Solo 401(k) Asset & Credit Protection Benefits

Retirement accounts have become many Americans' most valuable assets. That means it is vital that you have the ability to protect them from creditors, such as people who have won lawsuits against you. In general, the asset/creditor protection strategies available to you depend on the type of retirement account you have (i.e. Traditional IRA, Roth IRA, or 401(k) qualified plan, etc.), your state residency, and whether the assets are yours or have been inherited. Solo 401(k) Asset and Creditor Protection, also known as Solo 401(k) Bankruptcy Protection, can help protect your assets in your 401(k).

Federal Protection for 401(k) Qualified Plans for Bankruptcy

Effective for bankruptcies filed after October 17, 2005, the following rules give protection to a debtor’s retirement funds in bankruptcy by way of exempting them from the bankruptcy estate. The general exemption found in section 522 of the Bankruptcy Code, 11 U.S.C. §522, provides an unlimited exemption for retirement assets exempt from taxation for Section 401(a) (tax qualified retirement plans—pensions, profit-sharing and section 401(k) plans). Thus, ERISA qualified plans as well as Solo 401(k) plans are afforded full bankruptcy exemption. What this means is that if a participant of a 401(k) Plan declares bankruptcy, his or her 401(k) plan assets will be exempt from the bankruptcy proceeding and could not be attached by the bankruptcy’s estates creditors.

Federal Protection for 401(k) Plan Qualified Plan Funds Outside of Bankruptcy

In the case of a debtor who is not under the jurisdiction of the federal bankruptcy court but rather has become involved in a state law insolvency, enforcement, or garnishment proceeding, the 2005 Bankruptcy Act is inapplicable and the ERISA rules and state laws would govern.

Title I of ERISA requires that a pension plan provide that benefits under the plan may not be assigned or alienated; i.e., the plan must provide a contractual “anti‑alienation” clause. For the anti-alienation clause to be effective, the underlying plan must constitute a “pension plan” under ERISA. Such a plan is any “plan, fund or program which...provides retirement income to employees.” ERISA §3(2)(A).. Therefore, a plan that does not benefit any common-law employee is not an ERISA pension plan. As a result, a Solo 401(k) Plan is not treated as an ERISA Plan.

In addition to the ERISA protection, the Internal Revenue Code Section 401(a)(13(A) provides that “[a] trust shall not constitute a qualified trust under this section unless the plan of which such trust is a part provides that benefits provided under the plan may not be assigned or alienated. Thus, a retirement plan will not attain qualified status unless it precludes both voluntary and involuntary assignments.

Note - neither ERISA nor Code protections apply to assets held under individual retirement arrangements, simplified employee pension plans, government plans, or most church plans.

Furthermore, ERISA section 514(a) provides that ERISA supersedes state laws insofar as such laws relate to employee benefit plans. The ERISA anti-alienation and preemption provisions combine to make state attachment and garnishment laws inapplicable to an individual’s benefits under an ERISA-covered employee benefit plan.

Exceptions

There are a number of exceptions to ERISA’s and the Code’s anti‑alienation provisions:

- Qualified domestic relations orders (“QDROs”), as defined in Internal Revenue Code Section 414(p), may be exempted (Internal Revenue Code §401(a)(13)(B); ERISA §206(d)(3)). This means that retirement plan assets are a marital asset subject to division in divorce and attachment for child support.

- Up to 10 percent of any benefit in pay status may be voluntarily and revocable assigned or alienated (Internal Revenue Code §401(a)(13)(A); Treas. Reg. §1.401(a)-13(d)(1); ERISA §206(d)(2)).

- A participant may direct the plan to pay a benefit to a third party if the direction is revocable and the third party files acknowledgment of lack of enforceability (Treas. Reg. §1.401(a)-13(e)).

- Federal tax levies and judgments are exempted. The Treasury Regulations under Code section 401(a)(13) provide that plan benefits are subject to attachment by the IRS in common law and community property states.

In addition to the statutory exceptions noted above, several court decisions have held that an individual’s retirement plan benefits may be subject to attachment for federal criminal penalties or restitution arising from a crime

Solo 401(k) Plans

A debtor’s plan benefits under a pension, profit-sharing, or section 401(k) plan are generally safe from creditor claims both inside and outside of bankruptcy due to ERISA and the Code’s broad anti-alienation protections. However, case law and Department of Labor Regulations have held that such a plan that benefits only an owner (and/or an owner’s spouse) are not ERISA plans, thus voiding the anti-alienation protections generally afforded to ERISA plans. Thus, state law will govern the protection afforded to Solo 401(k) Plans outside the bankruptcy context.

State Law Protection of Solo 401(k) Plan Assets Outside of Bankruptcy

Because case law and Department of Labor Regulations have held that such a plan that benefits only an owner (and/or an owner’s spouse) are not ERISA plans, thus voiding the anti-alienation protections generally afforded to ERISA plans, state law will govern the protection afforded to Solo 401(k) Plans outside the bankruptcy context.

The following table will provide a summary of state protection afforded to Solo 401(k) Plans from creditors outside of the bankruptcy context.

| State | State Statute | Special Statutory Provision | State Solo 401(k) Plan Exemption from Creditors |

| Alabama | Ala. Code §19-3B-508 | Yes | |

| Alaska | Alaska Stat. §09.38.017 | The exemption does not apply to amounts contributed within 120 days before the debtor files for bankruptcy. | Yes |

| Arizona | Ariz. Rev. Stat. Ann. § 33-1126C | The exemption does not apply to amounts contributed within 120 days before a debtor files for bankruptcy. | Yes |

| Arkansas | Ark. Code Ann. §16-66-220 | Yes16-66-220. Pension and profit-sharing plans.(a)(1) A person's right to the assets held in or to receive payments, whether vested or not, under a pension, profit-sharing, or similar plan or contract, including a retirement plan for self-employed individuals, or under an individual retirement account or an individual retirement annuity, including a simplified employee pension plan, is exempt from attachment, execution, and seizure for the satisfaction of debts unless the plan, contract, or account does not qualify under the applicable provisions of the Internal Revenue Code of 1986. (2) A person's right to the assets held in or to receive payments, whether vested or not, under a government or church plan or contract is also exempt unless the plan or contract does not qualify under the definition of a government or church plan under the applicable provisions of the federal Employee Retirement Income Security Act of 1974. [FN1] (b)(1) Contributions to an individual retirement account that exceed the amounts deductible under the applicable provisions of the Internal Revenue Code of 1986 and any accrued earnings on such contributions are not exempt under this section unless otherwise exempt by law. (2) However, the limitations of subdivision (b)(1) of this section do not apply to an individual retirement account established pursuant to and qualifying under § 408(A) of the Internal Revenue Code. | |

| California | Cal. Civ. Proc. Code § 704.115 | YesBut only to the extent necessary to provide for the support of the judgment debtor when the judgment debtor retires and for the support of the spouse and dependents of the judgment debtor, taking into account all resources that are likely to be available for the support of the judgement debtor when the judgment debtor retires. | |

| Colorado | Colo. Rev. Stat. §13-54-102 | Yes | |

| Connecticut | Conn. Gen. Stat. §52-321a | Yes | |

| Delaware | Del Code Ann. § 10-4915 | Yes | |

| D.C. | D.C. Code § 15-501(a)(9) & (10) | Yes | |

| Florida | Fla. Stat. Ann. §222.21 | Yes | |

| Georgia | Georgia Code Ann. § 44-13-100(a)(2.1) | Yes | |

| Hawaii | Hawaii Rev. Stat. § 651-124 | The exemption does not apply to contributions made to a plan or arrangement within three years before the date a civil action is initiated against the debtor. | Yes |

| Idaho | Idaho Code §§ 11-604A, 55-1011 | Yes | |

| Illinois | I.L.C.S. § 5/12-1006 | Yes | |

| Indiana | Ind. Code Ann. § 55-10-2(c)(6) | Yes | |

| Iowa | Iowa Code Ann. § 627.6(8)(e), (f) | YesShould apply to Solo 401(k) – statute referenced in case. | |

| Kansas | Kan. Stat. Ann. § 60-2308 | Yes | |

| Kentucky | Ky. Rev. Stat. Ann. § 427.150(2)(f) | The exemption does not apply to any amounts contributed to an individual retirement account if the contribution occurred within 120 days before the debtor filed for bankruptcy. The exemption also does not apply to the right or interest of a person in individual retirement account to the extent that right or interest is subject to a court order for payment of maintenance or child support. | Yes |

