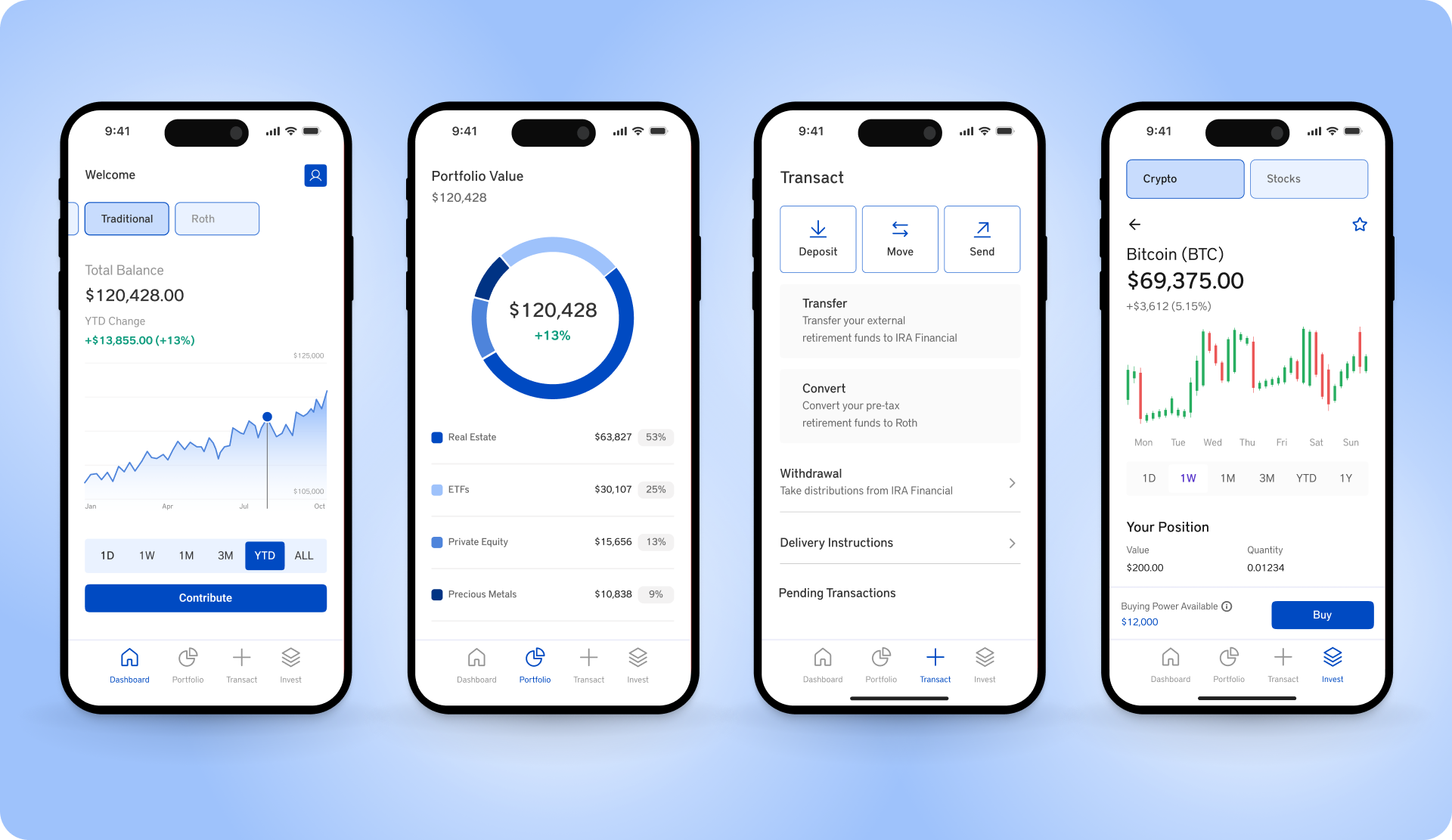

IRA Financial vs American IRA

When it comes to self-directed retirement investing, IRA Financial and American IRA take different approaches. American IRA is a Third Party Administrator working with New Vision Trust Company as custodian, with a flat fee structure built around choosing between a lower base fee with per-transaction charges or a higher flat fee with unlimited transactions. IRA Financial is built for investors who want one simple flat fee, modern technology, and a broader set of account structures.

In this comparison, we'll break down how the two companies stack up across pricing, product offerings, technology, and reputation to help you decide which one fits your goals best.

Pricing & Fees: Transparent, Flat, and Investor-Friendly

When evaluating Self-Directed IRA custodians, fees are a major consideration for investors seeking to grow their retirement accounts efficiently. IRA Financial and American IRA both use flat annual fee models, but the similarities end there. IRA Financial's flat fee covers unlimited transactions with no add-ons. American IRA's comparable unlimited-transaction option carries a higher annual price tag, and investors who want a lower sticker price have to accept a per-transaction fee instead.

IRA Financial | American IRA | |

Setup Fee | $0 | $50 |

Annual Fee | $495 | $450 |

Asset Value Fee | $0 | $0 |

Investment Fee | $0 | $0 |

Free Trades | Unlimited | Unlimited |

Roth Conversion Fee | $0 | Not published |

1 Year Total Cost | $495 | $500 |

5 Year Total Cost | $2,475 | $2,300 |

Pricing pulled from company website, as of the article publish date, based on a $200,000 account balance and American IRA's unlimited transaction plan

IRA Financial:

- Flat, transparent annual fee of $495/year for a Self-Directed IRA, with no setup fee.

- No asset-based fees, no transaction fees, and no hidden charges.

- Low-cost crypto trading through the IRAfi Crypto app.

American IRA:

- $50 one-time setup fee, then a choice of two annual plans: $285/year plus $95 per transaction, or $450/year for unlimited transactions.

- $750 minimum cash balance required on the account.

- No dedicated crypto platform.

Summary

American IRA's flat, unlimited-transaction plan comes in slightly below IRA Financial's over five years at this balance. But that comparison assumes you pick the unlimited-transaction option every year, regardless of how much you actually trade. Investors who trade less often can switch to American IRA's lower-tier plan and pay per transaction instead, which means the true cost shifts depending on activity level and requires choosing the right plan each year to avoid overpaying. IRA Financial's fee stays the same no matter which option you'd otherwise have to pick.

Winner: IRA Financial.

Same flat fee every year with no plan to choose and no transaction count to track, versus a decision between two American IRA pricing tiers that only pays off if you guess your trading activity correctly.

Product & Service Offerings: Breadth vs. Integration

Choosing the right custodian depends on the types of investments you want to make and how much support you need getting there. IRA Financial and American IRA both give investors access to alternative assets, but their account structures and platform integration look different.

IRA Financial | American IRA | |

Account Type | ||

Self-Directed IRA | ||

Solo 401(k) | ||

HSA | ||

Checkbook Control | ||

ROBS Structure | ||

Platform & Investments | ||

Crypto Platform | ||

Stock Trading | ||

Compliance & Protection | ||

In-House Compliance & Tax Services | ||

IRS Audit Protection |

IRA Financial:

- Full range of traditional SDIRA investments plus direct crypto investing through IRAfi Crypto.

- Stock, ETF, bond, and options trading powered by Interactive Brokers - available as a $100/year add-on, fully integrated inside your IRA Financial account.

- Advanced structures including Solo 401(k), SEP and SIMPLE IRAs, HSA and Coverdell accounts, and ROBS for business funding.

- IRA Compliance Shield ($299/year): in-house audit protection, tax consultation, deal reviews, prohibited transaction pre-clearance, and UBIT/UDFI modeling.

American IRA:

- Covers the core alternative asset classes well: real estate, private lending, tax liens, precious metals, LLCs, and privately held companies.

- Offers Checkbook IRA LLC structures for single-member and multi-member accounts.

- No ROBS structure for entrepreneurs looking to fund a business with retirement funds.

- No dedicated crypto platform or integrated stock trading.

- No in-house compliance, tax consultation, or IRS audit protection services.

Summary

Both custodians cover the fundamentals of alternative asset investing well. Where they diverge is breadth. IRA Financial supports business funding through ROBS, direct crypto trading, and stock trading in the same account, while American IRA's offering stays centered on traditional alternative assets without those additional structures.

Winner: IRA Financial

More account types, direct crypto access, integrated stock trading, and in-house compliance support that American IRA does not offer.

