directed IRA allows you to use your retirement funds to invest in promissory notes and loans directly from your mobile device through our app or directly through your computer. With our Self-Directed retirement plans you no longer need a third-party IRA custodian involved in every aspect of your investment transaction. Furthermore, you can rollover, deposit, or transfer funds between your investment and IRA seamlessly and without delay.

Benefits of Investing in Promissory Notes/Hard Money Loans

In general, a note (or promissory note as it’s often called) is simply a promise to pay. If you lend money to a third party, a document is created that dictates the terms of the loan that says the borrower will pay back the lender. A note can either be secured or unsecured. Some examples of common notes are:

- Mortgage Loans

- Personal Loans

- Business Loans

- Real Estate Loan (Hard Money Loans)

- Treasury Notes

- Peer-to-Peer Loans

When you open a Self-Directed IRA with IRA Financial you can invest in a wide range of alternative investments for a flat annual fee. While some companies limit you to precious metals and cryptos, IRA Financial allows you to invest in what you know.

Learn More: Self-Directed IRA For Real Estate

Related: Alternative Investments in an IRA

Secured or Unsecured Notes

When it comes to notes, it’s important to understand the idea of secured vs. unsecured notes.

A secured note essentially means that if someone defaults on the loan, the lender receives something in return as payback. The note is “collateralized.” In the case of a mortgage, the loan is collateralized against the actual home. If you default on your mortgage payments, the bank will foreclose on the property and take ownership.

On the other hand, if you fail to repay a non-secured-backed note, the lender has no legal recourse against the borrower. No collateral is repossessed or foreclosed.

Therefore, when making note investments with a self-directed IRA, it is important to consider whether the loan will be secured or unsecured. A secured loan offers the borrower more security and protection in the case of a borrower default.

Hard Money Loans

A hard money loan is simply a loan that is backed or secured by an asset, such as real estate. For example, a real estate developer who wants to develop a property seeks out investors to help finance the project. Since 2008, for many small real estate developers or general partners, acquiring bank financing in these circumstances still remains quite difficult.

Hence, the real estate developer or general partner may then look to secure a loan from a hard money lender, such as a self-directed IRA investor who is willing to give them the money that is secured by the underlying real estate asset(s) connected with the real estate project. If the borrower defaults on their loan, the lender would have the legal rights to the real estate secured by the loan.

Peer-To-Peer Loans

The Peer-to-peer lending industry has increased in popularity significantly over the last 10 years. Peer-to-peer lending platforms such as Lending Club and Prosper allow investors to invest in notes offered by the site.

Under a traditional peer-to-peer lending platform, borrowers are matched directly with investors through a lending platform. Investors can see and select exactly which loans they want to fund. Peer-to-peer loans are most commonly personal loans or small business loans. The majority of peer-to-peer loans are not secured, or asset-backed.

Small Business Loans

When a small business or start-up business needs working capital or seed capital, it is common to look for investors to either invest in the company in the form of equity (stock) or debt (loan). In most cases, if a small business cannot acquire financing through a bank, they may have to seek out private investors, such as self-directed IRA investors. Small business loans can either be secured or unsecured.

Tax Advantages

The advantage of using retirement funds to invest in notes/loan investments is that all the income and gains generated by the debt investment would not be subject to any tax or penalty. Instead of paying tax on the returns, such as interest, associated with the debt investment, tax is paid at a later date, leaving the investment to grow unhindered. Using a self-directed IRA to make a loan or invest in a debt instrument is tax advantageous. The tax on the interest payments can be deferred in the case of a pretax IRA or exempted permanently in the case of a Roth IRA.

In addition, self-directed IRA investments are made when a person is earning a higher income and is taxed at a higher tax rate. Withdrawals are made from an investment account when a person is earning little or no income and is taxed at a lower rate.

Read More: Tax Deferral vs. Tax Free

Why Use an IRA to Invest in Notes/Loans?

Unfortunately, none of the major financial institutions will allow you to use IRA or 401(k) plan funds to invest in Notes/Loans or essentially anything outside of Wall Street. The reason for this is simple: banks do not make money when you invest in non-traditional equities, such as private loans. They make money when you buy stock, mutual funds, and other financial products they market. As a result, a large number of individuals are turning to a Self-Directed IRA to invest in notes or other debt instruments.

Unrelated Business Taxable Income

In general, almost all retirement account investments generating passive income will not be subject to Unrelated Business Taxable Income (UBTI) or Unrelated Debt Finance Income (UDFI) Tax.

The UBTI tax is only triggered if:

- Retirement account uses margin to buy stock

- Retirement account invests in an active business through a pass-through entity, such as an LLC

The UDFI tax is triggered if:

- An IRA uses a non-recourse loan (real estate acquisition financing to purchase real estate)

- Exemption for 401(k) plans

- IRC 514(c)(9)

The UBTI & UDFI Trigger the Same Tax Rate

Because the UBTI and UDFI trigger the same tax rate, which is a maximum of 37% for 2024, if you plan to invest into loan/debt related investments using a self-directed IRA and the underlying investment will not involve an investment into a business operated via a pass-through entity, such as an LLC, has debt or margin, then the UBTI tax rules will likely not be triggered.