| Louisiana | La. Rev. Stat. Ann. §§ 20:33(1), 13:3881(D) | Yes | |

| Maine | Me. Rev. Stat. Ann. Tit. 14, § 4422(13)(E) | Exempt only to the extent reasonably necessary for the support of the debtor and any dependent. | Yes |

| Maryland | Md. Code Ann. Cts. & Jud. Proc. § 11-504(h)(1) | Yes | |

| Massachusetts | Mass. Gen. L. Ch. 235 § 34A; 236 § 28 | The exemption does not apply to an order of court concerning divorce, separate maintenance or child support, or an order of court requiring an individual convicted of a crime to satisfy a monetary penalty or to make restitution, or sums deposited in a plan in excess of 7% of the total income of the individual within 5years of the individual's declaration of bankruptcy or entry of judgment. | Yes |

| Michigan | Mich. Comp. Laws Ann. §§ 600.5451(1), 600.6023(1)(k) | The exemption does not apply to amounts contributed to an individual retirement account or individual retirement annuity if the contribution occurs within 120 days before the debtor files for bankruptcy. The exemption also does not apply to an order of the domestic relations court. | No |

| Minnesota | Minn. Rev. Stat. Ann. § 550.37(24) | Protection limited to $60,000 (adjusts for inflation). | Yes |

| Mississippi | Miss. Code Ann. § 85-3-1(e)Applies to solo 401(k) plans | Yes | |

| Missouri | 513.430 | Exemption limited to extent reasonably necessary for support. | Yes |

| Montana | Mont. Code Ann. §§ 19-2-1004, 25-13-608, 31-2-106 | Yes | |

| Nebraska | Neb. Rev. Stat. § 25-1563.01Should apply to Solo 401(k) Plans unless plan established within two years of action | Yes, unless plan established within two years of action. | |

| Nevada | Nev. Rev. Stat. § 21.090(1)(q) | The exemption is limited to $500,000 in present value held in an IRA or Solo 401(k) Plan. | Yes |

| New Hampshire | N.H. Code Ann. § 511:2, XIX | Yes | |

| New Jersey | N.J. Stat. Ann. § 25:2-1(b) | Yes | |

| New Mexico | N.M. Stat. Ann. §§ 42-10-1, 42-10-2 | Yes | |

| New York | N.Y. Civ. Prac. L. and R. § 5205(c) | Yes | |

| North Carolina | N.C. Gen. Stat. § 1C-1601(a)(9) | Yes | |

| North Dakota | N.D. Cent. Code § 28-22-03.1(3) | Retirement funds that have been in effect for at least one year, to the extent those funds are in a fund or account that is exempt from taxation under section 401, 403, 408, 408A, 414, 457, or 501(a) of the Internal Revenue Code of 1986. The value of those assets exempted may not exceed one hundred thousand dollars for any one account or two hundred thousand dollars in aggregate for all account. | Yes |

| Ohio | Ohio Rev. Code Ann. § 2329.66(A)(10)(b) and (c) | Questionable.The statute seems to exclude pension and other similar plans, but does seemingly carve out profit sharing plans for the exclusion. | |

| Oklahoma | 31 Okla. St. Ann. § 1(A)(20) | Yes | |

| Oregon | 2017 ORS 18.345 | Yes | |

| Pennsylvania | 42 Pa. C.S. §§ 8124(b)(1)(vii), (viii), (ix) | 100%, except for amounts (1) contributed within 1 year (not including rollovers), (2) contributed in excess of $15,000 in a one-year period, or (3) deemed to be fraudulent conveyances. | Yes |

| Rhode Island | R.I. Gen. Laws § 9-26-4(11), (12) | No protection for non-ERISA qualified plans. | No |

| South Carolina | S.C. Code Ann. § 15-41-30(12) | IRA exemption limited to the extent reasonably necessary for support. For Solo 401(k) Plans, not limited to the extent reasonable necessary for support. | Yes |

| South Dakota | S.D. Cod. Laws §§ 43-45-16S.D. Cod. Laws §§ 43-45-17 | Exempts “certain retirement benefits” up to $1,000,000. | Yes |

| Tennessee | Tenn. Code Ann. § 26-2-105 | Distributions 100% exempt to the extent they are on account of age, death, or length of service and debtor has no right or option to receive other than periodic payments at or after age 58. | Yes |

| Texas | Tex. Prop. Code § 42.0021 | Yes | |

| Utah | Utah Code Ann. § 78-23-5(1)(a)(xiv) | The exemption does not apply to amounts contributed or benefits accrued by or on behalf of a debtor within one year before the debtor files for bankruptcy. | Yes |

| Vermont | 12 Vt. Stat. Ann. § 2740(16) | Yes | |

| Virginia | Va. Code Ann. § 34-34 | Limited to interest in one or more plans sufficient to produce annual benefit of up to $25,000 (pursuant to actuarial table in statute). | Yes |

| Washington | Wash. Rev. Code § 6.15.020 | Yes | |

| West Virginia | §38-10-4 | Principal 100% protected. Exemption for distributions limited to the extent reasonably necessary for support. | Yes |

| Wisconsin | Wisc. Stat. Ann. § 815.18(3) | Applies to solo 401(k) plans but limited to the extent reasonably necessary for the support of the debtor and the debtor’s dependents. | Yes |

| Wyoming | Wy. Stat. Ann § 1-20-110(a)(i), (ii). No statutory exemption for IRAs. – only mentions retirement plans | No statutory exemption for IRAs. – only mentions retirement plans. | Yes |

Asset Protection Planning

The different federal and state creditor protection afforded to 401(k) qualified plans and IRS inside or outside the bankruptcy context presents a number of important asset protection planning opportunities.

If, for example, you have left an employer where you had a qualified plan, rolling over assets from a qualified plan, like a 401(k), into an IRA may have asset protection implications. For example, if you live in or are moving to a state where IRAs are not protected from creditors or have in excess of $1million dollars in plan assets and are contemplating bankruptcy, you would likely be better off leaving the assets in the company qualified plan.

Note - If you plan to leave at least some of your IRA to your family, other than your spouse, the assets may not be protected from your beneficiaries’ creditors, depending on where the beneficiaries live. IRA assets left to a spouse would likely receive creditor protection if the IRA is re-titled in the name of the spouse. However, you will likely be able to protect your IRA assets that you plan on leaving to your family, other than your spouse, by leaving an I.R.A. to a trust. To do that, you must name the trust on the IRA custodian Designation of Beneficiary Form on file.

The Solo 401(k) Asset & Creditor Protection Solution

By having and maintaining a Solo 401(k) Plan, the people to whom you owe money - as a result of normal debt, bankruptcy or a civil court judgment – will likely not be able to reach your Solo 401(k) assets to satisfy the debt. However, Solo 401(k) Plan assets are not federally protected from divorce settlements or federal tax liens. As illustrated above, most states will afford Solo 401(k) Plans full protection from creditors outside of the bankruptcy context.

Airbnb in Your IRA - Will it Trigger UBTI?

As you are probably aware by now, you can use retirement funds to invest in real estate. Of course, you must adhere to all the IRS rules, especially UBTI, when doing so. A lot depends on the type of property you own, how you earn income from it, and what type of plan you are investing with. Holding an Airbnb in your IRA has become more popular. Many investors are looking into short-term rental options, as opposed to annual commitments. Both types of investments offer the investor many advantages.

Investing in Real Estate with an IRA

Real estate has always been the most popular alternative asset for self-directed retirement account investors. These types of accounts, such as the Self-Directed IRA and Solo 401(k) plan, allow one to use retirement funds however you see fit. By self-directing, you are control of your investment decisions and not limited to what a bank or other financial institution offers. So long as you don't run afoul of the IRS rules, you have greater flexibility than just investing in the usual stocks, bonds and mutual funds.

Why is Real Estate so Popular?

For one, everyone needs a place to live, work and even build on. Plus, there's only so much land to develop on this great planet. Eventually, the demand will far outweigh the supply, making it a great investment. Real estate, and other alternatives, also provide diversity in your retirement holdings. As the saying goes, don't put all your eggs in one basket. Investing everything in the stock market is not the smartest decision you can make. On the other hand, neither is putting all of your retirement funds into one real estate property.

Of course, real estate is not without its risks. Everyone remembers the housing crash just over a decade ago. However, smart investors didn't panic. Instead, they started buying up even more properties at a much better price. They new that real estate would bounce back and it quickly did.