Technology: Modern Platform vs. Traditional Portal

Technology plays a critical role in managing self-directed retirement accounts, especially for investors who want real-time visibility and digital tools. IRA Financial has invested in a mobile-first platform, while American IRA relies on a web-based client portal and leans into personalized, phone-based service.

IRA Financial:

- Newly-updated mobile app and account dashboard with clean UI/UX and modern functionality.

- Offers a fully digital on-boarding experience, automated compliance, and secure document storage.

- In-house crypto trading, real-time dashboards, and checkbook control in a single portal.

American IRA:

- Web-based Client Portal for account management, statements, and documents.

- No dedicated mobile app.

- Emphasizes live phone support over digital self-service.

Summary

American IRA's portal covers the basics, and their phone-first approach may appeal to investors who prefer talking to a person over using an app. But for investors who want mobile access and real-time digital tools, IRA Financial's platform is built for that from the ground up.

Winner: IRA Financial.

A modern, mobile-first platform with crypto trading, stock trading, and checkbook control in one login, versus a web portal with no mobile app.

Reputation & Customer Reviews: Trusted by Thousands

Reputation matters when trusting a custodian with your retirement assets. Both IRA Financial and American IRA have built track records in the self-directed space, but investor sentiment looks different depending on where you look.

IRA Financial | American IRA | |

Trustpilot | 4.8 / 5 | 1.7 / 5 |

4.3 / 5 | 4.6 / 5 |

IRA Financial:

- Strong reputation for fast account setup, responsive customer service, and straightforward pricing.

- Over 3,000 5-star reviews across Google, Trustpilot, and other platforms.

- Founded by tax attorney Adam Bergman, who educates investors via weekly videos, podcasts, and blog articles.

American IRA:

- Strong showing on Google, with reviewers frequently citing responsive staff.

- On Trustpilot, a small sample size of 18 reviews skews heavily negative, with recent reviews citing slow transfer processing and unresponsive follow-up.

- A+ rating with the Better Business Bureau.

Summary

American IRA's Google reviews paint a picture of a responsive, well-regarded team, but its Trustpilot score tells a very different story, and the gap is large enough that it's worth an investor's attention before opening an account. IRA Financial's reputation holds up consistently across every platform.

Winner: IRA Financial.

Consistent 4.4+ ratings across every major review platform, without the kind of wide platform-to-platform swing American IRA shows between Google and Trustpilot.

The Bottom Line: Why IRA Financial Is the Smarter Choice

Both IRA Financial and American IRA give investors access to self-directed retirement investing, and American IRA's flat-fee approach and personalized phone support are real strengths for the right investor. But for someone who wants one simple flat fee regardless of how they trade, broader account structures including ROBS, direct crypto access, and in-house compliance support, IRA Financial offers more.

Whether you're looking to invest in real estate, trade crypto, access public markets, or fund a new business with your retirement account, IRA Financial is designed to support every part of your retirement strategy, efficiently, affordably, and under one roof.

Book a free call with a self-directed retirement specialist

- Review your self-directed retirement options

- Learn about investing in alternative assets

- Get all of your questions answered

Why the New Housing Law Could Create the Best Real Estate Buying Opportunity in Years

For the past several years, real estate investors have had to compete against one of the largest buyers the housing market has ever seen: Wall Street.

Large institutional investors, private equity funds, hedge funds, and publicly traded real estate companies purchased hundreds of thousands of homes across the country. Armed with virtually unlimited capital, they frequently outbid individual investors with all-cash offers, driving home prices higher and making it increasingly difficult for everyday Americans to build wealth through real estate.

But markets change.

A recent CNBC article explains that many of these same Wall Street firms are now becoming net sellers of residential real estate. Political pressure, regulatory changes, rising financing costs, and weaker returns are all causing institutional investors to reduce their exposure to single-family homes.

I believe this creates a tremendous opportunity.

Earlier this year, Congress passed the 21st Century ROAD to Housing Act, one of the most significant housing bills in decades. Section 901 of the law, titled "Homes are for People, Not Corporations," restricts large institutional investors that own 350 or more single-family homes from purchasing additional existing properties. Firms that want to continue building rental portfolios must construct new homes rather than buying existing ones, and any new homes built for rental must be sold to individual homeowners after seven years. At the same time, many of these firms have already begun selling portions of their residential portfolios and redirecting capital elsewhere.

As a tax attorney who has spent more than 25 years helping Americans build retirement wealth through Self-Directed IRAs and Solo 401(k) plans, I believe this creates one of the most attractive real estate investment opportunities we have seen in years.

Key Takeaways

- The 21st Century ROAD to Housing Act restricts large institutional investors owning 350 or more single-family homes from purchasing additional existing homes, reducing competition for individual real estate investors for the first time in years.

- Many of the same Wall Street firms are already becoming net sellers of residential real estate, creating more inventory and potentially better pricing for long-term investors.

- A Self-Directed IRA can purchase rental properties, apartment buildings, commercial real estate, tax liens, mortgage notes, and other real estate investments, with rental income growing tax-deferred in a Traditional IRA or potentially tax-free in a Roth IRA.

- A Solo 401(k) has a significant tax advantage over an IRA for leveraged real estate: the Section 514(c)(9) exception generally eliminates the UDFI tax that would otherwise apply when a retirement account uses a non-recourse loan to purchase property.

- For investors who plan to use financing to acquire investment real estate, a Solo 401(k) should always be part of the conversation.

A Fundamental Shift in the Housing Market

For years, individual investors simply could not compete with institutional buyers. Imagine trying to purchase a rental property when your competition is a billion-dollar fund capable of paying cash and closing in days. That was the reality in many housing markets across the country.

The new law is designed to change that. One of its primary objectives is to limit future acquisitions of existing single-family homes by the largest institutional investors while encouraging capital to flow toward the construction of new housing instead. Whether you agree with the legislation politically is beside the point. From an investment standpoint, the practical effect is clear: one of the largest groups of buyers in the housing market is stepping back.

Why This Matters for Investors

Markets are driven by supply and demand. When one of the largest sources of demand begins leaving a market, opportunities follow.

No one can predict whether home prices will rise or fall over the next twelve months. But individual investors are likely to face meaningfully less competition than they did just a few years ago. Institutional investors are already selling properties, reallocating capital, and focusing on areas of real estate that remain outside the new restrictions. That means more inventory and potentially better pricing for long-term investors.

History has consistently shown that the best investment opportunities often appear when large institutional money is moving in the opposite direction.

Why Real Estate Belongs in a Retirement Portfolio

As a tax attorney, I spend most of my time discussing retirement accounts. But I have always believed that real estate deserves a meaningful place in a diversified retirement portfolio.

Unlike stocks, real estate generates recurring rental income while also appreciating over time. Property values are influenced by local economic conditions, population growth, replacement costs, and rental demand rather than quarterly earnings reports, which provides genuine diversification. Real estate also allows investors to use prudent leverage to increase purchasing power. Over long periods, these characteristics have helped millions of Americans build lasting wealth.

The question is not whether real estate belongs in a retirement portfolio. The better question is: what is the most tax-efficient way to own it?

Why a Self-Directed IRA Makes So Much Sense

Most investors assume IRAs can only purchase stocks, mutual funds, or ETFs. That simply is not true.

A Self-Directed IRA follows the exact same IRS rules as any traditional or Roth IRA. The difference is investment flexibility. A Self-Directed IRA can purchase rental homes, apartment buildings, commercial property, raw land, private real estate funds, tax liens, mortgage notes, and many other alternative investments.

Rental income generated inside a Traditional Self-Directed IRA generally grows tax-deferred. If held inside a Roth Self-Directed IRA, qualified rental income and appreciation may ultimately be distributed completely tax-free.

Consider purchasing a rental property for $500,000 inside a Roth IRA. Thirty years later, the property is worth $2 million. If all Roth requirements have been satisfied, that appreciation may never be subject to federal income tax. That is exactly why Congress created retirement accounts.

Book a free call with a self-directed retirement specialist

- Review your self-directed retirement options

- Learn about investing in alternative assets

- Get all of your questions answered

Understanding UBIT and When It Applies

One of the most common misconceptions about Self-Directed IRAs is that all rental income is subject to tax. That is incorrect.