Your IRA Financial assigned specialist will help you understand the potential application of the UBTI/UDFI tax rules and potentially reduce or eliminate it.

Read More: How to Calculate Tax on UDFI

Act Quickly on Investments

With a Pocket IRA for notes/loans, you will have the power to act quickly on a potential investment opportunity. When you find an investment that you want to make with your IRA funds, as manager of the Checkbook IRA LLC, simply write a check or wire the funds straight from your Self-Directed IRA LLC bank account. The Pocket IRA for notes/loans allows you to eliminate the delays associated with an IRA custodian, enabling you to act quickly when the right investment opportunity presents itself. In addition, with the Pocket IRA structure, all income and gains from IRA investments will generally flow back to your IRA LLC tax-free. Because an LLC is treated as a pass-through entity for federal income tax purposes and the IRA, as the member of the LLC, is a tax-exempt party pursuant to Internal Revenue Code Section 408, all income and gains of the IRA LLC will flow-through to the IRA tax-free!

How Does Investing in Notes/Loans Work?

IRA Financials Self-Directed IRA is an IRS approved structure that allows one to use his or her retirement funds to make debt and other investments tax-free and without custodian consent. The process is simple and can be completed in a few easy steps:

- Establish a Self-Directed IRA with IRA Financial & Capital One online through our mobile app. You will need to decide if you want a traditional Self-Directed IRA or an IRA LLC.

- Your IRA cash/assets can be rolled over to IRA Financial Trust tax-free directly from our mobile app. Alternatively, you can fund your new Self-Directed IRA directly with your bank account. In 2024, individuals under 50 can contribute $7,000 per year. Individuals age 50+ can add $8,000 to their Self-Directed IRA annually.

- If you pursue a traditional IRA, you can begin investing directly from our app. However, if you pursue an IRA LLC, there are a few additional steps you will need to take:

- As manager of the LLC, you will open a bank account for the LLC at any local bank. IRA Financial will draft an LLC Operating Agreement identifying you as manager of the LLC and the IRA as the sole member.

- You, as manager of the LLC, will then have checkbook control over all the assets/funds in the IRA LLC to make the debt/note investment. Because the LLC is owned 100% by an IRA, it will be treated as a disregarded entity for tax purposes. There is no need to file a federal income tax return and all income and gains will flow back to the IRA without tax.

With IRA Financial's Self-Directed IRA, you will have the power to act quickly on a potential investment opportunity. When you find an investment that you want to make with your IRA funds, as manager of the Checkbook IRA LLC, simply write a check or wire the funds straight from your Self-Directed IRA LLC bank account. The Pocket IRA for notes and loans allows you to eliminate the delays associated with an IRA custodian, enabling you to act quickly when the right investment opportunity presents itself.

In addition, with the Self-Directed IRA structure, all income and gains from your IRA investments will generally flow back to your IRA LLC tax-free. Because an LLC is treated as a pass-through entity for federal income tax purposes and the IRA, as the member of the LLC, is a tax-exempt party pursuant to Internal Revenue Code Section 408, all income and gains of the IRA LLC will flow-through to the IRA tax free!

Read More: Promissory Note Checklist

Most Popular Debt Investments

The following debt investments have been popular with our self-directed IRA clients in 2019:

- Hard money loans to real estate investors - secured

- Hard money loans to real estate investors - unsecured

- Private business loans

- Peer-to-peer loan platforms

- Mortgage notes

3 Tips to Protect Your IRA From Creditors

Protect Your IRA

For many Americans, their retirement account is often their most valuable asset. There are approximately $65 million IRAs totaling over $13 trillion in IRAs (individual retirement accounts). Additionally, there are over $33 trillion in qualified retirement funds.

How can you protect your IRA from creditors? First, it’s important to remember that creditor protection can depend on whether you have entered into bankruptcy protection or not.

Most often, if an individual IRA holder is not under bankruptcy protection, state law will generally dictate to what degree the IRA will be protected from a creditor attack. In the case of bankruptcy, the 2005 Bankruptcy Abuse Protection Act generally offers a $1 million exemption for IRAs.

Here are three tips to remember to protect your IRA from creditors.

1. Is Bankruptcy an Option?

It's extremely important to decide whether to elect for bankruptcy protection. This is not a decision you can take lightly. We recommend that you consult with a bankruptcy attorney before you make the decision. With the Bankruptcy Act, your IRA may receive greater protection from creditors inside of bankruptcy than outside of bankruptcy.

If your state has opted into the Act, the law provides debtors in bankruptcy with an exemption for retirement assets in:

- Qualified plans

- Qualified annuities

- Tax sheltered annuities

- Self-employed plans

Additionally, the law exempts all assets in an IRA that are attributable to rollovers from a retirement plan described above. If you have a traditional IRA or Roth IRA that contains assets that are not attributable to a rollover from another type of retirement plan (i.e., the assets are from amounts you contributed directly to the IRA), then you may be allowed an exemption of up to $1,512,360 million total for the assets in those contributory IRAs.