There's also a myriad of real estate investment options, whether it be commercial or residential. For those looking for a steady stream of income, a rental, even a short-term rental like Airbnb, is very popular. Some might look into fix and flips, while others will buy and hold. Investing in raw land for future development may suit other investors.

Lastly, real estate is a hard asset, unlike stocks, which are considered "paper" assets. It's great for one's mindset that you can physically see and touch an investment. You also have the power to improve your property personally. Upgrading the appliances will help you receive more rent in an income property. Landscaping will raise the asking price of your flip house. Sweat equity is something real estate investors know all about.

Holding an Airbnb in Your IRA

Airbnb, along with other platforms like VRBO, have become increasingly popular across the globe. The next logical step is to look at these properties as retirement assets. Weekly and/or monthly rentals have the potential to bring in more income than an annual renter. The downside is that you need to keep the space occupied most of the time to keep the money coming in. Of course, there may be more expenses, as the rental needs to be cleaned after each stay. Having a full-time might be a better option for many people. However, an Airbnb property can pay huge dividends.

This is especially true if you are in a desired area. Live close to the beach? Maybe you are near a theme park or arena. Perhaps, you are on the outskirts of a major city, where you can charge a little more per stay. As mentioned earlier, you need to stay within the IRS rules.

The first rules, especially when real estate is involved, are the prohibited transaction rules. Specifically, it's important to note the disqualified persons facet of the Internal Revenue Code (IRC). Essentially, any investment (including an Airbnb property) cannot involve a disqualified person. Your Self-Directed IRA is the only thing that can benefit from the investment held within. Disqualified people include yourself (the IRA owner), your spouse, your lineal ascendants and descendants and entities controlled by such persons.

A disqualified person cannot benefit from an IRA-owned asset, including real estate. This means one cannot utilize the Airbnb property, nor can they earn a salary doing work for such property. Some examples:

- You cannot personally live in a property your IRA owns.

- You're not allowed to rent it out to your father, daughter or their spouses.

- You can't hire your son-in-law to manage the property.

What About UBTI?

Unrelated Business Taxable Income, or UBTI, is a tax imposed on certain investments made with retirement funds, which includes real estate. This tax, which can go as high as 37%, can make an investment tax-inefficient. In regards to real estate, the UBTI can apply in different scenarios. The first one, is when you borrow money to purchase a property. Also, if your real estate investments go far enough to make it a business, you might get hit with the tax. There is one other situation where the UBTI comes into play when holding an Airbnb in your IRA.

The IRS does not offer much guidance on the use of Self-Directed IRAs and short-term rentals, such as Airbnb, especially with respect to the UBTI rules.

Payments for the use or occupancy of rooms and other space that render services to the occupant don’t constitute rent from real property.

Rent from Real Property:

- The use or occupancy of rooms in hotels, boarding houses, or apartment houses furnishing hotel services,

- Tourist camps or tourist homes

- Motor courts or motels,

- Occupancy of space in parking lots, warehouses, or storage garages

Generally, services are considered rendered to the occupant if they are primarily for his/her convenience. Supplying maid service is an example of this kind of service. However, furnishing of heat and light, cleaning public entrances, exits, stairway and lobbies, etc. are not.

Therefore, it may appear that as long as you do not provide daily maid services or other convenience features like a daily breakfast, the investment should not be treated as a hotel or motel type of income stream. As a result, it may generate rental income that’s exempt from the UBTI tax rules.

Internal Revenue Code 469

An argument can be made that under IRC 469 – the rental income can be deemed active and not a passive investment if the average rental activity is less than seven days. Although, IRC 469 applies to the ability to take deductions under the passive activity loss rules, an argument can potentially be made that if under 469 the activity is deemed active, it could be subject to the UBTI tax

However, on the flip side, Schedule E, which is only required to be filed if the activity is passive and not active (Schedule C), does not have a day threshold as well and only focuses on level of ancillary activity. Hence, when doing short-term rentals with your Self-Directed IRA, it is important to be mindful of the potential application of the IRC 469 rules and the seven day threshold. Unfortunately, there is no direct guidance from the IRS under IRC 512 on short-term rentals.

As always, be sure to speak with a UBTI expert before engaging in such investments. Remember, the IRA Financial blog is for educational purposes, and you should always consult with a financial advisor before making any investment.

Should You Hold an Airbnb in Your IRA? - Conclusion

Of course, this can only be answered by each individual investor and their financial goals. Real estate will always be a popular investment. Short-term rentals, like Airbnb, are here to stay. Those with a prime location, can earn some serious income for their retirement plan. Of course, you have to be wary of the IRS rules to make sure the tax benefits of the IRA are not compromised.

If you have any questions about an Airbnb in your IRA, or about the UBTI rules, feel free to give us a call at 800.472.0646 today!

Flipping a Home in a Self-Directed IRA – A Case Study

Flipping homes in a Self-Directed IRA has quickly become one of the most popular investment concepts. The primary advantage of signing a retirement account, such as an IRA or 401(k), to buy and sell real estate is that all the income and gains from the real estate flipping transaction will go back to the IRA tax-free.

This article will use a case study to explore how one can use their retirement funds to generate tax-free gains from a real estate flipping transaction.

Facts

Jen is 47 years old and has been looking to get involved in the passive real estate investing space. Jen has an IRA of $175,000 at a traditional financial institution. Jen is also in the process of leaving her current employer for a new job. She has $125,000 in her former employer's 401(k) plan. Jen lives in the Dallas area and has been noticing several homes for sale in her neighborhood. After generating some solid returns in the stock market over the last several years, Jen is looking to gain some added diversification by gaining more exposure to real estate.

After spending some time online, Jen found a home in her neighborhood that she thought was priced right. Jen believed that if she put some money into landscaping and did some other internal improvements, she could flip the home at a higher price. Jen had some personal savings, but most of her savings were tied up in her retirement account. After doing some online searches Jen quickly discovered that she could set up a Self-Directed IRA and use her retirement funds to purchase the home tax-free. Best of all, the gains from the real estate flip would go back to the Self-Directed IRA without tax.

What is a Self-Directed IRA?

A Self-Directed IRA is essentially an IRA that allows for alternative asset investments, such as real estate or even cryptocurrency. Traditional financial institutions do not allow IRAs to invest in IRS approved alternative assets, such as real estate, because their focus is on earning fees through traditional investments.

When it comes to making investments with a Self-Directed IRA, the IRS generally does not tell you what you can invest in, only what you cannot invest in. The types of investments that are not permitted to be made using retirement funds is outlined in Internal Revenue Code Section 408 and 4975. These rules are generally known as the “Prohibited Transaction” rules. Other than life insurance, collectibles, and transactions that involve or directly or indirectly benefit the IRA holder or a “disqualified person,” one can use their IRA to make the investments. A “disqualified person” is generally defined as the IRA holder and any of his or her lineal descendants and/or any entities controlled by such persons.

Hence, so long as the real estate investment does not directly or indirectly benefit a “disqualified person,” it is a permissible Self-Directed IRA investment.

The IRS has always permitted real estate to be held inside IRA retirement accounts. Investments with a Real Estate IRA are fully permissible under the Employee Retirement Income Security Act of 1974 (ERISA). Real estate is one of the most popular Self-Directed IRA investments. IRS rules permit you to engage in almost any type of real estate investment, aside generally from any investment involving a disqualified person.”

Why Should Jen Flip Real Estate Using a Self-Directed IRA?

The concept of tax deferral is based on the principle that income and gains generated within a pretax retirement account are not taxed in the year they are earned. Instead, taxes are deferred until funds are withdrawn. This allows your investments to grow without the drag of current taxation.

For example, consider Jen, who begins contributing to a Self-Directed IRA at age 22. If she contributes $365 annually through age 70 and earns an 8% annual return, her account would grow to approximately $193,210. Assuming a 25% income tax rate, the same investment in a taxable account would grow to only $99,265 due to ongoing tax liability on investment gains.

This example highlights the power of tax deferral. By allowing earnings to compound without annual taxation, a Self-Directed IRA can significantly increase long-term retirement savings.

Where Can I Open a Self-Directed IRA?