Rental income from debt-free real estate is generally excluded from Unrelated Business Income Tax under Internal Revenue Code Section 512. Simply owning rental property inside an IRA without leverage does not trigger UBIT.

When borrowed money is involved, the rules change. If your IRA purchases a $1 million apartment building by contributing $400,000 and obtaining a $600,000 non-recourse loan, a portion of the rental income and any gain attributable to the financed percentage becomes subject to Unrelated Debt-Financed Income tax under Internal Revenue Code Section 514.

That does not mean investors should avoid leverage. Leverage has created tremendous wealth in real estate for generations, and even after accounting for UDFI, borrowing may substantially increase long-term returns by allowing retirement accounts to acquire larger, higher-quality properties. The key is understanding the rules before making the investment.

Why the Solo 401(k) Has a Major Advantage

This is where many investors miss one of the biggest tax opportunities in the retirement code.

Unlike IRAs, qualified retirement plans including Solo 401(k) plans generally qualify for the Section 514(c)(9) exception, which exempts qualifying leveraged real estate investments from the UDFI tax. That means a Solo 401(k) can generally purchase leveraged real estate using a non-recourse loan without paying the UDFI tax that would normally apply to an IRA.

In my opinion, this is one of the greatest tax advantages available to real estate investors. Unfortunately, many investors and even many financial professionals have never heard of it. For anyone who expects to use financing to purchase investment real estate, a Solo 401(k) should always be part of the discussion.

Diversification Has Never Been More Important

Today's stock market remains heavily concentrated in a relatively small number of technology and artificial intelligence companies. Those companies have produced tremendous returns, but concentration also creates risk.

Real estate offers exposure to an entirely different asset class that generates income differently, responds differently to economic conditions, and has historically helped reduce overall portfolio volatility. A diversified retirement portfolio should not rely entirely on one asset class.

Final Thoughts

The housing market is entering a new chapter. For years, Wall Street dominated the purchase of single-family homes, making it increasingly difficult for individual investors to compete. Today, that dynamic is shifting.

The 21st Century ROAD to Housing Act has fundamentally changed the landscape by limiting future purchases of existing single-family homes by the largest institutional investors. At the same time, many of those firms are already selling properties and shifting capital elsewhere. For long-term investors, this creates a rare opportunity.

When you combine potentially reduced competition with the powerful tax advantages of a Self-Directed IRA or Solo 401(k), you have a compelling strategy for building long-term retirement wealth. Rental income can grow tax-deferred, or completely tax-free inside a Roth account. Appreciation can compound for decades without annual taxation. And for investors using a Solo 401(k), the Section 514(c)(9) exception generally eliminates UDFI on qualifying leveraged real estate investments, making financing significantly more tax-efficient than it would be inside an IRA.

Successful investing is not just about finding the right asset. It is about owning that asset in the right structure. With Wall Street stepping back and retirement accounts offering some of the most favorable tax treatment available under the Internal Revenue Code, this may be one of the best opportunities in years for retirement investors to consider adding real estate to their portfolios.

3 Ways to Fund a Self-Directed IRA in 2026

The financial landscape of 2026 offers more opportunities and more complexity than ever before. As investors move beyond the traditional boundaries of Wall Street, the demand for alternative assets like real estate, private equity, and digital currency has reached an all-time high. Yet most retirement savers remain in conventional brokerage accounts that limit their choices to a pre-approved menu of stocks and mutual funds.

To truly diversify and capture the growth of the modern economy, you need to understand how a Self-Directed IRA works and how to fund one.

Key Takeaways:

- What a Self-Directed IRA is and how it differs from a standard IRA

- Why investors are moving toward alternative assets and self-direction

- The three funding pathways: transfer, rollover, and annual contribution

- 2026 contribution limits and income phase-out rules

Defining the Self-Directed IRA

In the eyes of the IRS, a Self-Directed IRA is not a distinct legal entity. It is a Traditional or Roth IRA held by a specialized custodian. While major retail banks and brokerages act as limited custodians that permit only the assets they sell, a true self-directed custodian like IRA Financial allows you to invest in virtually any asset the law allows.

The governing regulations under Internal Revenue Code Section 408 do not list what you can buy. They only list a few things you cannot buy, such as life insurance or collectibles. This means your retirement funds can legally own residential rentals, commercial real estate, private businesses, cryptocurrency, and precious metals, all while maintaining the exact same tax-advantaged status as a standard IRA.

Read more: Prohibited Transactions in Self-Directed IRAs: Rules and Compliance

Why Investors Are Making the Switch

The shift toward self-direction is driven by two core motivations: asset class diversification and inflation protection.

If your entire retirement is tied to the stock market, your future is exposed to systemic market shocks. A Self-Directed IRA lets you move into hard assets like real estate or private lending that often move independently of the S&P 500. That independence is what makes alternative assets genuinely diversifying rather than simply different.

The tax efficiency is equally compelling. When your IRA owns a rental property, the monthly rent check is not personal income. It is tax-deferred or tax-free growth inside your retirement account. You can buy, sell, and reinvest within the account without triggering a capital gains tax event, allowing your wealth to compound in a way that a taxable brokerage account simply cannot match.

https://youtu.be/adxCNjr49X0

Pathway 1: The Tax-Free IRA Transfer

The most common method for funding a Self-Directed IRA is a direct transfer. This is the process of moving funds from an existing IRA (Traditional, Roth, SEP, or SIMPLE) at one institution to a new SDIRA at another.

How it works

A transfer is a custodian-to-custodian movement of cash or assets. Because the funds move directly between financial institutions, the IRS does not treat this as a distribution.

- Tax-free and unlimited: You can initiate as many direct transfers as you wish in a single year with no tax withholdings and no penalties, provided the money moves from a like account to a like account (Traditional to Traditional, Roth to Roth)

- Direct vs. indirect: In a direct transfer, the money is sent via wire or check from your old institution to IRA Financial. In an indirect transfer, the old custodian sends the check to you personally

- The 60-day and 12-month rules: If you receive the funds personally, you have exactly 60 days to deposit them into your new SDIRA. Missing that deadline causes the IRS to treat the full amount as a taxable withdrawal. You are also limited to one indirect rollover every 12 months

To avoid these risks entirely, most investors use the direct transfer method. It is simpler, faster, and eliminates the compliance exposure that comes with handling the funds personally. IRA Financial handles the entire transfer process on the client's behalf, coordinating directly with the outgoing custodian to ensure funds move safely and within IRS guidelines.

Read more: Transfer Your IRA to a Self Directed IRA

Pathway 2: The 401(k) Rollover

In 2026, the movement of wealth from employer-sponsored plans into IRAs continues at a significant pace, with over $1 trillion rolling over annually. If you have a 401(k), 403(b), or Thrift Savings Plan from a former employer, you likely have capital sitting idle that could be working harder inside a Self-Directed IRA.

Understanding the triggering event

To move money out of an employer plan, the plan document typically requires a triggering event. The most common is separation from service, meaning you have left that employer. Many plans also allow in-service distributions for employees who have reached age 59½, even if they are still working.

Why a direct rollover matters

When moving 401(k) funds, a direct rollover is the right approach. If the check is made out to you personally, the plan is legally required to withhold 20% for federal taxes. That means if you have $100,000, you only receive $80,000, but you are still responsible for depositing the full $100,000 into your IRA within 60 days to avoid a penalty. A direct rollover avoids this entirely. The funds move in full, tax-free, and without limit.

Read more: How to Complete a Self-Directed IRA Rollover

Pathway 3: Annual IRA Contributions

If you are starting from scratch or want to add to an existing balance, you can fund your Self-Directed IRA through annual contributions.

2026 contribution limits

- Standard limit: $7,500 for those under age 50

- Catch-up limit: An additional $1,100 for those age 50 or older, bringing the total to $8,600

A Traditional IRA allows you to contribute funds that may be tax-deductible in the year they are made, lowering your taxable income today while allowing investments to grow tax-deferred until retirement.

Income limits and deductibility

While anyone with earned income can contribute to a Traditional IRA, the ability to deduct that contribution depends on your income and whether you or your spouse have access to a workplace retirement plan.

If neither spouse has a workplace plan: No income limits apply. Regardless of income level, both spouses can take a full deduction for their IRA contributions up to the applicable limit. This makes the Traditional Self-Directed IRA a particularly useful tool for high-earning couples who are self-employed or work for small businesses without a plan.