2. State of Residence

Your state of residency may dictate whether your IRA is protected from creditors outside of bankruptcy. In bankruptcy, your state of residence is also relevant in determining the scope of creditor protection you may receive. This is because some states have opted out of the 2005 Bankruptcy Act.

Whether you are a resident of California, New York or Florida may impact how your individual retirement account is protected from creditors inside or outside of bankruptcy.

Find out whether your state has opted into the 2005 Bankruptcy Act.

Read More: Asset & Creditor Protection by State

3. Self-Directed IRA LLC

The general rule in all states is that creditors cannot take the assets of an LLC to pay off personal debts or liabilities of the LLC's owners. In other words, if you (IRA owner) owns 100% of an LLC, a creditor of the LLC cannot go after your IRA assets outside of the LLC.

This is one of the benefits of using an LLC that your IRA completely owns.

Related: Why Hasn't my CPA Heard of a Self-Directed IRA?

Charging Order

A "charging order" allows an entity to place a lien and seize money from an individual who owes, but is also owner of an LLC—for example, the individual retirement account. It is usually one of the only ways a creditor can receive income or profits from an LLC that may otherwise be distributed to the LLC member/debtor. Creditors with a charging order can only obtain the owner-debtor's financial rights. They cannot participate in the management of the LLC.

In a single-member LLC, foreclosure on the debtor's interest may occur in addition to the grant of a charging order. This allows the proceeds to be used to satisfy the creditor's judgment claim. In other words, a Self-Directed IRA LLC can be helpful in protecting your IRA from creditors, although a charging order can threaten an IRA LLC and its assets.

However, when you form a Self-Directed IRA LLC, it could provide an even greater shield against creditor attacks. Nevada LLC law states that the charging order is the exclusive legal procedure that personal creditors of Nevada LLC members can use to get at their LLC ownership interest. Therefore, unlike some other states, Nevada doesn't permit an LLC owner's personal creditors to foreclose on the owner's LLC ownership interest. Additionally, creditors cannot get a court to order for the LLC to be dissolved and its assets sold. As a result, Nevada is seen as a favorable state for individual IRA investors seeking maximum asset creditor protection.

Related: Solo 401(k) Assets & Creditor Protection

Get in Touch

Do you still have questions on how to protect your IRA from creditors? Contact IRA Financial Group directly at 800-472-0646. We're here to assist you. Additionally, you can connect with an IRA specialist by filling out the contact us form.

IRA Transfer and Rollover Rules

IRAs are very flexible retirement plans, far more than defined contribution plans, such as a 401(k). An IRA owner can transfer funds directly from one IRA to another at anytime without tax or penalty. Furthermore, one can take an IRA distribution anytime without restriction, subject to income tax and a 10% early distribution penalty (if applicable), but nonetheless still have the flexibility to do so. On the flip side, one will generally need a plan triggering event, such as reaching the age of 59 1/2 or termination of employment, to gain access to 401(k) funds for purposes of rollover of distribution.

This follow will explain the IRA transfer and rollover rules, the difference between the two, and when you can execute them.

IRA Transfer Rules

One can transfer funds (cash) or assets (such as stocks or real estate), from one IRA to another IRA at anytime without limitations. IRA-to-IRA transfers are tax free and can be done anytime. An IRA transfer can be direct or indirect.

A direct transfer is between IRA custodians (financial institutions). For example, moving your IRA at Schwab to an IRA at Fidelity. A direct transfer can be done as many times as you wish during the year with no limitation.

An indirect transfer occurs when the IRA funds are first sent to the IRA owner before re-contributing them to a different IRA within 60 days. During the 60-day period, the IRA owner is free to use the funds for any purpose without limitation. However, if the IRA owner fails to return the funds within that time period, the portion of the IRA cash or assets not returned would be subject to income tax and a 10% early withdrawal penalty if applicable. If the IRA owner withdrew cash he or she must return cash and not an in-kind asset. Indirect transfers can only be done once every 12 months.

IRA Rollover Rules

To permit tax-free transfers of retirement savings from one type of investment to another, as well as to increase the portability of qualified plan rights for employees moving from one job to another, Congress included a complicated web of rollover provisions in ERISA. These provisions cover transfers from one IRA to another, transfers from qualified pension, profit-sharing, stock bonus, and annuity plans to IRAs, and transfers from IRAs to qualified plans. In general, a rollover of retirement funds to an IRA is tax free. Rollovers can either be direct or indirect. A direct rollover can be done without limit, whereas an indirect rollover can only be done once every 12 months

The IRA rollover rules are essentially the same as the transfer rules. The main difference between a transfer and rollover is that an IRA transfer is solely between IRAs, whereas a rollover is between and an IRA and another retirement plan, such as a 401(k). Note: a Roth IRA cannot be rolled into a 401(k) plan.

When one wishes to rollover funds from a 401(k) plan or other defined contribution plan to an IRA, there are plan restrictions that must be respected. In general, you need a triggering event to roll funds out of a 401(k) plan, which typically consists of one of the following: you are over the age of 59 1/2, you leave your job, or the company terminates the plan. If funds are rolled directly from a 401(k) plan to an IRA, there is no tax or penalty. Furthermore, there may be a 20% withholding tax on 401(k) funds that are being indirectly rolled over.