IRAs were created in 1974 by ERISA. When IRAs were created, ERISA did not distinguish between an IRA that invested in traditional or alternative assets, such as real estate. When it comes to making investments with a Self-Directed IRA, the IRS generally does not tell you what you can invest in, only what you cannot invest in. The types of investments that are not permitted to be made using retirement funds is outlined in Internal Revenue Code Sections 408 and 4975. These rules are generally known as the “Prohibited Transaction” rules. Other than life insurance, collectibles, and transactions that involve or directly or indirectly benefit the IRA holder or a “disqualified person,” one can use their IRA to make the investments. A “disqualified person” is generally defined as the IRA holder and any of his or her lineal descendants and/or any entities controlled by such persons. Note – siblings are not considered “disqualified persons.”

Traditional financial institutions do not allow IRAs to invest in IRS-approved alternative assets, such as real estate, because their focus is on earning fees through traditional investments. Hence, the birth of the Self-Directed IRA industry. Today, the Retirement Industry Trust Association (RITA) estimates anywhere between 4-7% of all IRAs are invested in alternative assets. Accordingly, the Self-Directed IRA is the only way one can purchase alternative assets in an IRA.

Rollover Rules & The Self-Directed IRA

There are two general ways to fund an IRA: (i) IRA contribution and (ii) IRA transfer/rollover.

IRA Contribution

The first is making an IRA contribution. In 2026, one can contribute up to $7,500 or $8,600 if over the age of 50 to an IRA or Roth IRA, subject to certain income limitations. In order to make an IRA contribution, one must have earned income. Passive income, such as capital gains, does not count as earned income.

IRA Transfer/Contribution

To permit tax-free transfers of retirement savings from one type of investment to another, as well as to increase the portability of qualified plan rights for employees moving from one job to another, Congress permitted the transfer of IRA funds between IRAs and the rollover of 401(k) funds to IRA under certain circumstances. In general, a rollover of retirement funds to an IRA is tax-free. Rollovers can either be direct or indirect. A direct rollover can be done without limit, whereas an indirect rollover can only be done once every 12 months.

IRA Transfer

A rollover from one traditional IRA to another Traditional IRA is called a transfer and can be done without limit. A transfer occurs between IRAs and a rollover occurs when one of the retirement accents involved is not an IRA. For example, moving funds from a 401(k) plan to an IRA is treated as a direct rollover, whereas, moving funds between IRAs is called a transfer. A transfer of IRA funds can be done in cash or in-kind.

401(k) Rollover

In general, to move funds from a 401(k) plan to an IRA, a “triggering event” is required. Common triggering events include: (i) reaching age 59½, (ii) separating from service, meaning leaving your employer, or (iii) plan termination. Some plans may also allow in-service distributions, depending on their specific rules.

If funds are transferred directly from a 401(k) plan to an IRA, known as a direct rollover, the transaction is not subject to taxes or penalties. However, if the distribution is paid directly to the participant, known as an indirect rollover, the plan is required to withhold 20% for federal taxes. To avoid taxes and penalties, the full distribution amount, including the withheld 20%, must be redeposited into an IRA within 60 days.

In Jen’s case, she can fund a Self-Directed IRA using $175,000 from her existing IRA and $125,000 from her former employer’s 401(k) plan.

If Jen is under age 59½ and still employed with the company sponsoring the 401(k), she may not have access to those funds unless the plan permits an in-service distribution. If no such option is available, she could consider a 401(k) loan, if allowed by the plan. The loan amount is generally limited to the lesser of $50,000 or 50% of the account balance. The loan must typically be repaid within five years, unless used to purchase a primary residence. The interest rate is set by the plan and is often based on the prime rate plus a margin.

How to Buy Real Estate in a Self-Directed IRA

On top of having the advantage of sheltering Self-Directed IRA income and gains to tax, establishing a Self-Directed IRA is also a great way to better diversify your retirement savings, gain the ability to hedge against inflation, invest in assets you know and trust, as well as gain exposure to potentially lucrative investments, such as real estate, investment funds, as well as cryptos.

The following are the two most common Self-Directed IRA structures.

On top of having the advantage of sheltering Self-Directed IRA income and gains to tax, establishing a Self-Directed IRA is also a great way to better diversify your retirement savings, gain the ability to hedge against inflation, invest in assets you know and trust, as well as gain exposure to potentially lucrative investments, such as real estate, investment funds, as well as cryptos.

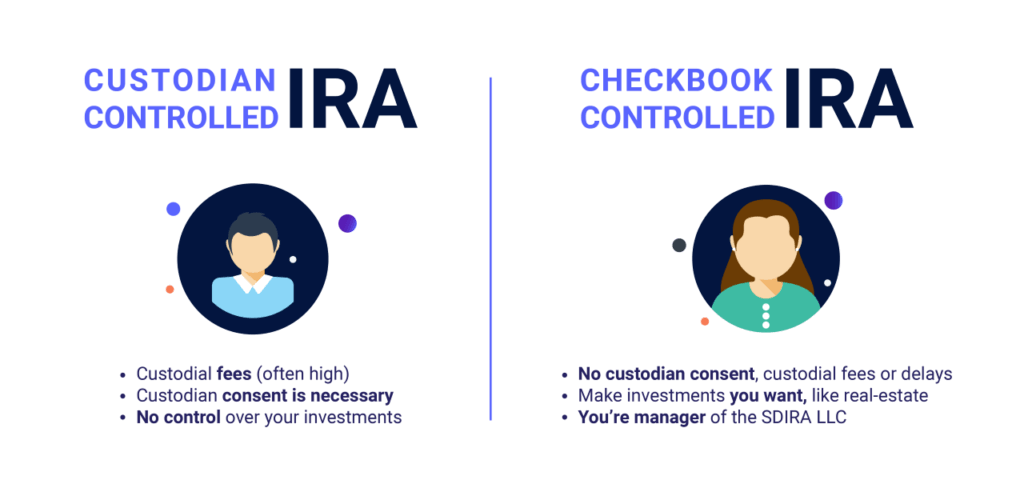

- Self-Directed IRA – Full-Service

- Self-Directed IRA LLC – “Checkbook Control”

With a Self-Directed IRA with checkbook control, an IRA is set-up with a Self-Directed IRA custodian, such as IRA Financial. The IRA is then invested into a special purpose limited liability company (“LLC”), which IRA Financial can help you establish. The Self-Directed IRA LLC is then managed by the IRA owner providing the IRA owner with “checkbook control” over the IRA funds. With a “checkbook control” Self-Directed IRA LLC, the manager of the Self-Directed IRA LLC will have the authority to make investment decisions without the involvement of the custodian. Plus, a Self-Directed IRA LLC will offer the IRA owner with limited liability protection over IRA investments. Moreover, all Self-Directed IRA investments will be titled in the name of the LLC offering the IRA owner more privacy. without needing the consent of an IRA custodian. With a Self-Directed IRA LLC with “Checkbook Control’ you will be able to buy real estate by simply writing a check.

All types of IRAs can be transferred tax-free to a Self-Directed IRA LLC. A Self-Directed IRA with “checkbook control” is popular with IRA investors seeking to invest in alternative assets, such as rental properties, fixes and flips, tax liens, or cryptocurrencies that require a high frequency of transactions.

Thus, Jen would have the option of using a Self-Directed IRA or a Self-Directed IRA LLC with “checkbook control” to do her real estate deal. For real estate investors who will be engaged in a higher frequency of activity, such as a flipper, who will need to engage and pay multiple third parties as part of the real estate improvement process, the use of the “checkbook control” LLC is a far more popular choice. In addition to gaining more control over the real estate rehab process, Jen would also get limited liability protection and a greater degree of privacy. Whereas, if Jen was buying a piece of land to hold or investing in a real estate passive fund, the use of the IRA LLC would be far less important.

Real Life Example of Buying Real Estate in a Self-Directed IRA

Real estate is the most popular investment class for Self-Directed IRA investors. The reason for this is that real estate is a tangible asset that is easy to understand. Real estate is also proven to be a great way to hedge against inflation as well as a key investment diversification tool.

Buying real estate with a Self-Directed IRA is quite simple and easy. Below is the steps Jen took to buy and sell real estate in her Self-Directed IRA. Continue reading and you will see how Jen’s real estate investment turned out.

Jen locates a real estate property and performs her diligence. She makes an offer to purchase the property. The offer is made in her name with the right to assign to her Self-Directed IRA. Jen establishes a Self-Directed IRA with IRA Financial IRA Financial initiates the tax-free IRA transfer for Jen.