When only one spouse has a workplace plan: The tax code is generous here. For the covered spouse, a full deduction is available if joint MAGI is $129,000 or below, with the deduction phasing out completely at $149,000. For the non-covered spouse, the ceiling is much higher. A full deduction is available as long as joint MAGI is below $242,000, with the phase-out occurring between $242,000 and $252,000.

When both spouses have workplace plans: Both fall under the lower threshold. A full deduction is available only if joint MAGI is $129,000 or below, phasing out completely at $149,000.

Distribution rules

- Age 59½: Withdrawing earnings before this age typically results in a 10% penalty plus ordinary income tax

- Required Minimum Distributions: Under SECURE Act 2.0, once you reach age 73, or age 75 for those born in 1960 or later, you are required to begin taking annual distributions

Book a free call with a self-directed retirement specialist

- Review your self-directed retirement options

- Learn about investing in alternative assets

- Get all of your questions answered

Final Thoughts

A Self-Directed IRA is not a complicated product. It is a standard IRA with a wider investment universe and a provider who gets out of your way. The three pathways covered in this guide, transfers, rollovers, and annual contributions, are all straightforward when you understand the rules and work with a custodian who handles the process correctly.

The investors who benefit most from a Self-Directed IRA are not necessarily the most sophisticated. They are the ones who recognized early that limiting their retirement savings to a pre-approved menu of stocks and funds was leaving real opportunity on the table. If you are reading this guide, you are already asking the right question. The next step is simply getting started.

IRA Financial vs. FranFund

FranFund is a franchise-focused funding company that offers its own ROBS product under the FranPlan name. They've built a reputation in the franchising world for straightforward pricing, a dedicated TPA team, and a unique no-risk SafetyNet option that lets prospective clients start the rollover process before committing to setup fees.

IRA Financial takes a broader approach, serving entrepreneurs across all business types with a platform built on tax law expertise. Here's how the two compare.

What is ROBS?

A Rollover as Business Startups (ROBS) is a legal structure that allows you to use funds from a 401(k) or traditional IRA to finance a new or existing business without paying taxes or early withdrawal penalties. The process works by rolling your retirement funds into a new 401(k) plan sponsored by a C-Corporation you establish. That plan then purchases stock in the corporation, giving your business the capital it needs to operate or grow. Because the funds are invested rather than withdrawn, no taxes or penalties are triggered. You're using your own money to invest in your own business, debt-free. A ROBS is not a loan, so there are no interest payments or repayment schedules to worry about. It does, however, require strict compliance with IRS and Department of Labor regulations, which is why choosing an experienced provider is one of the most important decisions you'll make in the process.

Pricing and Fees: What You'll Actually Pay

FranFund publishes its pricing directly on their website, which is worth acknowledging. Setup and ongoing TPA fees are listed separately and clearly. IRA Financial bundles everything into a single annual fee after setup.

IRA Financial | FranFund | |

Setup Fee | $3,500 | $4,795 |

Annual Fee | $1,200 per year | $1,980 per year |

IRS Audit Protection | Included | Included |

1 Year Total Cost | $4,700 | $6,775 |

5 Year Total Cost | $9,500 | $14,695 |

Pricing pulled from company websites as of the article publish date.

IRA Financial

- $3,500 setup fee, which is $1,295 less than FranFund.

- $1,200 per year flat annual fee, billed once annually.

- Audit protection and ongoing compliance support included.

- No monthly billing and no separate TPA fee.

FranFund

- $4,795 one-time setup fee.

- $165 per month ($1,980 per year) TPA fee, required for IRS and DOL compliance and billed separately.

- Veteran discounts are available through their VetFran membership.

- Total first-year cost of $6,775, which is $2,075 more than IRA Financial.

FranFund's TPA fee is the highest monthly fee among the providers compared here. Over five years, FranFund costs more than $5,000 more than IRA Financial. The pricing transparency is appreciated, but the total cost is hard to overlook.

Winner: IRA Financial.

Lower setup fee and nearly $800 less per year in ongoing costs. Over five years, IRA Financial saves clients more than $5,000 compared to FranFund.

Setup Process and Speed: Getting Funded

Both providers manage the full ROBS setup process. FranFund's SafetyNet program is a standout feature worth a closer look.

IRA Financial

- Three-step setup: apply online, work with a ROBS specialist, and establish your C-Corp and 401(k).

- All documentation, fund transfers, and compliance setup handled in-house.

- Digital-first process with no paper-heavy workflows.

- ROBS specialists are available throughout to ensure proper execution.

FranFund

- 15 to 20 business day average setup timeline.

- SafetyNet program lets you start the IRA rollover at no cost before committing to setup fees. If you change your mind, there's nothing to undo and no refund needed.

- Dedicated TPA administrator assigned post-setup for ongoing plan management.

- Attorney consultation on C-Corp and 401(k) formation is included in the setup fee.

- A broad range of qualifying retirement plan types are accepted.

FranFund's SafetyNet is a genuinely useful feature for entrepreneurs who want to start the process without financial commitment. IRA Financial's specialist-led process is efficient and fully in-house. Both complete a compliant ROBS setup within similar timeframes.

Winner: Tie.

FranFund's SafetyNet option is a smart, low-risk way to start the process. IRA Financial's streamlined specialist-led setup is equally capable. Both deliver a compliant, full-service ROBS structure.

Compliance and Ongoing Support: Staying Protected

FranFund's dedicated TPA team is central to their ongoing compliance offering. IRA Financial combines in-house compliance with a legal foundation that runs deeper than plan administration alone.

IRA Financial

- IRS audit protection is included in the annual fee.

- In-house compliance team handles all ongoing plan administration and annual filings.

- ROBS specialists are available for questions throughout the life of your plan.

- Founded by a tax attorney, so compliance is embedded at every level of the organization.

FranFund

- Dedicated TPA administrator handles ongoing plan compliance.

- Less than 1% audit rate, with no disqualified plans during an audit.

- IRS and DOL audit assistance is included in the TPA service.

- Annual compliance testing, Form 5500 filing, and fair market value support are all included in the monthly TPA fee.

- Regular webinars help educate clients on trustee responsibilities.

FranFund's TPA service is comprehensive and clearly defined. Their audit record is strong. IRA Financial's legal foundation adds a layer of expertise that goes beyond plan administration, which is particularly valuable if compliance issues become complex.

Winner: IRA Financial.

FranFund's TPA team is solid and their audit record speaks for itself. IRA Financial's legal foundation gives it an edge when compliance questions go beyond routine administration.

Experience and Credentials: Who's Behind the Plan?

FranFund is franchise-focused and proud of it. IRA Financial takes a broader view, grounded in tax law expertise.

IRA Financial

- Founded by Adam Bergman, an ERISA attorney with a Master's in Taxation

- 27,000+ clients across ROBS, Solo 401(k), SDIRA, and related structures.

- Serves entrepreneurs across all business types, not just franchise buyers.

- Free educational content led by Adam Bergman, including weekly videos, podcasts, and written guides.

FranFund

- Franchise-specialist focus with strong relationships with franchise brands and the International Franchise Association.

- VetFran member, offering discounts for veteran entrepreneurs.

- Attorney consultation on formation is included in setup.

- Dedicated TPA administrator provides continuity of support post-setup.

FranFund is an excellent fit for franchise buyers who want a provider embedded in the franchise ecosystem. IRA Financial serves a wider range of entrepreneurs and brings legal expertise that FranFund's franchise focus doesn't replicate.

Winner: IRA Financial.

FranFund's franchise relationships are a real advantage for franchise buyers. For everyone else, and for anyone who values legal expertise, IRA Financial is the stronger choice.

Final Thoughts: Why IRA Financial Is the Smarter Choice

FranFund is a capable ROBS provider with transparent pricing, a thoughtful SafetyNet program, and a dedicated TPA team. If you're buying a franchise and want a provider with deep ties to the franchise industry, FranFund is worth considering.

But for most entrepreneurs, IRA Financial offers a lower total cost, deeper legal expertise, and an equally strong compliance track record without the higher monthly TPA fee.

Book a free call with a ROBS retirement specialist

- Learn how to fund your business using your retirement savings

- Review your ROBS 401(k) options with a specialist

- Get all of your questions answered

Checkbook IRA vs Custodian-Controlled SDIRA: A Decision Tree Based on Your Asset Strategy

Most investors choose between a Checkbook IRA and a Custodian-Controlled Self-Directed IRA (SDIRA) based on which one sounds more appealing.