Self-Directing Your IRA

Whether you are rolling over a former employer 401(k) plan, or transferring IRA funds from a different custodian, the process if the same when you wish to self-direct your retirement funds. Obviously, you need to first decide on a custodian that allows for alternative investments, such as IRA Financial. Once you choose a custodian, you can then follow the instructions discussed here to get your new Self-Directed IRA funded.

Remember, you cannot invest in alternatives, such as real estate and precious metals, without the proper custodian. You cannot simply go to your bank and expect to make any investment you wish! Due your research before choosing a custodian. Make sure they allow the investments you wish to make.

IRA Transfer and Rollover Rules - Conclusion

The IRA transfer and IRA rollover are basically one-in-the-same. The end result is moving funds from one retirement plan to another. If you are eligible to move funds, you may do so directly without much help, or indirectly, if you wish to access those funds for a small period of time.

There are two main reasons for moving funds. First, you separate from your job and wish to move 401(k) funds out of a former employer plan. A Rollover IRA is probably your best choice. Secondly, you may want to make different investments than what your current provider offers. This is where self-direction comes into play.

So long as you follow these basic guidelines, most retirement investors will have the ability to move his or her funds wherever they wish and make the investments they want.

Qualified Purchaser, Accredited Investor & the Self-Directed IRA

In the case of some of the more popular Self-Directed IRA investments, such as private equity, hedge funds, venture capital, real estate, private placements, and private stock, being an accredited investor or qualified purchaser may determine whether your Self-Directed IRA would be permitted to invest in the deal. This article will explore how the qualified purchase and accredited investor rules work and then apply how those rules could impact the type of investments that an investor could potentially make with a Self-Directed IRA.

Who is a Qualified Purchaser?

In general, certain investments will require an investor to either be a qualified purchaser or an accredited investor. For example, an investor who satisfies the qualified purchaser or accredited investor rules would be able to invest in certain investments that are not registered with the SEC. These rules are aimed to protect investors from more sophisticated and illiquid investments into non-publicly traded securities, such as an interest in a private equity fund not listed on a public exchange.

A qualified purchaser is basically a person or a family business that holds investments with a value exceeding $5 million. However, the investments that go towards determining the $5 million value cannot include a primary residence, nor property used in the normal conduct of business. Moreover, it is common for an individual or entity who is a qualified purchaser to hold $25 million or more in assets under the qualified purchaser exemption rules. Additionally, a trust can also be a qualified purchaser status if it has assets with a value of $5 million or more and is owned by at least two close members of a familial unit.

The Benefit of Being a Qualified Purchaser

Under the 1940 Investment Company Act, privately held corporations or trusts engaged in the business of pooling capital from investor in securities. The primary advantage of of marketing a fund only to qualified purchasers is that the fund would be exempt from regulation under the "40 Act." Hence, any investment company that are solely targeting qualified purchaser investors would be exempt from tedious regulation under the 40 Act.

Qualified Purchasers and The Investment Company Act of 1940

Privately held capital firms are considered investment companies under the 1940 Investment Company Act (“the ‘40 Act”) rules when they seek to raise capital from the public where qualified purchasers are not the only owners of their outstanding securities.

The ‘40 Act considers qualified purchasers to be those who meet the criteria outlined above. This, in turn, means funds selling only to qualified purchasers are exempt from regulation under the ’40 Act. In other words, investment companies are not required to observe certain SEC requirements when they choose to work exclusively with qualified purchasers. Thus, the primary advantage of being a qualified purchaser is one would have the ability to invest in a diverse and wide range of investments that are far broader than those investments available to accredited investors.

What is an Accredited Investor?

Under Rule 501(a) of the Securities Act of 1933, an accredited investor is one who has a net worth exceeding $1 million dollars, individually or jointly as a married couple. The $1 million amount excludes one's primary residence. Additionally, one can satisfy the accredited investor rules if one has earned at least $200,000 ($300,000 if married filing jointly) in income for two consecutive years immediately prior to the year in question where accreditation is sought. Additionally, an individual can be deemed an accredited investor by having a FINRA Series 7, Series 65, or Series 82 financial securities license

The primary benefit of satisfying the accredited investor rules is that one can invest in most investment funds and private placements. That is because funds that are offering for sale unregistered securities, such as private equity funds, private placements, real estate funds, are allowed to sell only to accredited investors, who according to the SEC are in a better financial position to handle the risk associated with a non-publicly traded investment.

Read More: Can My Self-Directed IRA be an Accredited Investor?

Interplay Between Qualified Purchaser & Accredited Investor Rules

In general, all qualified purchasers will satisfy the accredited investor rules, but not all accredited investors will satisfy the qualified purchaser rules. The reason is because a qualified purchaser must have at least $5 million in net worth, excluding a primary residence, which is higher than the $1million threshold for an accredited investor. Furthermore, being a qualified purchaser will offer an investor even greater investment optionality than an accredited investor. For example, certain large and highly successful investment funds will only allow qualifying purchaser investors and will not open the fund to accredited investors.