She initiates the former employer 401(k) plan rollover to her new Self-Directed IRA. Jen is notified by IRA Financial when the IRA and former employer 401(k) funds arrive at IRA Financial. Since Jen elected to use a Self-Directed IRA LLC with “checkbook control,” Jen provides IRA Financial with the LLC details, such as proposed name and address in the state. Since the real estate would be located in Texas, IRA Financial recommends that Jen establish the LLC in Texas.

Jen notifies her real estate agent that she wishes to purchase the real estate in the name of an LLC. IRA Financial establishes the Texas LLC for Jen, which she calls Applesouth Investments LLC. Jen elects to be the manager of the LLC giving her checkbook control. IRA Financial also acquires a Tax ID# for the LLC and prepares an LLC operating agreement.

Jen elects to open a bank account at Capital One, a banking partner of IRA Financial. Jen is free to open the LLC bank account at any local bank of her choice, but she likes the fact that IRA Financial can establish her LLC bank account in minutes without her having to step foot in a bank.

At Jen’s direction, IRA Financial sends the $300,000 of IRA funds into the new LLC bank account. Jen provides all the LLC-related info to her real estate agent for closing.

At closing, Jen signs the real estate purchase documents as manager of the LLC. Title to the real estate is in the name of Applesouth Investments LLC. The purchase price of the home is $242,000.

After closing, Jen starts using her IRA funds from the Applesouth Investments LLC bank account to pay the contractor and other service providers. In all Jen, spends $35,000 on improvements to the home. Six months later, Jen puts the home up for sale for $385,000 and sells it for $380,000.

In six months, using her Self-Directed IRA, Jen made $103,000 tax free. Jen sold the property for $380,000 and she was able to buy the property for $242,000 and sent $35,000 on improvements. If Jen used personal funds, she would have had to pay ordinary income tax on the $103,000 of gain since she held the property less than 12 months. She is now looking for her next real estate project and has $103,000 more funds to spend in order to generate an even bigger tax-free gain.

Tips For Using a Self-Directed IRA to Flip Real Estate

- The deposit and purchase price for the real estate property should be paid using IRA funds or funds from a non-disqualified third party.

- No personal funds or funds from a “disqualified person” should be used.

- All expenses, repairs, and taxes incurred in connection with the Self-Directed IRA Plan real estate investment should be paid using retirement funds – no personal funds should be used.

- If additional funds are required for improvements or other matters involving the real estate investments, all funds should come from the Self-Directed IRA or a non “disqualified person.”

- If financing is needed for a real estate transaction, only non-recourse financing should be used. A non-recourse loan is a loan that is not personally guaranteed and whereby the lender’s only recourse is against the property and not against the borrower.

- No services should be performed by the IRA owner or “disqualified person” in connection with the real estate investment. In general, other than typical trustee type of services (necessary and required tasks in connection with the maintenance of the plan), no active services should be performed by the IRA owner or a “disqualified person” with respect to the real estate transaction.

- Title of the real estate purchased should be in the name of the IRA custodian for the benefit of the IRA owner. For example, IRA Financial Trust Company FBO John Doe IRA. However, in the case of a Self-Directed IRA LLC, the title to the real estate would be in the name of the LLC.

- Keep good records of income and expenses generated by the real estate investment.

- All income, gains, or losses from a Self-Directed IRA real estate investment should be allocated back to the IRA.

- Make sure you perform adequate diligence on the property you will be purchasing especially if it is in a state, you do not live in

- Make sure you will not be engaging in any self-dealing real estate transaction that would involve buying or selling real estate that will personally benefit you or a “disqualified person.”

Conclusion

Using a Self-Directed IRA to flip real estate is one of the best legal hidden tax-shelters. Most real estate investors are aware of the 1031 exchange solution. However, the Self-Directed IRA essentially provides a real estate investor with the same tax-free advantages. The case of Jen highlighted the major tax advantages one can enjoy using a Self-Directed IRA to flip real estate, along with investment diversification and the ability to invest in a hard asset you can trust. Today, establishing a Self-Directed IRA is easier and more cost-effective than ever before. The whole process will take just a few days and the set-up and ongoing fees can be paid using either IRA or personal funds. Best of all, companies such as IRA Financial charge annual low flat fees so as your IRA assets grow in value, you will still pay the same low annual fee. What are you waiting for? Join Jen and the millions of other Self-Directed IRA investors who have gained the freedom to take control of their retirement funds to invest in almost anything they want tax-free.

Contact Us

Hedge Fund with a Self-Directed IRA LLC

You can purchase a hedge fund with a Self-Directed IRA. Although the IRC doesn't describe what the Self-Directed IRA can invest in, it describes what it cannot invest in. Internal Revenue Code Sections 408 & 4975 prohibit Disqualified Persons from engaging in certain transactions.

The purpose of these rules is to encourage IRA holders to accumulate savings for their retirement. However, it also acts to prevent those in control of IRAs from taking advantage of tax benefits for their personal gains.

When it comes to using retirement funds to invest in a hedge fund, it is important to be mindful of the IRS-prohibited transaction rules. This includes disqualified persons in relation to your Self-Directed IRA LLC.

The Advantage of the Hedge Fund

A hedge fund is an alternative investment vehicle available only to sophisticated investors. This includes institutions and individuals with significant assets. In general, retirement funds are permitted to invest in hedge funds. The prohibited transaction rules tend to become more of an issue when the person using the IRA funds or any disqualified person related to the IRA owner has a personal interest or relationship with the hedge fund investment. In other words, an IRA can generally make an investment into a hedge fund in which neither the IRA holder nor any disqualified person has any personal ownership or relationship with.

The issues begin to arise from an IRS-prohibited transaction standpoint when the IRA owner wishes to use retirement funds to invest in a hedge fund where or she or a disqualified person is either an owner, employee, or, in some cases, has a professional relationship with the fund in question.

In general, if structured correctly, there may be a way for one to use their retirement funds to invest in a hedge fund that one is personally involved in. The key is to make sure that the IRA investment into the hedge fund will not directly or indirectly personally benefit the IRA owners since that type of investment would likely trigger a prohibited transaction.

Hedge funds are structured as limited partnerships or LLCs. In the case of a limited partnership, a general partner (“GP”) is created that tends to perform all the hedge fund management tasks. The GP generally owns a small percentage of the partnership. The investors are limited partners (“LP”) of the partnership. A typical fee structure for a hedge fund is the 2 and 20 model, which means the hedge fund manager will take a 2% management fee of all assets under management and then take 20% of the profits generated by the fund after the LP investors have received their money they invested back and, in some cases, a preferred return on the money invested is also returned to the investor.

A popular question is whether an individual who a principal is or in a management position with the hedge fund can use their retirement funds to invest in the fund. To begin with, the use of the retirement funds cannot be invested into the GP entity since that is the entity where the services are generally being performed on behalf of the hedge fund and where the management fee and carried interest are typically being directed as investing IRA funds into a company where the IRA holder has a personal ownership or is performing services as an employee would likely violate the IRS prohibited transaction rules. Therefore, the question then becomes can the IRA holder who has some personal ownership in the hedge fund use retirement funds to invest as an LP of the fund?

The answer generally depends on the facts and circumstances involved in the transaction. However, in general, there are ways that one can properly structure an investment of retirement funds into a hedge fund in which the IRA holder has some personal interest. The main question that needs to be asked and answered positively is if the IRS looked at the transaction, could they argue that the IRA owner has in any way directly or indirectly personally benefited by the IRA investment.

Related: Alternative Investments in an IRA

If the IRA owner cannot prove that he or she did not receive any direct or indirect personal benefit from the IRA investment into the hedge fund, then the IRS would likely argue that the investment triggered a prohibited transaction. Since the onus is always on the taxpayer to disprove a claim made by the IRS, it is crucial that the IRA owner who is seeking to make a retirement investment into a hedge fund in which he or she has some personal connection be extremely confident that he or she can prove, if requested, that no personal benefit was derived from the retirement account investment, either directly or indirectly. Accordingly, when it comes to using retirement funds to make investments into a hedge fund in which the IRA owner has a personal relationship, issues such as the management fee and carried interests are items that need to be taken into account when structuring the self-directed IRA hedge fund investment.

The IRS Standpoint on Hedge Fund Investments

The Tax Court in Rollins v. Commissioner, a 2008 Tax Court case, offers some insight as too how the IRS looks at transactions that involve investments into entity’s where the IRA owner has a small ownership interest in. Even though the Rollins case not involve using retirement funds to invest in a hedge fund, it nevertheless offers some insight as to the IRS thoughts on the application of the IRA self-dealing and conflict of interest rules.