That is the wrong starting point.

The structure that works best for a real estate investor making weekly expense payments is not the same structure that works best for someone making two or three passive fund investments per year. Choosing the wrong one does not just create friction. It creates compliance exposure that builds quietly until a filing or distribution forces a review. This guide gives you a decision tree based on what your assets actually require, not on which structure sounds like more control.

Key Takeaways:

- How each structure works in practice

- Where the two differ in daily operations

- A step-by-step decision tree based on your asset strategy

- An asset-by-asset fit comparison

- Where each structure creates risk or friction

- How to choose between them in 2026

How a Checkbook IRA Is Structured and How It Functions

A Checkbook IRA places IRA funds into an IRA-owned LLC. You act as the manager of that LLC. That setup allows you to write checks or send wires directly from the LLC account. Custodian involvement drops to funding and reporting rather than transaction execution.

With checkbook control, decisions move straight from you to the transaction rather than passing through the custodian. That directness is its primary advantage and its primary risk.

What a Custodian-Controlled SDIRA Structure Looks Like

A Custodian-Controlled SDIRA keeps the custodian involved in each transaction. Every investment, expense, and distribution runs through their process. That structure adds steps, and it also adds friction that slows mistakes down.

For many investors, that friction acts as a safety mechanism. Whether it is a help or a hindrance depends entirely on the assets you are holding and how often you need to move.

Where the Two Structures Differ in Practice

The difference shows up in daily operations, not legal theory.

| Feature | Checkbook IRA | Custodian-Controlled SDIRA |

|---|---|---|

| Transaction speed | Very fast | Slower, scheduled |

| Direct control | High | Limited |

| Custodian involvement | Minimal | Ongoing |

| Paper trail | Owner-managed | Custodian-managed |

| Error recovery | Harder | Easier |

Fast execution helps at the start, but long-term performance depends on having enough structure to handle compliance and documentation. The right choice is the one that matches your operational reality, not just your preference for control.

Read more: Custodian-Managed SDIRA vs. Checkbook IRA

Which Structure Fits Your Asset Strategy

Working through these steps in order filters out options that do not match your asset strategy.

Step 1: How often will you transact?

Multiple transactions per month or time-sensitive closings and payments favor Checkbook IRAs. Occasional investments with few annual transactions align better with Custodian-Controlled SDIRAs.

Step 2: Do your assets require rapid payments?

Assets that need same-day earnest money, repeated expense payments, or flexible wiring often benefit from checkbook control. Assets that move on scheduled capital calls or distributions usually fit custodian workflows without friction.

Step 3: How complex is compliance for your assets?

Assets with frequent personal involvement risk, related-party sensitivity, or gray-area transactions often benefit from custodian oversight. Assets with clean, repeatable structures tolerate checkbook execution more safely.

Step 4: How comfortable are you with documentation?

Checkbook IRAs require self-maintained records, clear separation of funds, and consistent transaction memos. If that level of ongoing discipline is not realistic for your situation, a Custodian-Controlled structure shifts recordkeeping and transaction processing back to the provider.

Book a free call with a self-directed retirement specialist

- Review your self-directed retirement options

- Learn about investing in alternative assets

- Get all of your questions answered

Asset-by-Asset Fit Comparison

| Asset Type | Better Fit | Why |

|---|---|---|

| Rental real estate | Checkbook IRA | Expense frequency and timing |

| Private notes | Either | Depends on payment volume |

| Private equity funds | Custodian-Controlled | Capital calls and reporting |

| Crypto | Depends | Wallet control vs reporting |

| Single passive deal | Custodian-Controlled | Low activity |

The table focuses on how assets move and get handled day to day, which is what determines custodian fit more than any other factor.

Where Checkbook IRAs Create Risk

High control increases risk by removing checkpoints, allowing small errors to accumulate before anyone notices. Common pressure points include commingling funds, paying expenses incorrectly, incomplete transaction records, and accidental personal use of IRA-owned assets.

These issues usually appear once filings or distributions force a review of past transactions, at which point the correction process is significantly more complicated than it would have been if the error had been caught earlier.

Where Custodian-Controlled SDIRAs Create Friction

Added oversight typically results in longer processing times while keeping compliance risk contained. Typical challenges include missed closing deadlines, slow expense reimbursement, paperwork backlogs, and limited flexibility during deals.

For some strategies, that friction blocks opportunities that require immediate action. For others, the slower pace is entirely manageable and worth the compliance protection it provides.

How to Choose Between the Two in 2026

The right starting point is asset behavior, not personal preference for control or cost. Structure should follow strategy.

A practical approach: map expected transaction volume for three years, identify which assets need fast execution, assign checkbook control only where speed genuinely matters, and keep custodian oversight where compliance risk is higher. Many investors split strategies across structures so each IRA only handles the assets it can manage cleanly.

Common Mistakes When Choosing a Structure

These patterns repeat themselves because the underlying decisions tend to be the same.

- Choosing checkbook control for simplicity rather than genuine operational necessity

- Assuming custodians prevent prohibited transactions (they do not)

- Underestimating the documentation workload that checkbook control requires

- Overvaluing speed for assets that do not actually need it

Each mistake traces back to skipping strategy alignment and choosing based on cost or perceived control instead.

Final Thoughts

A Checkbook IRA and a Custodian-Controlled SDIRA are tools, not upgrades from one to the other. Each solves different problems. Choosing based on asset flow, transaction frequency, and compliance tolerance produces cleaner outcomes than choosing based on either cost or control alone.

In 2026, the investors who run into the fewest problems are the ones who matched their structure to their strategy before the assets were in place, not after.

How to Use a Solo 401(k) to Invest in a Private Equity Fund Without Triggering UBIT

Private equity funds have historically delivered some of the strongest long-term returns available to sophisticated investors, and a Solo 401(k) is one of the most tax-advantaged vehicles for accessing them. But the intersection of retirement accounts and private equity comes with a specific tax risk most investors do not discover until it is too late: Unrelated Business Income Tax, or UBIT. This guide explains exactly when UBIT applies to Solo 401(k) private equity investments, how to structure your investment to avoid it, and what IRA Financial's approach looks like in practice.

Key Takeaways

- What UBIT is and why it applies to retirement accounts

- Which private equity investments trigger UBIT and which do not

- The Solo 401(k)'s structural advantage over an IRA for private equity

- How to use a UBIT blocker corporation to minimize exposure

- What to look for in a fund before you invest

- Common mistakes Solo 401(k) investors make with private equity

What Is UBIT and Why Does It Apply to Retirement Accounts?

UBIT is a federal tax imposed on retirement accounts, including Solo 401(k) plans, when they generate income from an active trade or business rather than passive investment activity.

The logic behind UBIT is straightforward. Congress designed retirement accounts to shelter passive investment income, dividends, interest, capital gains, and rent, from taxation. UBIT exists to prevent tax-exempt accounts from gaining an unfair competitive advantage over taxable businesses by engaging in the same active commercial activities. When a Solo 401(k) invests in a private equity fund structured as a partnership, which most funds are, the plan may receive a Schedule K-1 that includes income characterized as ordinary business income rather than passive investment return. That ordinary income is what triggers UBIT.

The UBIT rules apply to both Self-Directed IRAs and Solo 401(k) plans, but the Solo 401(k) has a meaningful structural advantage in navigating them that most investors do not know about.

Does Every Private Equity Investment Trigger UBIT?

Not every private equity investment triggers UBIT. The tax only applies when the fund's income is characterized as income from an active trade or business, or when the fund uses debt financing.

Two specific scenarios generate UBIT exposure for Solo 401(k) investors in private equity funds.

Scenario 1: Active business income passed through the fund. If the private equity fund operates or controls a business rather than simply holding a passive equity stake, the income passed through to your Solo 401(k) via the K-1 may be characterized as Unrelated Business Taxable Income. The determining factor is whether the fund is an active participant in the business's operations or a passive investor.

Scenario 2: Debt-financed income (UDFI). When a private equity fund uses leverage, borrowing to amplify returns, the portion of income attributable to that debt is subject to Unrelated Debt-Financed Income (UDFI) rules, which are a subset of UBIT. The UDFI rules calculate the taxable portion based on the ratio of acquisition indebtedness to the fund's average adjusted basis.