Self-Directed IRA & Qualified Purchasers/Accredited Investors

Since an IRA is a retirement account and not a natural person, the SEC will look to the IRA owner to determine whether the IRA can make the investment in satisfaction of the qualified purchaser or accredited investor rules. In other words, the IRA itself does not have to have over $1 million in assets to be deemed an accredited investor or over $5million to be a qualified purchaser. The IRA owner would be the one responsible for satisfying the net worth test or the annual income requirement.

Making a Self-Directed IRA Investment as a Qualified Purchaser/Accredited Investor

Now that you hopefully understand the rules and requirements involving in determining whether you are a qualified purchaser or accredited investor, it is important to identify whether the IRA investment into a fund or private placement could be subject to tax.

In general, when it comes to using a Self-Directed IRA to make investments, in almost all cases, all income and gains would be exempt from federal income tax. This is because an IRA is exempt from tax pursuant to Internal Revenue Code Section 408. Furthermore, IRC 512 exempts most forms of investment income generated by an IRA from taxation. Some examples of exempt types of income include interest from loans, dividends, annuities, royalties, most rentals from real estate, and gains/losses from the sale of real estate.

However, a tax known as the unrelated business taxable income (UBTI) tax can, in limited circumstances, trigger up to a 37% income tax on an IRA in the following limited investment scenarios:

- Income from the operations of an active trade or business – i.e. a restaurant, gas station, store, etc.

- Business income generated via a passthrough entity, such as an LLC or partnership.

- Using a nonrecourse loan to purchase a property (in the case of an IRA)

- Using margin on a stock purchase

In the case of an accredited investor or qualified purchaser making a Self-Directed IRA investment into an investment fund, if the fund will be using leverage or investing in businesses operating via a passthrough entity, such as an LLC, the income from the fund could be subject to the UBTI tax when allocated to the IRA investor.

The IRA Financial Qualified Purchaser/Accredited Investor Difference

IRA Financial “literally” wrote the book on the Self-Directed IRA. Our founder, Adam Bergman, Esq, has written 8 books on self-directed retirement plans and over the last 15+ years has helped over 24,000 clients invest over $3.2 billion in alternative assets.

IRA Financial is one of the only Self-Directed IRA providers that can help a qualified purchaser or accredited investor navigate the UBTI rules and customize the investment in the most tax efficient manner, whether it involves using a C Corporation blocker, foreign blocker corporation, re-structuring the investment, or applying various tax optimization strategies, IRA Financial is the leading provider for sophisticated qualified purchaser or accredited investors seeking to make a Self-Directed IRA investment.

Why Self-Directed IRA Fees Really Matter

Self-Directed IRA custodian fees matter and could cost you tens of thousands of dollars for your retirement by making the wrong custodian choice for your Self-Directed IRA.

Do you really know how much Self-Directed IRA fees you are paying? If you don’t know off the top of your head, you’re not alone. There are numerous Self-Directed IRA providers, but many people still do not know the fees they pay annually to Self-Directed their retirement. Many don’t even realize that the Self-Directed IRA custodian is charging them an annual fee based on the value of their IRA. It is certain that if more Self-Directed IRA investors did not find the task of figuring it out confusing and difficult, more Self-Directed IRA investors would be turning to flat annual IRA custodian fee options. Numbers don’t lie. A customer with $200,000 that grows to $400,000 over a ten-year period would pay an extra $5000 or so of IRA fees versus choosing a flat fee option with a Self-Directed IRA custodian, such as IRA Financial. That's close to $5000, or 1.60% of a customer’s average IRA assets of $300,000 cumulatively over the 10 years that they chose to Self-Directed. This is exactly why it is so important to understand your Self-Directed IRA custodian fees, as overpaying for Self-Directed IRA custodian fees will impact your retirement savings.

What is a Self-Directed IRA Custodian?

Pursuant to Section 408 of the Internal Revenue Code, an IRA must be established by a bank, financial institution, or authorized trust company. Thus, a bank such as Wells Fargo, financial instruction such as Vanguard, or a trust company such as the IRA Financial Trust Company are authorized to establish and administer IRAs. The main difference is that not all IRA custodians allow the IRA to invest in alternative assets, such as real estate.

The majority of all Self-Directed IRA custodians are non-bank trust companies for the reasons outlined above. The Self-Directed IRA custodian, or trust company, will typically have a banking relationship with a bank that will hold the IRA funds in a special account called an omnibus account, offering each Self-Directed IRA client FDIC protection of IRA funds up to $250,000 held in the account. For example, IRA Financial Trust is a non-banking IRA custodian. IRA Financial Trust has partnered with Capital One Bank, one of the largest banks in the country, to offer our Self-Directed IRA clients with a safe and secure way to make Self-Directed IRA investments.

What Does a Self-Directed IRA Custodian Do?