The Rollins case is especially helpful in examining how the IRS could look at a transaction involving the use of retirement funds into a hedge fund in which the IRA owner has some personal relationship or ownership interest. Mr. Rollins was a CPA who had an ownership in several companies. One of the companies, in which he owned less than 10%, served as a director, but received no compensation, was in financial trouble and needed additional funds. Mr. Rollins decided to use his 401(k) plan funds to lend the company money at prevailing interest rates. The IRS audited the transaction and argued that the loan from Mr. Rollins 401(k) plan to the company was a prohibited transaction as the loan personally benefited him.

The Tax Court agreed and basically stated that even though the company was not itself a disqualified person because Mr. Rollins owned less than 50% of the company, nonetheless he could not provide that he did not directly or indirectly personally benefit from the loan made to the company by his 401(k) plan. Clearly, the Tax Court felt that Mr. Rollins personally benefited from the loan since without the loan his investment would have been lost. The Rollins case is a good illustration of how the IRS could view an investment into a hedge fund by an IRA owner who has some personal interest in the hedge fund below the 50% ownership threshold.

Navigating Hedge Fund Investments

Below are several examples that highlight the complexities involved in structuring an investment of retirement funds into a hedge fund in which the IRA owner has some personal relationship or ownership.

1. Joe is looking to start a hedge fund and needs $100,000 to begin operations. The hedge fund would be a limited partnership and Joe would be charging a traditional 2% management fee and 20% carried interest on fund profits. Joe will own 100% of the general partner of the hedge fund and is looking for investors to invest in the hedge fund. Joe wishes to use his IRA funds to invest in his hedge fund.

Issues for Joe to consider

Joe would clearly not be able to use his IRA funds to invest in the general partner since he will own 100% of that entity personally and that would likely trigger a prohibited transaction. What if Joe wanted to invest the funds as a limited partner of the fund? Unfortunately, there is no clear answer to this question as the answer is generally dependent on the facts and circumstances involved in the transaction. For example, if the only way Joe could attract investors to the fund is to show he also has invested in the fund and the only funds he had available to invest were IRA funds, the IRS could argue that the use of his IRA funds would personally benefit him since without his IRA funds being used he would not be able to attract investors to his fund and derive a personal financial return from owning the fund.

2. Ben is a 2% partner at a hedge fund that has $500 million under management. The hedge fund is set-up as a limited partnership. The hedge fund has a traditional fee model of 2% management fee and 20% carried interest. The hedge fund is looking to raise an additional $250 million and Ben is seeking to use $250,000 from his IRA to invest as a limited partner of the fund. His limited partnership interest would be 2.5% of the total fund.

Issues for Ben to consider

Ben is clearly a disqualified person because he is the IRA holder, but the hedge fund he is a partner at would likely not be since he owns just 2% of the fund, pursuant to Internal Revenue Code Section 4975(e)(2). However, the self-dealing or conflict of interest rules under Internal Revenue Code Section 4975(c)(1)(D) and (E) could treat Ben’s investment into the fund as a prohibited transaction. The question Ben must ask himself is whether he would receive any personal benefit, either directly or indirectly, from making the fund investment with his IRA funds. For example, would the fund be in financial trouble without Ben’s investment? Will Ben receive a salary bonus if he invests in the fund? Or what if, Ben is required to invest in the fund in order to maintain his position as partner of the fund? These are some of the facts that would need to be examined before determining whether Ben’s investment would rise to the level of a prohibited transaction.

3. Steve is a 99% owner of hedge fund A, which has over $750 million in assets under management. The hedge fund is set-up as a limited partnership. The hedge fund has a traditional fee model of 2% management fee and 20% carried interest. The hedge fund is looking to create fund B, which will be exclusively investing in a pool of loans. Fund B will be looking to raise $500 million from outside investors. Steve and a number of hedge fund A executives want to invest their retirement funds into fund B, but expect to own less than 5% of fund B. Fund A will be charging a management fee and carried interest on the limited partners of fund B.

Issues for Steve to consider

Since Steve owns 99% of hedge fund A and hedge fund A will be receiving a fee from the limited partners of fund B, a management fee and carried interest allocated to Steve’s IRA and potentially his executives could violate the prohibited transaction rules under Internal Revenue Code Section 4975. Fees paid by Steve’s IRA to a company he owns 99% of could be considered a prohibited transaction. What if Steve and his executives were able to have their IRAs exempted from the management fee and carried interest going to the general partner of fund A or were able to buy a different membership class of fund B, which did not have to pay any fees to hedge fund A. Because of Steve’s large ownership interest in hedge fund A, it is especially important that he focuses on the self-dealing and conflict of interest prohibited transaction rules to make sure his IRA investment into fund B could not be viewed as personally benefiting him directly or indirectly.

Unrelated Business Taxable Income

After examining the IRS prohibited transaction rules in order to determine whether an IRA investment into a hedge fund could be made, another set of IRS rules must be reviewed in order to verify whether a tax would be imposed on the income allocated to the IRA from the hedge fund investment.

In general, when it comes to using a Self-Directed IRA to make investments most investments are exempt from federal income tax. This is because an IRA is exempt from tax pursuant to Internal Revenue Code 408 and Section 512 of the Internal Revenue Codes exempt most forms of investment income generated by an IRA from taxation. However, in the case of the use of margin, non-recourse debt, or income generated from an active trade or business conducted via an LLC or partnership, a tax would be imposed on a percentage of the income generated. These rules have become known as the Unrelated Business Taxable Income rules or UBTI or UBIT. If the UBTI rules are triggered, the income generated from that activities will generally be subject to close to a 40% tax for 2018. The UBTI generally applies to the taxable income of “any unrelated trade or business…regularly carried on” by an organization subject to the tax. The regulations separately treat three aspects of the quoted words—“trade or business,” “regularly carried on,” and “unrelated.” In the case of an IRA, all active business activities will be treated as unrelated.

So why have I never heard of these rules before? The reason is that since most Americans with retirement funds invest in publicly traded stocks or mutual funds, which are often structured as a “C” Corporation, an entity subject to tax. A “C” corporation is also known as a blocker corporation. Unlike an LLC, which is treated as a passthrough entity, income from a “C” Corporation is blocked or stays in the “C” Corporation and does not flow to the shareholder. Whereas, income from an LLC passthrough the to the member/owner of the LLC – there is no entity tax with an LLC or partnership. Hence, any income allocated to an IRA via an LLC or passthrough entity would not be subject to an entity level tax and could be subject to the UBTI tax if the LLC was engaged in an active trade or business or margin or debt was used by the LLC. In other words, if one buys stock of a “C” corporation with a retirement account, the UBTI tax rules would not apply. Whereas, if one purchased an interest in a passthrough entity, such as an LLC, with IRA funds and the LLC was engaged in an active trade or business, used margin, or acquired debt, then the income allocated to the IRA could be subject to the UBTI tax.

In the case of an IRA investment into a hedge fund, if the hedge funds activities rise to the level of a trade or business, or if margin or debt is used in the hedge funds trading activities, then even though the investment may not violate the IRS prohibited transaction rules, the income could be subject to the UBTI tax rules. Since most hedge funds are structured as passthrough entities, gaining a solid understanding of the UBTI tax rules is extremely important.

Using retirement funds to invest in a hedge fund is not on its face a prohibited transaction, however, when the IRA owner has some personal involvement with the hedge fund, the IRS-prohibited transaction rules must be closely examined to make sure the investment would not trigger a prohibited transaction.

Related: How to Avoid Unrelated Business Taxable Income with a Self-Directed IRA

Get in Touch

The tax professionals of the IRA Financial have helped hundreds of hedge fund investors use their retirement funds to make hedge fund related investments, including in their own funds, and have significant experience in this area.

What is a Non-Recourse Loan and How does it Work?

Since the creation of IRAs in 1974, real estate has become a popular investment category for millions of retirement account investors. Many IRA or 401(k) investors will use their retirement funds to purchase real estate directly with account funds. However, with real estate prices rising over the last several years, more investors have looked to borrowing funds to buy properties. What is a non-recourse loan and how does it affect retirement account investments?