Purely passive private equity investments, where the fund holds equity stakes without operating the underlying businesses and without leveraging the portfolio, typically do not generate UBTI. The challenge is that most private equity funds do not advertise their UBIT implications clearly, and K-1s often arrive long after the investment decision has been made.

The Solo 401(k)'s Structural Advantage Over an IRA for Private Equity

A Solo 401(k) has a specific UBIT exemption that Self-Directed IRAs do not: the UDFI exception for real property acquired with debt financing.

For Solo 401(k) plans, the UDFI exemption means that debt-financed real estate held inside the plan does not trigger UBIT, a significant advantage over an IRA which does not have this exemption. While this exemption applies specifically to real property rather than private equity broadly, it illustrates an important principle: the Solo 401(k)'s legal structure provides more favorable UBIT treatment than an IRA in certain investment categories.

For private equity specifically, this matters when evaluating funds that hold real estate assets or use real property as part of their investment strategy. A Solo 401(k) investor in a real estate-focused private equity fund may have significantly better UBIT outcomes than an IRA investor in the same fund.

IRA Financial works with clients on using a Solo 401(k) for real estate investment funds as part of a broader UBIT minimization strategy. This depends on careful fund selection and structure analysis before the investment is made, not after.

How to Structure a Solo 401(k) Private Equity Investment to Minimize UBIT

The most effective UBIT minimization strategy for Solo 401(k) private equity investments is the UBIT Blocker Corporation, a C-corporation inserted between your Solo 401(k) and the private equity fund to convert active business income into dividend income.

Here is how the structure works:

- Your Solo 401(k) invests in a C-corporation (the "blocker") rather than directly into the private equity fund

- The C-corporation invests directly into the private equity fund as a limited partner

- The private equity fund distributes income to the C-corporation. Because C-corporations are taxed entities, the income is taxed at the corporate rate (currently 21%) at the blocker level

- The C-corporation pays dividends to your Solo 401(k). Dividends are passive investment income, not UBTI, so they flow into your plan tax-free at the retirement account level

The UBIT blocker corporation strategy does not eliminate all taxation. The C-corporation pays corporate tax on the income it receives. But it converts what would have been UBIT (taxed at trust rates that reach 37% quickly) into corporate-rate income at 21%, and eliminates UBIT at the Solo 401(k) level entirely. For large investments generating significant active income, this structure produces meaningful tax savings.

What to Look for in a Private Equity Fund Before You Invest

Evaluating UBIT exposure before committing capital is far more effective than managing it after the fact. Here are the key things to review before your Solo 401(k) invests in any private equity fund.

Review the fund's offering documents for leverage disclosure. Limited Partnership Agreements and Private Placement Memoranda should disclose whether the fund intends to use debt financing. A fund that plans to leverage portfolio companies will generate UDFI for retirement account investors.

Request a sample K-1 from a prior year. The K-1 will show you how the fund characterizes its income. Ordinary income on Line 1 is a signal of active business income. Capital gains on Line 9 and interest and dividends on Lines 5 and 6 are generally passive. A fund that has historically generated only capital gains and dividend income is far less likely to trigger UBIT than one generating ordinary income.

Ask the fund manager directly about UBIT. A fund manager who works with retirement account investors regularly will have a prepared answer. One who does not know what UBIT is, or dismisses the question, is telling you something important about their investor base and their diligence on this issue.

Evaluate whether the fund offers a blocker structure. Some institutional private equity funds offer a parallel UBIT blocker vehicle specifically for tax-exempt and retirement account investors. If the fund you are evaluating has this option, it eliminates the need for you to establish your own blocker corporation.

Book a free call with a self-directed retirement specialist

- Review your self-directed retirement options

- Learn about investing in alternative assets

- Get all of your questions answered

How Much UBIT Would You Actually Owe Without a Blocker?

UBIT on Solo 401(k) income is taxed at trust tax rates, which are compressed relative to individual rates, meaning high UBIT income reaches the top bracket quickly.

For 2026, Solo 401(k) plans as trusts reach the 37% federal tax bracket at just $15,650 of UBTI. A private equity investment generating $100,000 of UBTI inside your Solo 401(k) would produce a federal tax bill of approximately $35,000 to $37,000, paid from plan assets, directly reducing the tax-advantaged balance you have worked to build.

The UBTI tax rate calculation also requires filing IRS Form 990-T on behalf of the plan. This is a filing obligation most Solo 401(k) holders are unaware of, and one that creates additional compliance exposure if missed.

By contrast, a UBIT blocker corporation paying 21% corporate tax on the same $100,000 would reduce the effective tax rate by more than 40% relative to unmanaged UBIT exposure.

The Role of Checkbook Control in Private Equity Investments

A checkbook control Solo 401(k) gives your plan a dedicated bank account and LLC or trust structure, allowing you to invest directly without custodian approval for each transaction. For private equity investments, this matters in two specific ways.

First, speed. Private equity fund closings often have tight deadlines. A fund that closes on a rolling basis or has a hard close date will not wait for custodian processing. Checkbook control allows you to wire funds directly from your Solo 401(k)'s bank account when the capital call arrives, without a multi-day approval process.

Second, blocker corporation funding. If you are using a UBIT blocker corporation, checkbook control allows your Solo 401(k) to invest directly into the C-corporation, which then invests into the fund. Without checkbook control, this two-step structure becomes logistically complicated and custodian-dependent.

IRA Financial's Solo 401(k) includes checkbook control as a standard feature, a meaningful operational advantage for investors making time-sensitive private equity commitments.

Common Mistakes Solo 401(k) Investors Make with Private Equity

Investing directly without reviewing K-1 characterization. The most common mistake is committing capital to a fund without understanding how its income will be characterized on the K-1. By the time the K-1 arrives, often 12 to 18 months after the investment, it is too late to restructure.

Assuming capital gains treatment means no UBIT. A fund that sells a portfolio company and distributes long-term capital gains does not trigger UBIT. But many funds generate a mix of income types, some capital gains and some ordinary income, and the ordinary income portion remains taxable even when the fund's overall returns look like capital gains from the outside.

Confusing the UDFI exemption scope. The Solo 401(k)'s UDFI exemption applies to real property, not to leveraged private equity investments broadly. A fund that borrows to buy operating companies rather than real property still generates UDFI for Solo 401(k) investors. This is one of the most common misconceptions IRA Financial encounters from investors who have read about the Solo 401(k)'s UDFI advantage but applied it too broadly.

Missing the Form 990-T filing obligation. If your Solo 401(k) generates more than $1,000 of UBTI in a year, the plan must file Form 990-T. Missing this filing triggers penalties, and the IRS has been increasing scrutiny of retirement accounts with alternative investments in recent years.

Comparison: Direct Investment vs. Blocker Corporation Structure

| Factor | Direct Solo 401(k) Investment | UBIT Blocker Corporation |

|---|---|---|

| UBIT on active income | Taxed at trust rates (up to 37%) | Eliminated at plan level |

| Corporate tax on income | None | 21% paid by C-corporation |

| Dividend income to plan | N/A | Tax-free (passive income) |

| Setup complexity | Low | Moderate (C-corporation establishment required) |

| Best for | Passive-income-only funds | Funds generating active or leveraged income |

| Form 990-T required? | Yes, if UBTI exceeds $1,000 | No, at the Solo 401(k) level |

| Checkbook control benefit | Helpful for timing | Essential for two-step structure |

Frequently Asked Questions

Does all private equity income inside a Solo 401(k) trigger UBIT?

No. UBIT only applies when the income is characterized as income from an active trade or business, or when the fund uses debt financing that generates UDFI. Purely passive funds generating capital gains, interest, and dividends typically do not trigger UBIT. The characterization depends on the fund's structure and activities, which is why reviewing the K-1 and offering documents before investing is essential.

Can I use a Self-Directed IRA instead of a Solo 401(k) for private equity to avoid UBIT?

A Self-Directed IRA faces the same UBIT rules as a Solo 401(k) for active business income, with one important difference: the IRA does not have the UDFI exemption for debt-financed real property that the Solo 401(k) has. For real-estate-focused private equity funds that use leverage, a Solo 401(k) is generally the more tax-efficient vehicle.

How do I set up a UBIT blocker corporation for my Solo 401(k)?