In general, a Self-Directed IRA custodian is responsible for complying with IRS rules for the administration and recordkeeping of your Self-Directed IRA. The two main functions of a Self-Directed IRA are filing IRS Form 5498 and IRS Form 1099-R. IRS Form 5498 is filed annually with the IRS and provides the IRS with an overview of the Self-Directed IRA account value and general investment history. Whereas, IRS Form 1099-R gives the IRS information as to any contributions, transfers, rollovers, or distributions involving the Self-Directed IRA

The following are the primary roles and responsibilities of a Self-Directed IRA custodian:

-

- Permitted to hold and custody IRA and 401(k) plan assets

-

- Subject to state regulation by the state division of banking

-

- Performance of administrative record-keeping regarding the Self-Directed IRA

-

- Perform administrative review of the Self-Directed IRA assets

-

- Assisting in opening & funding your IRA account

-

- Making the investment(s) on your behalf

-

- Making distributions & paying expenses per your request

-

- Providing you with quarterly statements

-

- Answering questions about your account and our procedures

-

- Reporting information required by the IRS and other governmental agencies

-

- IRS Form 1099R - Distributions from your IRA

-

- IRS Form 5498 - Contributions to, and Fair Market Value of, your IRA

A Self-Directed IRA custodian is not permitted to offer any investment advice or sell investment products. Hence, establishing a Self-Directed with a custodian who will charge your IRA fees based on the annual value of the IRA is illogical. The entire purpose behind a Self-Directed IRA is that the owner gets to “self-direct” his or her IRA investments. With a Self-Directed IRA, the IRA owner has total control and freedom to make investment decisions on behalf of the IRA. Hence, all IRA gains or losses solely reflect the investment decisions of the IRA owner. A Self-Directed IRA custodian that imposes annual asset valuation fees on their IRA customers for no value-added investment services is irrational.

Additionally, imposing annual asset value fees on Self-Directed IRAs creates a conflict of interest between the IRA custodian and the Self-Directed IRA custodian. Each year the Self-Directed IRA customer must provide the custodian with the annual value of their IRA. The value is then reported by the IRA custodian to the IRS on Form 5498. The value is used for the imposition of required minimum distributions for pre-tax IRA owners over the age of 73. That amount of tax paid by an IRA owner subject to the required minimum distribution rules is wholly dependent on the values provided to the IRA custodian. However, if the Self-Directed IRA customer is concerned about IRA custodian fees, he or she may deflate the value of their IRA to keep their annual IRA custodian fees as low as possible. This puts the Self-Directed IRA customer in a difficult position to juggle their responsibility to provide an accurate annual IRA value for IRS purposes while simultaneously attempting to keep their Self-Directed custodian fees as low as possible.

Understanding Self-Directed IRA Custodian Fees

Over the last several years, the fees involved in establishing and maintaining a Self-Directed IRA account have become more cost-efficient and client-friendly. Depending on the IRA custodian you choose and the type of Self-Directed IRA you establish, custodian controlled vs. checkbook IRA, the type of Self-Directed IRA fees imposed could differ. Irrespective of whether you elect to use a Self-Directed IRA or a Self-Directed IRA LLC, the basic premise of a Self-Directed IRA account is that the IRA owner has total investment control and authority over their IRA. That is where the name “Self-Directed” comes from. Hence, imposing an asset valuation fee on a Self-Directed IRA account does not seem right or fair. For example, if you open a Self-Directed IRA and buy property A for $100,000 and a year later the property’s value went up to $200,000. Why should the Self-Directed IRA custodian charge higher Self-Directed IRA annual custodian fees just because you made a smart investment? A Self-Directed IRA custodian is known as a passive custodian. A Self-Directed IRA custodian is not permitted under law to offer investment advice or promote investments. Hence, why would anyone choose a Self-Directed IRA custodian that charges asset valuation fees? Here is another real example. An individual purchased Bitcoin in 2015 and did not know she chose a custodian that was charging a 1% fee on the value of the Self-Directed IRA as of December 31. Her initial annual Self-Directed IRA custodian fee would be fair. However, by the time Bitcoin hit $40,000 some years later, she was forced to pay thousands of dollars of annual Self-Directed IRA custodian fees to a custodian who added no value. Paying asset value fees to an investment advisor who is providing investment advice and services makes total sense. However, paying asset value fees to a Self-Directed IRA custodian that is offering no investment advice or adding any investment value, makes no sense. The core reason so many Self-Directed IRA investors end up establishing IRA accounts with custodians that charge an annual asset valuation fee is they are either unaware or fail to understand the long-term impact the choice can have on their retirement.