- When borrowing funds to make a retirement account investment, the loan must be non-recourse

- A Self-Directed IRA or Solo 401(k) can be used to make alternative asset investments

- When using an IRA to finance a property, be aware of the UBTI tax

Recourse & Non-Recourse Real Estate Loans

What is a Recourse Loan?

The most common type of real estate loan is a recourse loan. It is a loan personally guaranteed by the borrower. Almost all residential mortgages are recourse loans. Having a recourse loan means that if there is a default, the lender can attempt to cure it by not only seizing the underlying real estate but also pursuing the individual borrower personally. The recourse mortgage is what caused many borrowers to declare bankruptcy in the 2008 financial crisis because the equity they had in the real estate investment collapsed which forced the lenders to pursue the individual borrowers personally. Today, most residential, and commercial mortgages are still recourse.

The IRS and Retirement Account Recourse Loans

Internal Revenue Code (IRC) Section 4975 prohibits the IRA owner from personally guaranteeing a retirement account loan. Specifically, 4975(c)(1)(B) holds that a disqualified person cannot lend money or use any other extension of credit with respect to a retirement account.

As a result, in the case of a Self-Directed IRA, one could not use a standard loan, such as a mortgage, as part of an IRA transaction since that would trigger a prohibited transaction. This leaves the Self-Directed IRA investor with only one financing option – a non-recourse loan.

Related: Self-Directed IRA for Real Estate

What is a Non-Recourse Loan?

A non-recourse loan is a loan that is not guaranteed by the borrower. The lender is securing the loan by the underlying asset or real estate that the loan will be used for. Hence, if the borrower is unable to repay the loan, the lender’s only remedy is against the underlying asset and not the borrower personally.

Below are some common characteristics of a non-recourse loan:

- The loan cannot be personally guaranteed by the borrower. Verify loan documents that this is the case.

- Most non-recourse lenders will require at least 30% equity down; others will want at least 40%.

- Expect to pay a higher interest rate for a non-recourse loan since the lender is taking more risk.

- Many lenders will not do a non-recourse loan associated with a real estate project in certain states (such as New York and Vermont) that have very pro-tenant rules, which make foreclosure difficult.

- Do your diligence on the nonrecourse lender and don’t be afraid to shop your deal around. (For Self-Directed IRA and Solo 401(k) real estate investors, IRA Financial has a number of non-recourse lenders that our clients work with.)

In general, a non-recourse loan is far more difficult to secure than a traditional recourse loan or mortgage.

Tax Treatment of Using a Non-Recourse Loan

Most investments made with a retirement plan will be tax-deferred (or tax-free in the case of a Roth account). However, the use of a non-recourse loan in connection with an IRA or 401(k) investment could trigger a tax known as UBTI, Unrelated Business Taxable Income.

In general, if non-recourse debt financing is used, the portion of the income or gains generated by the debt-financed asset will be subject to the UBTI tax. For example, if an individual invests 80% IRA funds and borrows 20% using a nonrecourse loan, 20% of the income or gains generated by the investment would be subject to the UBTI tax.

As stated earlier, the IRS allows IRA and 401(k) plans to use non-recourse financing only. The rules covering the use of non-recourse financing by an IRA can be found in IRC Section 514 which requires debt-financed income to be included as unrelated business taxable income, which generally triggers a maximum tax of 37% tax in 2023.

401(k) Exception

When one uses non-recourse financing to invest in real estate with a 401(k), there is no UBTI tax, pursuant to IRC Section 514(c)(9). To take advantage of this exception, generally, you need to be self-employed to be eligible for a Solo 401(k) plan. The reason for this is that most traditional 401(k) providers do not allow for alternative investments. A Solo 401(k) allows you the freedom to invest in just about anything you want, including real estate.

Conclusion

An investor looking to invest in real estate with retirement funds who also wishes to use leverage to purchase the property, or another asset may only use a non-recourse loan. The procedures for acquiring a non-recourse loan are essentially the same as a mortgage. However, since the borrower is not personally guaranteeing the loan, the lender will require more cash down and will generally charge a higher interest rate.

It's up to you as the investor to weigh the pros and cons when using leverage to make a real estate investment. The more retirement funds you use, the less tax you will owe from the income generated by the financed investment. Alternatively, if you are self-employed, you can completely avoid the UBTI tax.

The Self-Directed IRA Rollover Rules

Self-Directed IRA Rollover

Rollovers are the most common way to transfer funds to a self-directed IRA. A transfer and rollover are two transactions that allow you to move your retirement assets between IRAs (individual retirement accounts) and 401(k) plans.

In general, all transfers or rollovers between retirement funds are not subject to any tax. Transfers occur between individual retirement accounts. A rollover occurs between an IRA and another type of retirement account, like a 401(k) plan. In other words, a transfer occurs when you send funds from one IRA to another. A rollover occurs when you transfer funds between an IRA and a different retirement account, like a 401(k) or 403(b).

When you roll over a retirement plan distribution, you don't usually pay tax until you withdraw it from the new plan. By rolling over, you’re saving for your future and your money continues to grow tax deferred.

How To Complete a Self-Directed IRA Rollover?

Direct Rollover

If you receive a distribution from a retirement plan, ask the plan administrator to make the payment directly to another retirement plan. Or ask that it go to a Self-Directed IRA. The administrator may issue the distribution in the form of a check. This will be made payable to your new account. No taxes are withheld from your transfer amount.

Trustee-to-trustee transfer

You can also complete a self-directed IRA rollover using the trustee-to-trustee transfer. If you receive a distribution from an individual retirement account, ask the financial institution holding the IRA to make the payment directly from that IRA to another IRA. For example, you can have the funds sent to a Self-Directed IRA or to a retirement plan. No taxes will be withheld from your transfer amount.

60-day rollover

If a distribution from an IRA or a retirement plan is paid directly to the retirement account holder individually and is not going directly to the retirement account, you can deposit all or a portion of it in an IRA or a retirement plan within 60 days. This is an indirect rollover.

Indirect rollover in Depth

If you take a 60-day rollover of cash (indirect rollover), then you must return the same amount within 60-days. For example, if you tax a 60-day rollover of $45,000 from your IRA, you need to return the $45,000 within 60 days. If you take out $5,000 and purchase a piece of land, you can't use the land as part of the 60-day rollover. In other words, cash for cash or property for property. This is what's necessary in order to satisfy the 60-day rollover rule.

In the example above, let's assume you return $35,000 of the $45,000 rollover amount. Only the $10,000 would be subject to tax. Additionally, you will have a 10% early distribution penalty if you're under the age of 59 1/2.

An indirect rollover occurs when the individual retirement account assets or qualified retirement-plan assets are moved. It first goes to the IRA holder or plan participant before ultimately going to an IRA custodian. Usually, you have 60 days from receipt of the eligible rollover distribution to roll the funds into an IRA. The 60-day period starts the day after you receive the distribution. There are typically no exceptions to the 60-day time period. There are cases where the 60-day period expires on a Saturday, Sunday, or legal holiday. As a result, you may execute the rollover on the following business day.

Related: Alternative Investments & IRA Custodians

Measurements to Avoid Abuse

To avoid abusing the rule, the tax code prescribes that taxpayers can only complete an IRA rollover once a year. Or, once in a twelve-month period. In the past, the IRS (Internal Revenue Service) has interpreted this to apply to IRAs on an account-by-account basis. As a result, this treatment of "separate accounts" due to the IRA rollover rule potentially allows taxpayers to chain together multiple IRA rollovers. This will be in an attempt to avoid the one-year rule and gain "temporary" use of IRA funds for an extended period of time.

It may seem like the Internal Revenue Service's Publication 590 suggests that the 60-day rule applies to separate IRA accounts. Yet many tax professionals often advise clients that the IRS may interpret the rule to apply to all IRAs. This is because of the potential for abuse of the 60-day distribution rule.

Bobrow Case – One Indirect Rollover Allowed Every 12 Months

A recent tax court decision clarified how the IRS interprets the 60-day rollover rule and whether it applies to all IRAs or to separate IRAs. With the decision in Bobrow versus Commissioner, the IRS shut down the separate-individual retirement accounts rollover strategy altogether. In the aftermath of the Bobrow case, the IRS issued the IRS Announcement 2014–15, stating that it would:

- assent to the tax court decision

- update its proposed regulations and Publication 590

- issue new proposed regulations soon that will definitively apply the one-year IRA rollover rule on an IRA-aggregated basis going forward

So what does all this mean?