The process involves establishing a C-corporation, having your Solo 401(k) invest in the C-corporation by purchasing shares, and having the C-corporation invest in the private equity fund as a limited partner. IRA Financial's ERISA attorneys can structure and document this arrangement in compliance with prohibited transaction rules. The setup requires careful attention to ensure the blocker corporation does not create a prohibited transaction between the plan and a disqualified person.

What is the minimum Solo 401(k) balance that makes a UBIT blocker worth the setup cost?

The blocker corporation structure generally becomes cost-effective when the expected UBTI from the investment exceeds approximately $20,000 to $25,000 annually. Below that threshold, the C-corporation setup and maintenance costs may offset the tax savings. Above it, the difference between trust-rate UBIT and corporate-rate tax at the blocker level typically justifies the structure.

Does IRA Financial help with Form 990-T filing for Solo 401(k) plans with UBIT?

Yes. IRA Financial's in-house tax filing and IRS reporting service covers Form 990-T filing for Solo 401(k) plans that generate UBTI, an obligation that many plan holders are unaware of until a tax professional flags it during year-end review.

Comparing IRA Financial's Solo 401(k) to Discount "Doc-Only" Providers: What Are You Really Paying For?

Most people shopping for a Solo 401(k) compare prices and stop there.

A doc-only plan at a low annual fee looks identical on paper to a fully administered platform.

The IRS document is the same.

The account type is the same.

What is not the same is everything that happens after you sign up, and that is important to understand as an investor.

Key Takeaways:

- What doc-only providers include and what they leave out

- What a full-service Solo 401(k) platform provides beyond the document

- A side-by-side feature comparison

- The real compliance responsibilities that come with lower-cost plans

- How to decide which option fits how you plan to use the account

What "Doc-Only" Solo 401(k) Providers Typically Sell

Discount or "doc-only" providers typically offer a basic Solo 401(k) plan document, limited or no ongoing administration, minimal support after setup, no investment infrastructure, and no transaction or compliance review.

Their value proposition is straightforward: low upfront cost. For investors who only need a compliant plan document and are comfortable managing everything else themselves, that can be a reasonable fit. What they do not provide is often misunderstood until it matters.

What IRA Financial's Solo 401(k) Provides For Investors

IRA Financial's Solo 401(k) is structured as a full-service, self-directed plan. That typically includes plan establishment and ongoing administration, support for alternative investments, optional checkbook control, compliance guidance around prohibited transactions, assistance with required filings and plan amendments, and infrastructure designed for long-term use rather than one-time setup.

The cost difference reflects scope, not markup.

Side-by-Side Comparison

| Feature | IRA Financial Solo 401(k) | Discount "Doc-Only" Provider |

|---|---|---|

| Plan Documents | Included | Included |

| Ongoing Administration | Yes | No |

| Self-Directed Investing | Yes | Usually No |

| Checkbook Control Option | Yes | Rare |

| Support for Alternative Assets | Yes | Limited or None |

| Compliance and Rule Guidance | Built-in | Self-managed |

| Form 5500-EZ Awareness | Supported | User responsibility |

| Long-Term Plan Maintenance | Designed for it | Not included |

What You Are Really Paying For

1. Ongoing Compliance, Not Just Setup

Solo 401(k)s require more than a one-time document. Tracking contribution limits, monitoring eligibility rules as your business changes, filing Form 5500-EZ once assets exceed $250,000, and adopting plan amendments when laws change are all ongoing responsibilities.

With a doc-only plan, that responsibility sits entirely with you. With a full-service provider, you have support navigating those requirements as they come up.

2. Investment Infrastructure

Many Solo 401(k) owners start with simple investments and eventually want to move beyond mutual funds into real estate, real estate syndications, private equity, or private credit. Doc-only plans often lack the mechanisms to execute these investments properly, not because the plan document prohibits them, but because the administrative infrastructure to support them was never built.

3. Risk Reduction

The most expensive Solo 401(k) mistake is not paying higher fees. It is disqualification. Common errors include prohibited transactions, improper loans, incorrect ownership structures, and missed filings. A full-service platform reduces the likelihood of structural mistakes that can cost far more than the difference in annual fees.

The Real Cost of Lower-Fee Plans

Lower-cost plans shift responsibility, not cost, to the user. It is worth being clear about what that means in practice.

| Risk | Who Bears It With Doc-Only Plans |

|---|---|

| IRS filing errors | You |

| Compliance mistakes | You |

| Missed amendments | You |

| Disallowed investments | You |

| Audit exposure | You |

The savings at setup tempting. So is thinking you can handle all of the responsibilities. The question is whether you have the knowledge and time to handle these duties.

It is also worth noting that even with a full-service provider like IRA Financial, the account holder retains ultimate responsibility for investment decisions and compliance. What changes is the level of support and guidance available when questions arise.

Who Doc-Only Providers Are Actually Best For

Doc-only Solo 401(k)s can be a reasonable fit for investors who only invest in public markets, are comfortable managing IRS compliance independently, want the lowest possible upfront cost, and expect minimal plan complexity over time.

They are less suitable for investors who plan to actively use the plan for alternative investments or who want support as their retirement strategy evolves.

Who IRA Financial's Solo 401(k) Is Best For

IRA Financial's structure tends to fit investors who want self-directed or alternative investments, expect their plan balance to grow significantly over time, prefer administrative support over managing compliance alone, and value long-term flexibility over upfront savings.

Book a free call with a self-directed retirement specialist

- Review your self-directed retirement options

- Learn about investing in alternative assets

- Get all of your questions answered

Cost vs Value: A Useful Frame

| Question | Doc-Only Plan | IRA Financial |

|---|---|---|

| How cheaply can I set this up? | Strong fit | Not the goal |

| How do I use this plan for 20+ years? | Weak fit | Strong fit |

| Who helps if rules change? | No one | Administrator |

| What if I want to invest in alternatives? | Limited | Supported |

Final Thoughts

The Solo 401(k) document itself is largely standardized. What differs is the support, infrastructure, and ongoing guidance that surrounds it.

Doc-only providers are built for investors who want low upfront costs and are comfortable handling compliance independently. IRA Financial is built for investors who want a platform they can actually use over decades, across a wide range of investments, with support when the rules get complicated.

The right question is not which plan is cheaper. It is what you are taking on when you choose the lower-cost option, and whether that tradeoff makes sense for how you plan to invest.

What Makes a Great Solo 401(k) Provider?

If you are self-employed and serious about retirement savings, the Solo 401(k) is one of the most powerful tools available to you. It offers higher contribution limits than a SEP IRA, loan privileges, Roth options, and with the right provider, the ability to invest in alternative assets like real estate, private equity, and crypto. But not every Solo 401(k) provider is built the same way, and choosing the wrong one can cost you far more than fees. This guide gives you an objective framework for evaluating your options and the specific questions you should be asking before you sign anything.

Key Takeaways:

- What a Solo 401(k) provider actually does and the key split in the market

- Eight criteria for objectively evaluating any provider

- A provider evaluation scorecard you can use side by side

- How IRA Financial measures against each criterion

What Does a Solo 401(k) Provider Actually Do?

A Solo 401(k) provider establishes, administers, and maintains your plan documents, ensures IRS compliance, and depending on the provider, offers varying levels of investment flexibility, tax filing support, and ongoing guidance.

That definition matters because it reveals the first major split in the market: custodial providers versus plan document providers. Custodial providers like Fidelity or Schwab hold your assets but typically restrict you to stocks, bonds, ETFs, and mutual funds. Plan document providers like IRA Financial give you a self-directed Solo 401(k) with checkbook control, meaning you can invest in a much broader universe of assets including real estate, private placements, crypto, and tax liens, without needing custodian approval for each transaction.

Understanding which type of provider you are evaluating is the essential first step, because the criteria for evaluating them are fundamentally different.

Read more: Top Solo 401(k) Providers of 2026

Criterion 1: Investment Flexibility

The investment universe your provider permits is often the single most consequential factor in long-term wealth building through a Solo 401(k).

A standard brokerage-based Solo 401(k) limits you to publicly traded securities. If your investment thesis includes real estate, private equity, hard money lending, or cryptocurrency, a brokerage provider will not serve you. You need a provider that offers a truly self-directed structure.

Questions to ask every provider:

- Can I invest in real estate, private placements, or alternative assets?