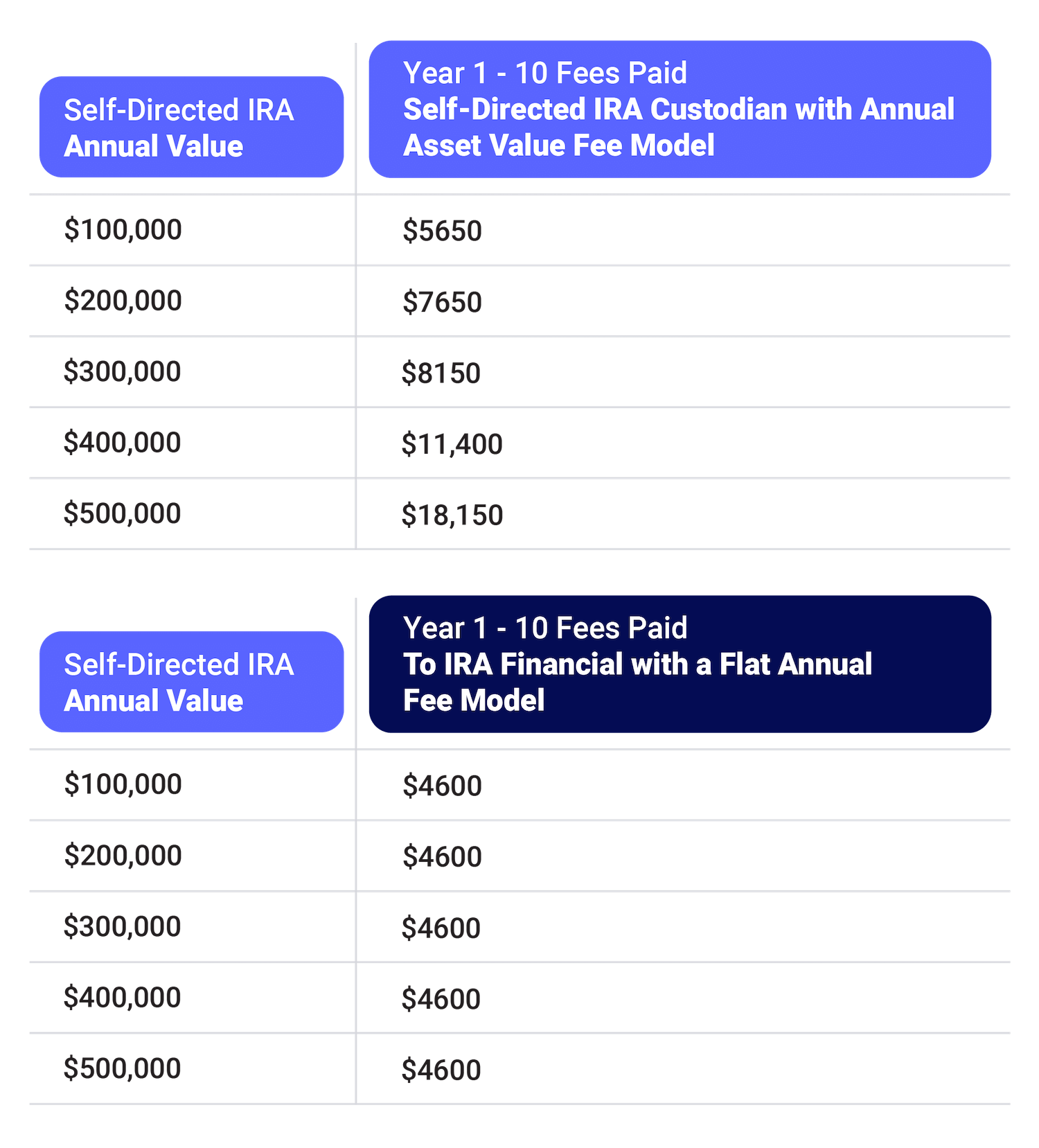

Below is a table that illustrates the significant long-term financial damage done to a retirement account by choosing the wrong Self-Directed IRA custodian. The table shows the difference between choosing to work with IRA Financial, which has flat annual Self-Directed IRA custodian fees, versus a Self-Directed IRA custodian that charges fees based on the annual value of the Self-Directed IRA. The Self-Directed IRA annual value figures are based on the average fees charged by several Self-Directed IRA custodians.

A client with $500k in assets would save nearly $14,000 over ten years.

The above-referenced table is a conservative estimate of the total fees a Self-Directed IRA investor would pay to a custodian that charges annual asset valuation fees. The reason for this is that the table assumes that the customer would maintain the same Self-Directed IRA value over ten years. Consider that if a customer Self-Directed IRA’s assets grew from $200,000 to $400,000 over ten years, the Self-Directed IRA custodian would pay an extra $4,925 cumulatively versus. what they would pay to IRA Financial with a flat annual Self-Directed IRA fee model. That's $4,925, or 1.64% of their average assets of $300,000 cumulatively over the 10 years.

Conclusion

There is categorically no good reason to establish a Self-Directed IRA with a custodian who will charge your IRA fees based on the value each year. It makes no sense. Why on god’s green earth would you pay fees to a third party for your smart investment decisions and success? It’s not like the Self-Directed IRA custodian is providing you with any investment advice. The Self-Directed IRA custodian is not even permitted by law to offer any investment or financial advice. The good news is that you have other fee options for your Self-Directed IRA. You can always transfer your IRA tax-free to IRA Financial or any other Self-Directed IRA custodian that charges a flat annual fee. Electing to establish a Self-Directed IRA at a custodian that imposes annual asset valuation fees on your IRA is a mistake that will have a long-term impact on you and your family’s financial future.