It is important to remember that this 60-day rule applies only to indirect rollovers. In other words, to funds that you do not transfer directly between retirement account custodians. This includes financial institutions, banks, trust companies, and so forth. When funds are moved from a retirement to a retirement account, that’s considered a direct rollover or IRA transfer. In that case, there is no 60-day limit or any limit on the number of direct rollovers that can be done in a year.

So in summary, as long as the funds are being moved from one retirement account to another, it can be done as often as you would like. And it’s only when the retirement funds are sent to you individually that you have 60 days to re-contribute those funds to a retirement account. You can only do this once every twelve months. Additionally, any amount that's not re-contributed is then subject to tax, as well as a ten percent penalty if you're under the age of 59 1/2.

60-Day Rollover from an IRA vs. 401(k) Plan

Taking a 60-day rollover is far more tax-efficient than an individual retirement account. The reason is, there's no withholding tax on the IRA rollover. Whereas, in the cases of a rollover from a 401(k) plan, taxes will be withheld from a distribution. You would have to use other funds to roll over the distribution amount. In general, before taking a distribution from a 401(k) plan, you have to satisfy a plan “triggering event.” In general, a “triggering event” is any event that allows the Plan participant (you) to become eligible to make a withdrawal. A triggering event can include the termination of employment with the employer that sponsors the plan, or even disability.

Therefore, if you are over the age of 59 1/2 or leaving your job, you are eligible to roll the 401(k) funds into an IRA without tax or penalty. The advantage of taking a taxable distribution from an IRS versus a 401(k) plan is that distributions from an IRA are not subject to the 20% withholding tax.

Summary

Self-Directed IRA transfers and rollovers are always tax-free and can be done without limit so long as the funds go directly from one retirement account to another. This is one of the reasons why they are done so frequently.

Two of the most common reasons for rolling over is not wanting to leave assets behind at the former employer (24 percent of traditional IRA–owning households with rollovers). The second is wanting to preserve the tax treatment of the savings (18 percent of traditional IRA–owning households with rollovers). Another 17 percent of traditional IRA–owning households with rollovers indicated their primary reason for rolling over was to consolidate assets.

Contact Us

If you have any questions about the Self-Directed IRA Rollover Rules, please give us a call at 800.472.0646 today.

ROBS Prohibited Transaction Rules

What are the ROBS Prohibited Transaction Rules?

The IRS-prohibited transaction rules are not triggered in a rollover business start-up (ROBS) solution. The ROBS solution allows one to use their IRA or rollover 401(k) funds to purchase stock in a C Corporation that they are personally involved in without triggering the IRS-prohibited transaction rules. Whereas, if a Self-Directed IRA was used instead of the ROBS solution, the purchase of corporate stock by the IRA would trigger the IRS prohibited transaction rules if the retirement account owner of their lineal descendants controlled the company.

Before we go further into that, let’s take another look at what the prohibited transaction rules entail. It will help you better understand why no ROBS-prohibited transaction rules are set in place.

If you have a retirement account, then you’re aware of the prohibited transaction rules. These rules don’t describe what you can invest in, only what you cannot invest in. You may also know why the Prohibited Transaction Rules are in place. The IRC doesn’t want you to use the funds in your retirement account for personal gains. The goal of the IRA is to accumulate as many funds until you reach retirement age and then make withdrawals.

Read More: Rollovers as Business Startups

Disqualified Persons

For the sake of clarification, what exactly is a disqualified person? In general, a disqualified person is:

- You (the IRA holder)

- Your lineal descendants

- Any entity controlled by such persons (greater than 50%)

The IRS believes that the IRA holder and his/her lineal descendants are one in the same. However, there are many more disqualified persons than what we have listed. You can review all disqualified persons in Solo 401(k) Prohibited Transaction Rules.

The prohibited transaction rules are also set in place because they protect the IRS revenue-generating rules.

If you use your retirement money to help your children or spouse, the IRS sees this as getting around the distribution rules (the minimum amount you can withdraw from your account each year). You aren’t paying taxes on the IRS accounts and at the same time, you’re benefiting by helping close family relatives.

These rules help the IRS in other ways, as well. For example, if you use your IRA funds and give them to your spouse, it’s as if you’re gaining use of the IRA funds without paying tax or the potential 10% penalty. Then everyone would take advantage of this to avoid paying taxes on their IRA funds.

Related: Rollover Business Startups (ROBS) Compliance Rules

How does this hurt the IRS?

Let’s look at an excerpt from Turning Retirement Funds into Start-Up Dreams.

“…The IRS would be left with very little tax revenue from the IRA account, and it would also lose tax revenue because of the use of the IRS deduction in the year of contribution…So prohibited transaction rules are actually very important for the IRS.”

Related: Potential Drawbacks to Using Rollover Business Startup Solutions

The Reason There are No ROBS Prohibited Transaction Rules

As you saw in ROBS Solution – How Can I Benefit and ROBS Solution – How it Works, individuals can break the prohibited transaction rules. Again, that’s because the ROBS solution takes advantage of the ‘qualifying employer securities’ exception in the tax code under IRC Section 4975(d) (13). This is an exception to the IRS prohibited transaction rules that allow the 401(k) to buy qualifying employer securities or stock of a C corporation. Doing so does not trigger the prohibited transaction rules like the self-directed IRA LLC will, for example.

With so many advantages to the ROBS solution, it’s time to think seriously about using it to start or finance your business. At IRA Financial Group, our IRA specialists will establish the ROBS today, and handle all necessary paperwork. Additionally, your assigned specialist will guide you through the process and answer any questions or concerns you may have. Contact us today to get started.

Related: How to Use Retirement Funds to Start a Business

Did You Know?

The ROBS solution can allow you to use funds from your Self-Directed IRA and Solo 401(k) to purchase a business that you can earn a salary from. It is the only legal way you can do it. You will need a C Corporation to do a Rollover Business Start-Up solution. Contact us today to learn more.

Using a Self-Directed IRA for Hard Money Lending

IRA Financial, the leading provider of Self-Directed IRA LLC and Solo 401(k) Plan solutions, announces a specially designed Self-Directed IRA LLC solution for hard money lenders looking to generate tax-deferred or tax-free returns. Because most financial institutions continue to require solid credit scores and spend weeks reviewing financial statements, tax returns, and business plans, there is a growing need for quick financing for many individuals, small businesses, and investors, especially real estate developers, and builders for their real estate projects. As a result, IRA Financial designed a special Checkbook Control Self-Directed IRA LLC program designed specifically for hard money lenders.

As a result of the very strong demand from hard money lenders to have more control over the loan process, we have developed a special Self-Directed IRA LLC solution specifically tailored for the hard money lender investor. Because of the very limited amount of financing available to most individuals and small businesses, many hard money lenders are eager to use their IRA or 401(k) funds to make loans and generate tax-deferred income or gains.

A Self-Directed IRA LLC offers one the ability to use his or her retirement funds to make almost any type of investment on their own without requiring the consent of any custodian or person in a tax-efficient manner. The IRS only describes the types of investments that are prohibited, which are very few. The main advantage of using a Self-Directed IRA LLC to make hard money loans is that the loan can be made by simply writing a check. In addition, all income and gains associated with the Self-Directed IRA hard money loan would grow tax deferred.

With IRA Financial Group’s Self-Directed IRA hard money lending solution, traditional IRA or Roth IRA funds can be used to make secured or unsecured private loans to small business owners or home builders.

The Self-Directed IRA for hard money investors is an IRS-approved structure that allows one to use their retirement funds to make hard money loans, either secured or unsecured, to any non-disqualified third party by simply writing a check. The Self-Directed IRA LLC involves the establishment of a limited liability company (“LLC”) that is owned by the IRA (care of the IRA custodian) and managed by the IRA holder or any third party. As manager of the IRA LLC, the IRA owner will have control over the IRA assets to make traditional as well as non-traditional investments, such as hard money loans by simply writing a check.

Additionally, a Solo 401(k) can be used for hard money loans.

IRA Financials Solo 401k allows you to use your retirement funds to invest in all types of debt instruments and products directly from your mobile device or PC securely and cost-effectively. You no longer need a third-party custodian involved in every aspect of your investment transaction. Buy, sell, or exchange notes on your own directly from a mobile device or PC with IRA Financial’s Solo 401(k). Rollover, deposit, or transfer funds between your investment and 401(k) seamlessly and without delay.

Learn More: Tips for Making Investment with a Solo 401(k)

Why Notes/Hard Money Loans