- Do I need custodian approval for each investment, or do I have checkbook control?

- Are there asset classes your plan explicitly prohibits beyond IRS-mandated restrictions?

A provider that hedges on any of these answers, or buries the restrictions in fine print, is telling you something important.

Criterion 2: Contribution Limit Expertise

For 2026, the Solo 401(k) allows up to $72,000 in total contributions ($80,000 if you are 50 or older with standard catch-up contributions, or $83,250 for those ages 60 to 63 under the enhanced catch-up rules), combining employee deferrals and employer profit-sharing. The math behind maximizing those limits is more complex than most providers communicate upfront.

Your provider should be able to walk you through how employee deferrals and profit-sharing contributions interact based on your business structure, the impact of the 2026 Roth catch-up contribution rules for high earners, whether your business situation qualifies for a Mega Backdoor Roth through after-tax contributions, and how to handle contributions if you have multiple income sources or business entities.

A provider who quotes you the contribution limit without asking about your business structure is not giving you the full picture. The difference between optimized and unoptimized contributions can be tens of thousands of dollars per year.

Criterion 3: Plan Document Quality

The plan document is the legal foundation of your Solo 401(k). It dictates what you can invest in, what loans are permitted, how distributions work, and how your plan stays compliant with IRS rules. This is one of the most overlooked evaluation criteria and one of the most important.

Key questions:

- Is the plan document an IRS-approved prototype plan or a custom-drafted plan?

- Does it explicitly allow for alternative investments, loan provisions, and Roth contributions?

- Who drafted the plan documents, a licensed ERISA attorney or a template provider?

- How are plan documents updated when tax law changes, such as SECURE Act 2.0?

IRA Financial's Solo 401(k) plan documents are drafted by in-house ERISA attorneys and updated continuously to reflect regulatory changes. A thin or outdated plan document can create compliance exposure that follows you for years.

Criterion 4: IRS Compliance and Tax Filing Support

A Solo 401(k) is not a set-it-and-forget-it product. Ongoing compliance involves annual reporting requirements, prohibited transaction rules, required minimum distributions, and once plan assets exceed $250,000, mandatory IRS Form 5500-EZ filing.

Evaluate every provider on:

- Do they offer in-house tax filing and IRS reporting, or do they outsource it?

- What happens when you have a prohibited transaction question? Is there a licensed professional available?

- How do they handle the controlled group rules if your business structure becomes more complex?

- Do they provide ongoing consulting, or does support end after plan establishment?

IRA Financial offers an in-house tax filing, IRS reporting, and annual consulting service specifically for Solo 401(k) plan holders, handling Form 5500-EZ filings and providing year-round access to tax and ERISA professionals. Most providers do not offer this. Those that do often charge separately for each interaction.

Criterion 5: Loan Provisions

One of the significant advantages of a Solo 401(k) over a SEP IRA or Self-Directed IRA is the ability to borrow from your plan, up to $50,000 or 50% of your vested account balance, whichever is less. Not every provider structures this correctly.

When evaluating loan provisions:

- Does the provider's plan document explicitly include loan provisions?

- What are the repayment terms, interest rate requirements, and documentation requirements?

- What happens to your loan if you miss a payment? Does the provider have a process for addressing it?

The Solo 401(k) loan rules have specific IRS requirements around documentation and repayment schedules. A provider who waves off these details is one who will leave you exposed if the IRS ever scrutinizes your plan.

Criterion 6: Speed and Setup Process

How quickly can you establish your plan, fund it, and make your first investment? This matters more than it might seem. Solo 401(k) plans must be established by December 31 of the tax year for which you want to make elective deferral contributions. If a provider's setup process takes six to eight weeks, a late-October inquiry could mean missing an entire year of contribution opportunity.

Ask specifically:

- What is the average time from application to plan establishment?

- What documentation do you need to provide, and how is the process managed?

- Can the plan be funded and ready for investment in time to meet your contribution deadlines?

Criterion 7: Fee Structure and Transparency

Fee structures across Solo 401(k) providers vary enormously, from free brokerage plans with investment restrictions to flat annual fees, transaction fees, or asset-based fees. The right fee structure depends on your investment activity and asset levels.

A few realities worth understanding. Free Solo 401(k) plans from brokerages typically generate revenue through investment product margins, not plan administration fees. That is fine if you want index funds. It is a problem if you want alternatives. Asset-based fee models from some custodians become expensive quickly as your account grows. A fee that seems reasonable at $100,000 can be very costly at $500,000. Flat annual fee models are typically more predictable and cost-effective for active investors with growing balances.

Ask every provider for a complete fee schedule in writing, including any fees for transactions, investment approvals, loan administration, or IRS filings.

Criterion 8: Checkbook Control

Checkbook control means your Solo 401(k) holds a dedicated bank account, and you, as the plan trustee, write checks or initiate wires directly from that account to make investments. No custodian approval, no transaction delays, no per-investment fees.

For investors in time-sensitive asset classes, real estate, private placements, and tax liens, this is not a convenience feature. It is a practical necessity. Waiting five to ten business days for custodian approval on a real estate deal with a 48-hour funding requirement means losing the deal.

The checkbook control Solo 401(k) structure is available through self-directed plan providers but not through brokerage-based providers. If alternative investments are part of your strategy, this single criterion may narrow your provider options significantly.

The Provider Evaluation Scorecard

| Criterion | What to Look For | Red Flags |

|---|---|---|

| Investment flexibility | Explicit alternative asset permission, checkbook control | Vague answers, custodian approval required per transaction |

| Contribution expertise | Business-structure-specific guidance, Roth and catch-up optimization | One-size-fits-all limit quotes |

| Plan document quality | ERISA attorney-drafted, regularly updated | Template plans, no mention of ERISA compliance |

| Compliance support | In-house tax filing, ongoing ERISA consulting | Outsourced or fee-per-call support |

| Loan provisions | Explicit IRS-compliant loan documentation | Loan availability unclear or undocumented |

| Setup speed | Clear timeline, December 31 deadline awareness | Vague timelines, no deadline guidance |

| Fee transparency | Complete written fee schedule | Fees disclosed piecemeal or only on request |

| Checkbook control | LLC or trust-based structure with dedicated bank account | No mention of checkbook control |

Read more: Solo 401(k) Provider Scorecard: 15 Questions to Ask Before You Choose

How IRA Financial Measures Against This Framework

IRA Financial was founded by tax attorneys with an explicit focus on self-directed retirement plans. The Solo 401(k) is designed for investors who want maximum flexibility, contribution optimization, and compliance confidence.

Against the eight criteria above:

- Investment flexibility: IRA Financial's Solo 401(k) permits investment in real estate, private equity, cryptocurrency, hard money loans, tax liens, foreign assets, and more.

- Contribution expertise: IRA Financial provides business-structure-specific contribution analysis, including high-earner strategies, Roth optimization, and catch-up contribution guidance.

- Plan document quality: Plans are drafted by in-house ERISA attorneys and updated to reflect current law, including SECURE Act 2.0 provisions.

- Compliance support: In-house tax and ERISA professionals handle Form 5500-EZ filings and provide ongoing plan consulting.

- Loan provisions: IRA Financial's plan documents explicitly include IRS-compliant loan provisions with full documentation support.

- Setup speed: Plans are typically established within days, not weeks.

- Fee transparency: IRA Financial operates on a flat annual fee model with no transaction fees or asset-based charges.

- Checkbook control: IRA Financial's Solo 401(k) includes a dedicated LLC or trust with a separate bank account for direct investment.

Book a free call with a self-directed retirement specialist

- Review your self-directed retirement options

- Learn about investing in alternative assets

- Get all of your questions answered

Frequently Asked Questions

What is the most important factor when choosing a Solo 401(k) provider?

Investment flexibility and compliance support are the two most consequential criteria. Investment flexibility determines what your retirement assets can actually do over decades. Compliance support determines whether your plan stays protected from IRS scrutiny. Every other factor is secondary to getting these two right.

Can I switch Solo 401(k) providers if I am unhappy with my current one?

Yes. You can transfer your Solo 401(k) to a new provider through a direct plan-to-plan transfer without triggering taxes or penalties. The process requires establishing a new plan and transferring assets. IRA Financial regularly assists clients with transfers from brokerage-based plans seeking greater investment flexibility.

Do free Solo 401(k) plans from brokerages have hidden costs?