The Self-Directed IRA Trust

Over the years there has been interest by Self-Directed IRA investors to gain checkbook control without the cost of using an LLC. Most states charge moderate LLC filing fees and annual fees, and some states, like California, impose a high annual franchise fee on all CA LLCs ($800). For this reason, some CA residents have looked for an alternative to using an LLC to gain checkbook control. For some states, like FL, which do not have any state income tax, using a trust can be an alternative to using an LLC for a Self-Directed IRA, however, the investor would not be able to avail themselves of any limited liability protection, which is important for many real estate investors. Plus, almost all states, even those that do not have a state income tax, require trusts to file a state tax return, on top of the IRS Form 1041.

- For most Self-Directed IRA, an LLC is better than a trust

- LLCs offer protection for your investments

- Trusts have annual filing requirements

Over ten years ago, IRA Financial was one of the first Self-Directed IRA providers to offer clients the ability to use a trust instead of an LLC for checkbook control IRA investments. However, there are a number of important reasons why an LLC makes far more sense in the Self-Directed IRA context than a trust.

Before I get into the advantages and disadvantages of using a trust versus an LLC with a Self-Directed IRA, it is important to understand some basic trust terms.

What is a Self-Directed Trust?

A trust is a legal vehicle that allows a third party, a trustee, to hold and direct assets in a trust fund on behalf of a beneficiary. You need three parties to legally have a trust:

- Grantor

- Trustee

- Beneficiary

The trust is not filed with the state but is simply an agreement between three parties

Can an IRA be a Grantor of a Trust?

It appears that an IRA can be a grantor of a trust. The grantor is the party contributing the asset to the trust. The trustee is the party that manages the trust’s assets, and the beneficiary is the party that receives the income or assets of the trust.

In the case of a Self-Directed IRA, the IRA trust company, the custodian for the benefit of the IRA, will be the grantor and beneficiary of the trust and the IRA owner will be the trustee. The trust agreement would details the terms of the trust and its rules.

Type of Grantor Trusts

Trusts can generally be revocable or non-revocable. In the case of a Self-Directed IRA, the trust would be revocable.

Federal Tax Treatment

A grantor trust is taxed similarly to a single-member LLC and there would be no federal income tax liability, except that it still has a federal income tax filing requirement – Form 1041. The income or assets of the trusts are reported by the grantor, in this case, the IRA, which is a tax-exempt party. However, unlike a single-member LLC, where no federal income tax return is required to be filed, for a grantor trust, IRS Form 1041 must be filed on an annual basis. The IRS Form 1041 does not have to be completed in full, but it must be partly completed and submitted to the IRS annually.

State Tax Treatments

Depending on the state where the trust is formed, trustee resides, or where trust assets are located, the state may impose state taxation on the trust, plus require a trust return. The complexities involved in the state tax treatment of trusts is one of the main reasons why using a trust for self-directed IRA purposes is unpopular. For example, California will impose state tax and require the trust to file a state return if the trustee resides in California or if the trust as California source income. The same goes for the state of New York. Some states, like Florida that do not have a state tax regime, will not impose any state tax or filing on a Florida trust, but the trust will still have a federal tax filing requirement under IRS Form 1041.

The difficulty with the state taxation of trusts is that every state is different, and every state has different trust rules and taxation principles. Whereas, the state rules surrounding LLCs are far more uniform and consistent. It is for this reason that LLCs are seemingly a better option than trusts for most self-directed IRA investors.

Advantages of using a Trust vs a Self-Directed IRA LLC

The main advantage of using a trust versus an LLC for a Self-Directed IRA investor is the ability to gain checkbook control without having to incur costs for state LLC establishment. A trust is not a legal entity formed under state law and can be created by simply having an agreement between three parties: a grantor, trustee, and beneficiary. In addition, the trust can have its own EIN and can use a bank account managed by the trustee to make self-directed IRA investments. However, the majority of states have moderate LLC filing and annual fees, and most are under $150. Furthermore, the state with the highest LLC annual fees, California, will also impose similar fees and filing obligations on California state trusts.

Disadvantages of using a Trust vs an LLC

The two primary disadvantages of using a trust versus an LLC for a Self-Directed IRA investor are (i) loss of limited liability protection, and (ii) annual tax filing obligations.

The advantage of using an LLC to make investments is that the LLC protects all assets outside of the LLC from creditor attack. Hence, a creditor of an IRA LLC can only attack the IRA assets in the LLC and not any of the IRA owner’s other IRA assets. Whereas, a trust does not offer any limited liability protection, although it does offer better privacy since it is quite difficult to identify the grantor or beneficiaries of a trust since the trust agreement is not filed with any state authority.

Because each state generally has its own trust rules and tax regime, using a trust puts a lot of administrative responsibility on the trustee of the trust, the IRA owner, to make sure the trust is satisfying all state trust reporting and filing requirements.

Conclusion

In general, an IRA can be the grantor of a trust and a trust can technically be used as a vehicle for a Self-Directed IRA investor to gain checkbook control. However, the federal and state trust tax rules and requirements and the lack of limited liability protection make the LLC the smarter choice for most Self-Directed IRA investors.

For more information, please contact one of our IRA experts @ 800.472.0646.